This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

payment processing landscape, covering market size, merchant demographics, transaction volumes, major players, and key trends shaping the industry. This market includes a range of services and technologies that facilitate the acceptance, authorization, and settlement of payments across various channels, including online, in-store, and mobile.

However, mobile payments, digital wallets, and real-time transactions are broadening financial access. How does the rise of real-time payments impact traditional banking in Latin America? Growth is driven by financial inclusion, fintech innovation, and regulatory reforms. Key Takeaways – Report Summary 2. Management Summary 3.

Founded in 2018, The Power 50 shines a spotlight on companies transforming financial services, while delivering ongoing support and development for participants. I am extremely proud of the support we have had from the industry and the sheer volume of entries we received.

Open banking is appealing to financial institutions (FIs) and regulators in many markets, even as the pandemic sweeps across the world. Regulators in other regions, including Latin America, are also shaping and announcing plans to enable open banking and better support digital financial systems. Around The Data Protection World.

A new report by Reputa, an online reputation monitoring system provided by Viettel, Vietnam’s state-owned telecommunications giant, offers an analysis of the country’s fintech sector and provides rankings of the most reputable fintech companies in Vietnam based on their online reputation and reach.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

A new year has begun, but the pandemic continues to throw financial and operational curveballs at banks, businesses and their consumers regarding how they conduct daily tasks or routine payments. This compares to just 17 percent of cardholders who experienced debit-related fraud as recently as 2018. The report noted that U.S.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4 billion by late 2022.

The fourth quarter of 2018 was kind to Venmo and Zelle , the two big peer-to-peer (P2P) services that are battling for consumer loyalty and market supremacy — a fight that pits PayPal , the owner of Venmo, against the banks that operate Zelle. 31, 2018, with a year-end goal of 300 million.) Zelle Bank Gains. P2P Numbers.

The EU enacted open banking rules in 2018, inspiring regulators worldwide to reconsider how they were transacting funds or transmitting data. Mobile and online payments are also on the rise for this same reason. COVID-19 Exposes Online Payment Concerns. and the EU. Australia and Canada.

Brick-and-mortar branches shuttered as social distancing measures were enforced, and customers subsequently turned to mobile apps or websites to fulfill their banking needs rather than risking in-person visits. Online account openings have increased 14.5 Confronting Digital Banking Reality.

For those watching the payments sphere, the tea leaves are there for the reading, tied to mobile and digital banking adoption, to outstanding balances on cards, and to auto loans and mortgages. 15) will mark releases from Bank of America and Goldman Sachs. Going Mobile. Tuesday (Jan. Looking at Credit.

Bank earnings this week gave us a bit of insight into the momentum gained by bank-backed P2P payment network Zelle in 2018. For example, Bank of America reported on Wednesday (Jan. 16) that Zelle payments were up 97 percent in Q4 2018, signaling the latest burst of growth for that payment method.

Mastercard beat estimates on Wednesday (May 2) as the company showed results that reflected higher spending on both credit and debit cards through the first quarter, as well as cross-border volumes that surged by double digits. The company said that worldwide gross dollar volume gained 14 percent to $1.4 The net revenue number of $3.6

Sure, activities like shopping online, getting food delivered, catching a cab or finding a gig are some of the most front-and-center examples. A study from Juniper Research found that mobile ticketing is becoming mainstream in sports, with users predicted to spend $23 billion via mobile in 2023, up from $14 billion in 2019.

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. In aggregate, these product development and investment decisions reveal that Amazon isn’t building a traditional bank that serves everyone.

trillion in total assets, JPMorgan Chase is the largest bank in the US. Its retail bank, Chase, spans 61 million American households. Led by Chairman and CEO Jamie Dimon, the bank is undergoing a transformation, moving away from offline legacy systems and into the digital age. Live briefing: Consumer Banks in The Digital Age.

