This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

4 Fintech Unicorns in Hong Kong Hong Kong continues to cement its role as a fintech powerhouse in Asia, blending its strong regulatory framework with an innovation-friendly environment. The fintech unicorns in Asia are moving to reshape the very fabric of how people and businesses interact with money. billion insurtech Matrixport 1.05

With the launch of Ingo Money QuickConnect last week , the company capped off a year that CEO Drew Edwards told Karen Webster could best be characterized as the “Great Awakening” of push payments. We’ve finally moved beyond ‘so what is a push payment?’ That one bite is via a card that almost everyone has in their wallets today.

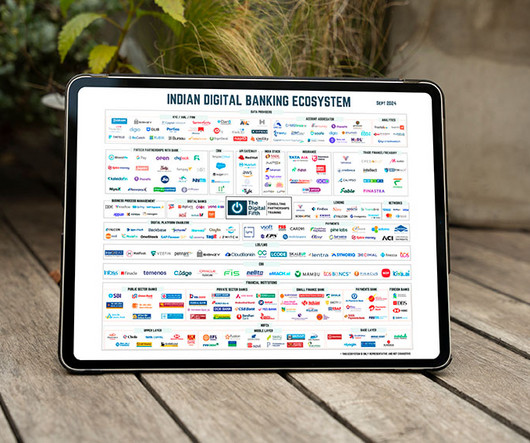

Despite a clear funding slowdown across global markets , Indias fintech sector continues to command significant capital, ranking as the third-highest funded fintech ecosystem globally after the United States and the United Kingdom. A standout USD $658 million Series D in 2023 signalled continued investor confidence. billion.

This dynamic ecosystem is supported by regulatory advancements and collaborative partnerships, which are expected to continue fostering innovation and growth in the sector. Banks push for digitalization According to the report, large banks are at the forefront of the sector’s digital transformation.

However, an awful lot is in fact different at the dusk of 2018 than it was at the dawn. The year 2018 saw massive changes in where consumers shop, how they pay, and what goods and services they want in their carts. Yet, as 2018 was coming to a close, Facebook was hit with just a bit more bad news. The Facebook Follies.

Continue to reduce any buying/selling friction. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. But it’s clear that the company remains very focused on building financial services products that support its core strategic goal: increasing participation in the Amazon ecosystem. Amazon Payments.

In short, while 2017 was the year of payments disruption, 2018 will be the year of the satisfied customer. The newest PYMNTS eBook is full of expert insight into the future of B2B payments, from commercial cards to accounts receivable. trillion: the current valuation of the U.S. trillion: the current valuation of the U.S.

Taiwan, along with South Korea, Hong Kong SAR, and Singapore, forms the group known as the ‘Four Asian Tigers,’ renowned for their rapid industrialisation since the 1960s. These economies have since developed into fully advanced nations. Taiwan’s gross domestic product (GDP) per capita is over $35,000.

Treasury will allow two financial technology companies to issue prepaid Visa cards loaded with coronavirus stimulus payments. Treasury Secretary Steven Mnuchin had said a more efficient distribution of government funds would be achieved through digital delivery and prepaid card providers. So far, the agency has delivered 89.5

Blockchain will continue to be among the hottest topics in payments and commerce in 2019 — and maybe one day people will agree on what blockchain really is and what it can really do. No, think of them as miniature seminars. These podcasts focus on innovation, best practices, learning from past failures and the like. Igniting B2B eCommerce.

trillion in 2018. are made with cash , for example, and 63 percent of consumers have at least two credit cards. These changes are likely here to stay, with 31 percent of bank customers saying they will continue to use digital payment methods even after the pandemic has passed. billion noncash payments totaling $97.04

Last year, Brex born as a scrappy startup with a corporate card for startups that transformed into a global fintech and enterprise SaaS firm in corporate spend made a bold move: it hit reset. This move simultaneously positioned Brex as a competitor to companies like Ramp and traditional corporate card providers.

