This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And on that note, two of the most common modes of electronic funds transfer are ACH and wiretransfers. In this post, we’re going to review ACH and wiretransfers, look at their similarities, and then see how they compare against each other. What is a WireTransfer?

ACH credit payments are best for sending one-time payments whereas ACH debit payments are more suited for making regular payments, such as for monthly utility bills. All ACH payments are secure and reliable, available 24 hours a day, 7 days a week, and 365 days a year. Learn More What are ACH Credit Payments?

Wiretransfers and electronic funds transfers have been staples of financial transactions for decades, but various electronic transfer methods have emerged with the innovation in banking technology. EFTs enable seamless direct payments for operations, including payroll, taxrefunds, and recurring bills.

ACH payments are a convenient way for business owners, individuals, and employers to use intuitive automated banking throughout their daily lives. Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACHnetwork provides.

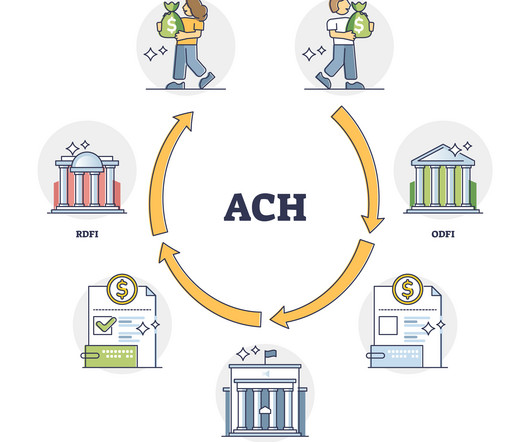

Though usually just called ACH payments or ACHtransfers, the term more specifically refers to a national payment network that banks and other institutions rely upon to process payments securely and accurately between parties. ACH payments are generally fast during the work week but aren’t instantaneous.

So, what is an ACH deposit? ACH direct deposits are common. Your paycheck, taxrefund, or even a government benefit could be sent to you this way. Understanding the ACH deposit meaning is important because it’s a fast, secure, and cost-effective way to transfer money. This is called an ACH direct deposit.

Some examples of direct deposits include government benefits, such as Social Security or unemployment benefits, taxrefunds, and payroll payments from employers. Thanks to the ACHnetwork, these transactions are handled securely and efficiently, giving consumers peace of mind when making payments.

Read on and learn everything you need to know about ACHtransfers , including their types, benefits, potential downsides, and their alternatives. What Is ACH Bank Transfer?: ACHtransfers are electronic, bank-to-bank money transfers processed through the ACHnetwork.

One of the advantages of EFT is that it's relatively quick - payments can be processed and transferred within a few days. EFT is also typically cheaper than other methods of payment (such as wiretransfer), and it's a convenient way to make recurring payments (such as monthly bills).

One of the advantages of EFT is that it's relatively quick - payments can be processed and transferred within a few days. EFT is also typically cheaper than other methods of payment (such as wiretransfer), and it's a convenient way to make recurring payments (such as monthly bills).

Also keen on the Fed’s involvement were the community banks and credit unions that worry (as they should) about having TCH as the only operator of an RTP network in the U.S. and one of two operators of the ACHnetwork in the U.S., TCH is the association of the 25 largest banks in the U.S., the other being the Fed.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content