Moreover, Adobe projects that voice-assisted retail will prove to be a big hit during the 2018 holiday shopping season — and that consumers already devoted to the technology will buy even more gear for themselves and others. #3: 6: With Person-To-Person Mobile Tech. But that’s changing in this era of mobile and digital commerce.

There are a few common themes among big bank earnings reports. consumer spending is carrying over to other areas where banks get their bread and butter. That positive consumer mindset has also helped foster positive sentiment among corporate and commercial customers of the bank, said Piepszak. Spending, Done Digitally.

In broad strokes, open banking lays out a path and process for banks and other financial institutions (FIs) to share their customers’ data with third parties (even competitors), where that data tie into apps and new products and services. Dan Weaver, open banking expert at Equifax U.K., Open Banking In The States .

Bank customers’ needs and demands of financial service providers are growing more sophisticated and complex. For the banks and merchants serving them, the challenge is matching the great strides in connectivity with consistency of experience and security. What is driving this trend? from EMVCo and “PIN on Glass” from the PCI Council.

Square ‘s Q4 earnings 2018 results came after market close on Wednesday (Feb. These trends included double-digit gross payment volume (GPV) growth, as measured year on year, double-digit transaction gains and traction in newer technology offerings — such as point-of-sale (POS) financing to help sellers log their own top-line growth.

In 2022, the country was home to 993 active fintech companies, representing about 25% of all fintech ventures operating across the ASEAN region, data from a 2022 report by the United Overseas Bank (UOB), PwC Singapore and the Singapore Fintech Association (SFA) reveal. billion to US$15 billion during the period. in July 2023.

Banking giant JPMorgan reported results that bested Wall Street estimates on Thursday, buoyed in part by strong growth in its card business and mobile initiatives. In the consumer and community banking segment, revenues were up 6 percent year on year to $12 billion. Credit card sales and merchant volumes were up 13 percent.

A 2018 survey by Bank of America shows that millennials’ top financial priorities were saving for emergency funds (64%), saving for retirement (49%), and saving to buy a house (33%) — not much different from the concerns their baby boomer parents had 30 years ago. From big banks to big tech. From big banks to big tech.

And they are incredibly mobile-connected – particularly when it comes to making choices about purchases, according to PYMNTS research. So-called online-only retailers — including Amazon — operate some 630 physical retail locations in the U.S., That presents ample opportunity for mobile retail. Digital Banking.

Since we would hate for anyone to go into the end of 2018 behind the eight ball, we decided to pay tribute to both a great bit and a great deal of news with our own top 10 list of the biggest news of summer 2018. million in tokens for DENT, a mobile data ICO; and over $1.1 Theranos Investors Settle. They also stole $13.8

For those watching the payments sphere, the tea leaves are there for the reading, tied to mobile and digital banking adoption, to outstanding balances on cards, and to auto loans and mortgages. 15) will mark releases from Bank of America and Goldman Sachs. Going Mobile. Tuesday (Jan. Looking at Credit.

Methods like a one-time password sent by text message (SMS), for example, can cause many consumers to abandon their online shopping carts. If the same abandonment rates are applied to increased eCommerce volume, merchants could miss out on a significant amount of lost revenue. Not a New Concept. Time Is Right.

Federal Reserve asset cap on Wells Fargo will last all year instead of through the first half, said the bank’s CEO Tim Sloan on Tuesday (Jan. 15), as the financial institution (FI) disclosed its Q4 2018 earnings. The bank, trying to restore trust among consumers and commercial clients, said full-year 2018 revenue decreased about 2.3

The startup has said that business banking on the continent needs to be repaired, and that it can provide a much better experience with its mobile and online-first offerings. . billion USD) in transaction volume last year. . billion USD) in transaction volume last year. .

airlines are cancelling all flights to and from mainland China due to the coronavirus outbreak and Starbucks reported 17 percent mobile order growth in its Q1 2020 earnings report. New reports say 1 percent of all Bitcoin transactions involve criminal activity, and while this doesn’t sound like a lot, it’s almost double from 2018.