Since Open Banking launched on January 18, 2018, banks have made a suite of mandatory APIs available to TPPs. Our first reaction to observing this opportunity was to consider if and how we could persuade the regulator to push banks to make more APIs available. NatWest has been working to solve this puzzle for several years.

Despite that reality, blockchain projects continue to roll in, and in this week’s Blockchain Tracker, PYMNTS takes a look at some of the largest names in tech marching forward with their faith in blockchain and its potential to disrupt enterprise processes. Mastercard. Reports said the filing, dated Nov. 9 with the U.S.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Virtual card issuance. Business lending and corporate cards. Supporting merchant partner growth. Growing the internet economy.

Since we would hate for anyone to go into the end of 2018 behind the eight ball, we decided to pay tribute to both a great bit and a great deal of news with our own top 10 list of the biggest news of summer 2018. It is not an exaggeration to say that 2018 has been the summer of movie subscription service MoviePass ’ discontent.

Regulatory disruption — think GDPR and open banking rules — shook up the business financial services market, while blockchain continued to dig deeper into use cases like trade finance and global payments. As part of that effort, Mastercard enabled push payments to small businesses from other companies via the Send solution.

Connecting these two dots suggests a few important things that, for banks and card networks, might be the 2020 hindsight that could have come in handy had they stopped to look backwards a few years ago: That the Fed has much more than a passing interest in how faster payments are run in the U.S. A Couple of Important Dots.

billion per year in incremental growth between 2018 and 2023. A multitude of security issues continue to plague the space, however, despite this optimistic future of digital identity. A multitude of security issues continue to plague the space, however, despite this optimistic future of digital identity.

Authorized push payment (APP) scam losses are on the rise, expected to climb to $7.6 Authorized push payment (APP) scam losses are on the rise, expected to climb to $7.6 billion by 2028 across six leading real-time payment markets (U.S., billion by 2028 across six leading real-time payment markets (U.S.,

Instances of APP fraud around the globe have continued to rise as real-time payment rails extend their reach. targeting both individuals and merchants during the first half of 2018, hitting £148 million ($191 million USD) in losses. The nature of these payments means that, once they have been made, consumers cannot reverse them.

Regulators in Mexico passed a law governing FinTechs in March 2018, just two months after PSD2 went into effect in the European Union, and others in the region have since followed suit. Mexico has crafted its upcoming rules with similar developments in mind, especially as its 2018 law makes the market more attractive to FinTechs.

The Financial Conduct Authority issued a consultation in 2017 called the ‘Credit card market study: consultation on persistent debt and earlier intervention remedies’ that was completed in July. From July 2018 issuers will need to prompt their cardholders if their expenditure surpasses pre-defined thresholds.

As digital infrastructure continues to advance, the ease and speed of contactless transactions are becoming increasingly attractive to consumers and businesses. Instead of entering a PIN or handling cash, users can simply tap their card or mobile device to complete a transaction in seconds. What are Contactless Payments?

Retail figures will vary as new stores continue to come online and the marketplace continues to evolve,” the report said. That market could reach as much as $5.1 billion in annual sales by 2020, according to one estimate – though some predictions are higher, especially ones that include spending on accessories and growing supplies.

These and other milestones have come to pass, pushing enterprise-scale AI solidly into the “early adoption” phase, as defined by “Chasm” author Geoffrey Moore. So, more work is needed to enforce and audit ethical AI usage, as 67% of AI leaders don't monitor their models to ensure continued accuracy and ethical treatment.

Petal , a startup with a mission to shake up the world of credit cards, is poised for more expansion after nailing down another big commitment from its investors. Once approved, customers gain access to a “high-quality Visa® credit card.” Once approved, customers gain access to a “high-quality Visa® credit card.”

As advanced analytics permeated nearly every industry in 2018, FICO’s thought leaders continued to push it into new areas. Here were the top 5 posts in the Analytics & Optimization category last year. Advancing the Field of Prescriptive Analytics. Read the full pos. The Financial Industry’s Digital Transformation.

