This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ACH credit payments are best for sending one-time payments whereas ACH debit payments are more suited for making regular payments, such as for monthly utility bills. All ACH payments are secure and reliable, available 24 hours a day, 7 days a week, and 365 days a year. What are ACH Debit Payments?

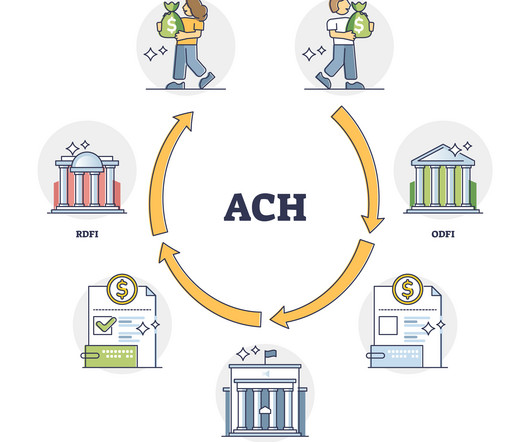

Automated Clearing House (ACH) is one type of EFT that processes payments in batches through the ACHNetwork. EFT and ACH offer more security and convenience than cash and checks, but they also come with limitations. Interconnecting 10,000 US banks and credit unions, this network continues to receive high demand.

NACHA — The Electronic Payments Association — announced that its membership has approved three new rules that will expand Same-DayACH for all financial institutions and their customers. The expansion of Same-DayACH will be made possible through the creation of a new Same-DayACH processing window by the two ACHNetwork operators.

Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACHnetwork provides. And the best part about ACH? Most ACH deposits are completed within 1-3 businessdays. Instead, everything is a click away.

The EFTA limits your liability for unauthorized transactions to $50 if you notify your bank within two businessdays of discovering the loss or theft of your card. However, if you don’t report it within 60 days, you could be held liable for any unauthorized transactions. So, an ACH payment is just one example of an EFT.

In this post, we’re going to review ACH and wire transfers, look at their similarities, and then see how they compare against each other. TL;DR ACH is cost-effective and ideal for recurring payments, with transfer times ranging from 1-3 businessdays. and territories) No geographical limitations except for U.S.

ACH transfers, or payments made through the Automated Clearing House network, account for billions of dollars in payments annually. In fact, NACHA, the nonprofit that governs the ACH payments network reported 6.1% The average consumer commonly uses the ACHnetwork for automated bill payments and larger transactions.

ACH (Automated Clearing House) payments are electronic fund transfers that use the ACHnetwork to move funds between bank accounts in the United States. This payment method is widely used for direct deposit of payroll, payment of bills, and business-to-business payments. Book a 30-min live demo now.

This is called an ACH direct deposit. Your employer sends the money through the ACHnetwork, and it ends up in your account, often on the same day. The ACH deposit meaning goes beyond just paychecks. When you set up an ACH direct deposit, the process starts with the person or company sending the money.

Paper Check Comparison Benefits for Businesses Common Questions About eCheck Payments Getting Started with eCheck Payments Key Takeaways eCheck payments are electronic versions of paper checks that process funds through the ACHnetworkBusinesses save 60-80% on transaction fees compared to credit card payments Processing typically takes 3-5 business (..)

The sender then enters payment details into their bank's ACH system, which sends the payment to the ACHnetwork for processing. The ACHnetwork checks the transaction and sends it to the receiver's bank for deposit.

By doing so, businesses can enhance their operations, and consumers can make more informed financial decisions. What are ACH payments? ACH payments refer to electronic funds transfers (EFTs) between financial institutions using the ACHnetwork. What are ACH payment codes?

ACH (Automated Clearing House) payments are basically EFTs ( electronic fund transfers ) that use the ACHnetwork to move funds between bank accounts in the United States. ACH is most commonly used for direct deposit of payroll, payment of bills, and business-to-business payments.

13, 2018, NACHA , the rules and standards body for the ACHnetwork, announced that its voting members had approved amendments to the NACHA Operating Rules & Guidelines to establish a third Same DayACH processing and settlement window,” the Federal Reserve wrote in the announcement. “On Sept.