Wearables are becoming the must-have of mobile devices. Trupay is one of the first private sector companies in India to offer a mobile payment app based on a unified payment interface (UPI), according to a press release. The gloves are off in the fight for Europe’s mobile payments market. But with the impending arrival of U.S.

Facebook reported on their website that their teams have made progress: They removed 837 million pieces of spam in Q1 2018 before anyone reported it, disabled 583 million fake accounts “within minutes” of going online and removed 24 million inappropriate pictures related to violence and nudity. million such pieces.

Coverage includes WorldRemit ’s partnership with Safaricom for money transfers to mobile money accounts in Kenya. In addition, Bambora is working with Payworks to introduce Bambora Connect, and Hong Kong-based The Bank of East Asia (BEA) has unveiled its i-Payment Hub. billion in 2018 to $22 billion by 2023.

Paying tuition used to be a difficult process, and involved exchanging yuan to South Korean won at a bank and then paying the university, noted the report. Although mobile payments are very common in China, simple cross-border transactions are not. In 2018, it had a daily transaction volume of over one billion.

Payment values went up 54 percent year over year, and payment volume increased 72 percent. The Zelle network is used by an upwards of 5,391 financial institutions (FIs), either through a mobilebanking app or by registering a debit card with Zelle’s app. According to eMarketer , nearly 80 million U.S. P2P Partnerships.

will last all year instead of through the first half, the bank’s CEO, Tim Sloan, said Tuesday (Jan. 15) as the financial institutions disclosed its Q4 and 2018 earnings. The bank, trying to restore trust among consumers and commercial clients, said that full year 2018 revenue decreased about 2.3 percent, to $86.4

The report, released in September 2023, looks at the Thai fintech sector, highlighting the rise of digital payments and the explosive growth of real-time transactions, as well as presenting the opportunities that exist in digital remittances, open banking, business-to-business (B2B) payments and agricultural lending.

Mobile point-of-sale (mPOS) solutions have enjoyed widespread uptake in much of North America, and the region’s related market could see continued growth if solutions providers, government officials and other stakeholders play their cards right. percent of total payments by volume in 2017 and debit responsible for 26.5 percent and 21.5

Among the findings of the recent 2018 Diary of Consumer Payment Choice , produced through several of the U.S. Federal Reserve Banks, electronic payments are on the rise. The Fed banks said that 14 percent of respondents reported making zero payments. Cards over cash – specifically, debit cards over cash. Cash represented 31.6

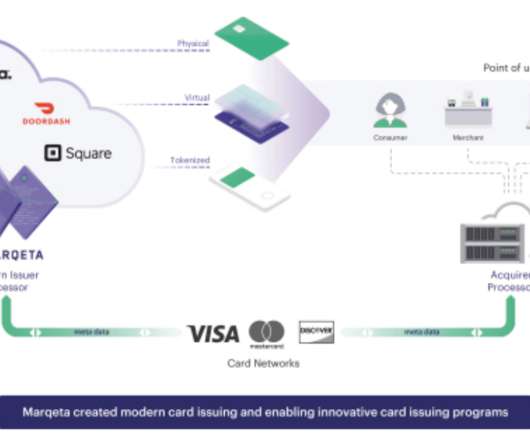

Marqeta allows businesses to offer payment card products to customers without having to deal directly with a traditional bank. It handles the back-end payment technology while working with banks that process the payment transactions. . in transaction volume. . G lobal online sales are expected to reach $4.8T

In addition, the company filed a patent in 2018 that explores additional layers of authentication, including asking users to perform certain actions like “smile, blink, or tilt his or her head.”. Banks use facial recognition for authentication. The company is hoping this technology will be showroom-ready by 2020.

In the wake of the outbreak, everything from doctors appointments to schooling to workouts went online. As more people have worked, learned, banked, exercised, relaxed, and even sought medical care from home during Covid-19, they have gotten a crash course in just how much can be accomplished at home. Online courses & content.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content