This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

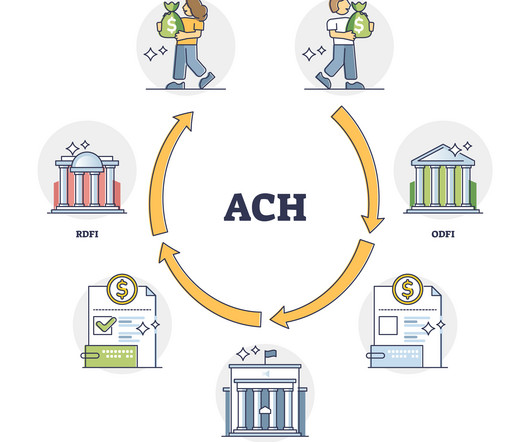

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financial institutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

And on that note, two of the most common modes of electronic funds transfer are ACH and wire transfers. In this post, we’re going to review ACH and wire transfers, look at their similarities, and then see how they compare against each other. A typical ACH transaction is like a machine with multiple moving cogs.

NACHA — The Electronic Payments Association — announced that its membership has approved three new rules that will expand Same-DayACH for all financial institutions and their customers. The expansion of Same-DayACH will be made possible through the creation of a new Same-DayACHprocessing window by the two ACH Network operators.

ACH fees may not seem like much, but they can make a big difference for even the most prominent businesses. While ACH transactions are everywhere these days, understanding these fees can still feel like navigating a maze. What is ACH? What are ACHprocessing fees?

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACH network in a single transaction or within a specified period. This article will shed light on what ACH transactions are, the nature of their limits, and the influencing factors. What is an ACH transfer?

You’ve probably heard the term “ACH deposit,” but what does it really mean? ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? ACH direct deposits are common. What Is an ACH Deposit? So, what does an ACH deposit mean?

Automated Clearing House ( ACH) transfers have revolutionized the way we handle our finances, offering a convenient and secure method to send and receive money electronically. Whether it’s receiving your paycheck through direct deposit or paying your bills online, ACH payment solutions have become an integral part of our daily lives.

In fact, he said, they often create even more friction for small businesses because of interchange fees that can tack on a 3 percent processing charge for each of those dozens, or even hundreds, of transactions. Alas, ACH is a far-from-perfect payment rail, Koeppel admitted. We would love [ real-time ACH ]. “We

13, 2018, NACHA , the rules and standards body for the ACH network, announced that its voting members had approved amendments to the NACHA Operating Rules & Guidelines to establish a third Same DayACHprocessing and settlement window,” the Federal Reserve wrote in the announcement. “On Sept.

With the use of cash dwindling as a payment preference, debit and credit cards and ACH take over as the predominant payment methods. ACH debit payments allow donors to give directly from their bank account. This is done by using an e-check, which is a payment that goes through the automated clearing house (ACH).

Remember, if it takes a few businessdays to resolve an issue with invoicing or processing your credit card transactions, not only could you lose out on valuable revenue, you could damage your customers’ trust in your business. Then, look into reviews regarding their turnaround time on support requests.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content