The move pushes Visa ever further away from cards and toward its goal of becoming, as management has often described it, a “network of networks.”. Holiday (and Post-Holiday) Shopping: Throughout the month of December helped push retail sales up more than 5.8 branded cards business grew by 10 percent. percent year on year.

Charles Dickens’ famous starter to A Tale of Two Cities , as it turns out, is a pretty good way to sum up the year 2018 from the view of the alternative financial services segment. However, as 2018 wore on, headwinds started to blow back on the segment, most especially in the form of rising interest rates. That amounts to $13.2

JPM’s digital push, a theme it refers to as “Mobile First, Digital Everything,” is showing positive early results. JPM continues to improve its existing apps while also focusing on developing new ones (such as Finn) for future customers. JPM boasts an industry leading credit card network. First Name.

As demonstrated in the POC track II, NETS’ solution capitalises on the Push payment model via SGQR. In Singapore, micro and small merchants (MSMEs) are responding to the ever-increasing consumer demand for cashless options, and are swiftly embracing QR payment solutions.

A new year has begun, but the pandemic continues to throw financial and operational curveballs at banks, businesses and their consumers regarding how they conduct daily tasks or routine payments. consumers now count themselves as “ debit-centric ” users, a sizable jump over the 33 percent who said the same about credit cards.

Paper checks may become a thing of the past if healthcare’s trend toward modernization continues,” according to the new report. Paper checks may become a thing of the past if healthcare’s trend toward modernization continues,” according to the new report. For many, it’s very difficult. Real-Time Payments Get Healthy.

These systems, Pai said, are pushing the adoption of electronic payments among the country’s vast base of migrant workers. . Pai believes, however, that even if there are fees, workers will continue to use these services. As such, it’s common practice for these workers to send a portion of their wages home to their families.

No cards are needed. At Garanti BBVA, we continue to implement innovations to make our customers’ lives easier,” said Didem Dinçer Ba? billion as of June 30, 2018. billion as of June 30, 2018. The new feature is on the Garanti BBVA corporate mobile app and is available to business and personal users.

The project also could grow to include app or loyalty card identification of shoppers to further the frictionless commerce and payments ideal. Sainsbury’s also is taking part in the cashierless push. The grocery industry is making a go of it. The latest effort comes from the U.K. European Role. the report noted.

Among the company’s recent pushes in the restaurant space is helping to craft fraud prevention defenses for mobile order-ahead technology that, arguably, has recently emerged as one of the hottest trends in mobile commerce. It’s a relatively simple prospect: Select food. Order food. Happy Thanksgiving , by the way!). Getting Past Hype.

That unit will include the company’s online lending platform, Marcus , and credit card business, the latter of which is done through a joint venture with Apple. billion seen in December 2018. That includes Marcus and the Apple Card. If you can’t beat ’em, join ’em — at least when it comes to reporting structure.

Since about mid-December of 2018, checking out in the stores here in Boston has become even more of a hassle. Never mind the people who start rummaging around in their purse or wallet to pull out their cards after stepping up to the checkout counter. I say yes, because … well, what else is there to say? is nothing new.

New reports say 1 percent of all Bitcoin transactions involve criminal activity, and while this doesn’t sound like a lot, it’s almost double from 2018. Most customers still visit bank branches, but prefer digital in-branch experiences, pushing FIs to undergo digital transformations to provide the best customer engagement possible.

That unit will include the company’s online lending platform, Marcus , and credit card business, the latter of which is done through a joint venture with Apple. billion seen in December 2018. That includes Marcus and the Apple Card. If you can’t beat ’em, join ’em — at least when it comes to reporting structure.

For all the talk in the UK about disruptors and fintechs and new entrants to the credit market, and about how banks and card issuers need to manage customers in arrears, there’s one group that seems strangely absent from this focus: retailers. It is estimated over £200 billion of UK household debt is in unsecured retail credit.

While there has been some innovation in wage payment mechanisms as more employers shift away from the paper check toward direct deposit and payroll cards, little has changed about the timing of those payments. workforce doesn’t look like it used to. It’s also opened up conversations about how professionals get paid.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content