This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many small businesses choose ACHoperators because they are more convenient than most direct deposits. ACH transfers don’t come with high fees and transactions and they’re easily edited if an employer wants to adjust payroll, extend bonuses, or reimburse an employee.

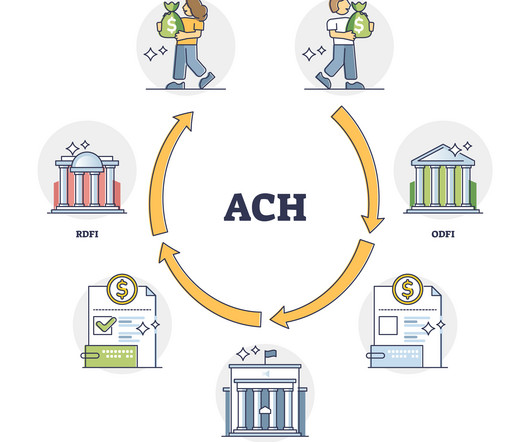

So, what is an ACH deposit? ACH direct deposits are common. Your paycheck, taxrefund, or even a government benefit could be sent to you this way. Understanding the ACH deposit meaning is important because it’s a fast, secure, and cost-effective way to transfer money. But, why does this matter?

It’s like a direct deposit from one account to another, but unlike wire transfers, they are not subject to a fee by the processing banks. Many businesses prefer ACH credit payments for paying suppliers or vendors, especially when the amounts vary or when the payments are made irregularly. Health insurance and premiums.

Last week, NACHA issued an ACHoperations bulletin announcing the delay of the rollout of a third Same Day ACH (SDA) processing window by six months, to March 19, 2021. Or that wire transfer revenues could be cannibalized as end users are incented to shift payments to RTP. A Couple of Important Dots.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content