In this article, we'll explore the ACHnetwork and ACH payments, how ACH payments function, and the ways in which it impacts our daily financial transactions. What are ACH payments? The clearing house was operated by people on businessdays only. Book a 30-min live demo now.

The National Automated Clearing House Association (NACHA) governs the ACHnetwork, setting rules and standards for ACH transactions. ACH processing fees are charges for processing electronic payments and transfers between bank accounts. This fee compensates the processor for the increased risk and handling of large sums.

Though usually just called ACH payments or ACH transfers, the term more specifically refers to a national payment network that banks and other institutions rely upon to process payments securely and accurately between parties. ACH payments are generally fast during the work week but aren’t instantaneous.

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACHnetwork in a single transaction or within a specified period. The two types of ACH transfers are ACH credit, where funds are pushed into an account, and ACH debit, where funds are pulled from an account.

First, let's delve into the mechanics of ACH and Wire transfers, followed by an exploration of their distinctions, guidance tailored for small businesses, and concluding with instructions on establishing ACH and Wire processes. What is ACH? NACHA for ACH and government-run rails like FedWire & Swift for Wire.

The significance of EFT transfers lies in their ability to facilitate immediate access to funds on nearly any given businessday. This immediate access is essential for both individuals and businesses to manage cash flows , make timely payments, and maintain financial stability. What is the Electronic Funds Transfer Act (EFTA)?

Thanks to the ACHnetwork, these transactions are handled securely and efficiently, giving consumers peace of mind when making payments. Direct Payments Direct payments are transactions initiated by individuals to pay for goods or services. This could include anything from paying your monthly utility bills to shopping online.

Read on and learn everything you need to know about ACH transfers , including their types, benefits, potential downsides, and their alternatives. What Is ACH Bank Transfer?: ACH transfers are electronic, bank-to-bank money transfers processed through the ACHnetwork. How to Initiate an ACH Bank Transfer?

Generally speaking, ACH payments are best suited for routine, smaller transactions, whereas wire transfers are preferred for urgent, high-value transfers. ACH Payment Wire Transfer Speed of transactions Typically takes 1-3 days for the receiving bank to receive the funds Within a day for a domestic wire transfer.

Automated Clearing House (ACH) transfers are a common form of EFT payment that facilitate the movement of funds between financial institutions in the U.S. ACH transfers operate via the ACHnetwork, managed by the National Automated Clearing House Association (NACHA), for merchants, banks, and individuals to initiate transactions.

ACH payments Another commonly used EFT payment type includes transactions conducted through the ACHnetwork. An ACH debit is frequently used for transactions like automatic bill pay and recurring payments but is also commonly used for one-time transactions.

With an electronic check, money is electronically transferred from the payer’s checking account to the seller’s checking account, where it is directly deposited after passing through the national ACHnetwork. At this stage, funds are withdrawn from the customer’s checking account and transferred to the business’s account.

Before diving deeper into SEC codes, let’s take a minute to better understand ACH transactions – if you’ve already worked with ACH transactions and have an idea about what is involved in them, you can skip this section and go straight to SEC codes. SEC Codes – The List.

ACH Transfers as EFT ACH transfer is a type of EFT, or electronic funds transfer. The ACHnetwork is a nationwide network of banks and financial institutions that handle electronic funds transfers. ACH Transfers: Typically 1-2 businessdays, but same-day options are available.

ACH Transfers as EFT ACH transfer is a type of EFT, or electronic funds transfer. The ACHnetwork is a nationwide network of banks and financial institutions that handle electronic funds transfers. ACH Transfers: Typically 1-2 businessdays, but same-day options are available.

FedNow offers a flexibility that conventional online transfers via the Automated Clearing House (ACH) Network currently don’t provide. ACH transfers, which operate in batch mode, typically require one to three businessdays for completion.

Senator Elizabeth Warren asks in a campaign ad, ignoring the fact that 93 percent of working Americans have their checks directly deposited into their bank accounts – ready for use on payday – using the ACHnetwork. Direct deposit over the ACHnetwork eliminated that friction and got them earlier access to those funds.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content