This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). EFT and ACH payments are fast, secure, and hassle-free. EFT and ACH offer more security and convenience than cash and checks, but they also come with limitations.

Understanding ACH credit payments means understanding the way in which different types of ACH payments are processed in the US banking system. ACH credit payments differ from ACH debit payments and both are distinct from credit and debit card payments. Learn More What are ACH Credit Payments?

As transactions evolve, merchants often find themselves torn between Automated Clearing House (ACH) payments and credit card processing. Understanding how these payment methods operate and the benefits and disadvantages of each can help you determine which is best for your business to significantly enhance your bottom line.

And on that note, two of the most common modes of electronic funds transfer are ACH and wire transfers. In this post, we’re going to review ACH and wire transfers, look at their similarities, and then see how they compare against each other. A typical ACH transaction is like a machine with multiple moving cogs.

This article goes into the details of ACH and wire transfers, providing business owners and merchants with insights into their real-world applications. When it comes to electronic payments, two major players stand out in the United States: ACH transfers and wire transfers. of the total amount being transferred.

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financial institutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

ACH payments are a convenient way for business owners, individuals, and employers to use intuitive automated banking throughout their daily lives. Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACH network provides.

ACH transfers, or payments made through the Automated Clearing House network, account for billions of dollars in payments annually. In fact, NACHA, the nonprofit that governs the ACH payments network reported 6.1% The average consumer commonly uses the ACH network for automated bill payments and larger transactions. in Q4 2021.

If you’ve been accepting and using electronic payments in your business, you’ve probably come across two of the most popular terms in the digital payments scene— automated clearing house (ACH) and wire transfer. International wire transfers can take up to 7-10 days Costs and fees Around 1% of the payment amount.

NACHA — The Electronic Payments Association — announced that its membership has approved three new rules that will expand Same-DayACH for all financial institutions and their customers. The expansion of Same-DayACH will be made possible through the creation of a new Same-DayACH processing window by the two ACH Network operators.

ACH fees may not seem like much, but they can make a big difference for even the most prominent businesses. While ACH transactions are everywhere these days, understanding these fees can still feel like navigating a maze. What is ACH? What are ACH processing fees?

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACH network in a single transaction or within a specified period. This article will shed light on what ACH transactions are, the nature of their limits, and the influencing factors. What is an ACH transfer?

You’ve probably heard the term “ACH deposit,” but what does it really mean? ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? ACH direct deposits are common. What Is an ACH Deposit? So, what does an ACH deposit mean?

What are ACH payments? ACH (Automated Clearing House) payments are electronic fund transfers that use the ACH network to move funds between bank accounts in the United States. This payment method is widely used for direct deposit of payroll, payment of bills, and business-to-business payments.

Automated Clearing House ( ACH) transfers have revolutionized the way we handle our finances, offering a convenient and secure method to send and receive money electronically. Whether it’s receiving your paycheck through direct deposit or paying your bills online, ACH payment solutions have become an integral part of our daily lives.

Automated Clearing House (ACH) payments have become increasingly popular among growing businesses, for their faster processing times, lower fees, and reduced risk of fraud. However, managing ACH payments can be a challenging task for AP teams, especially when dealing with multiple vendors and payment preferences.

But, just as keeping a subscription on automatic renewal without oversight can be a costly mistake, so too can mismanaging recurring ACH transactions. What are ACH Payments? ACH payments are generally fast during the work week but aren’t instantaneous.

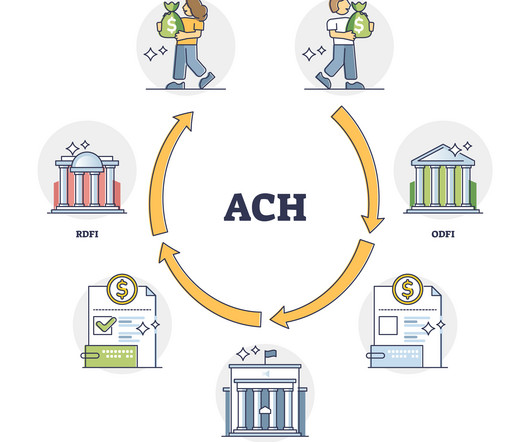

Below, you will find all the information you might need about ACH transactions, in which those codes are used, as well as what they are, and share with you some real life examples. . ACH Transactions – What To Know. When it comes to an ACH transaction, there are two main participants.

The Automated Clearing House (ACH) payment system facilitates the movement of billions of dollars every day, operating behind the scenes in the U.S. In this article, we'll explore the ACH network and ACH payments, how ACH payments function, and the ways in which it impacts our daily financial transactions.

Automated Clearing House (ACH) transactions are revolutionizing how businesses and consumers transfer money, offering a variety of payment types to meet diverse needs. Recognizing the different types of ACH payments and their relevant codes is crucial for navigating this complex landscape. What are ACH payments?

What is an ACH transfer? ACH (Automated Clearing House) payments are basically EFTs ( electronic fund transfers ) that use the ACH network to move funds between bank accounts in the United States. ACH is most commonly used for direct deposit of payroll, payment of bills, and business-to-business payments.

Clearing is typically performed by financial institutions or central banks using payment systems like the Automated Clearing House (ACH). While clearing timeframes can vary, they usually align with the settlement cycle, which indicates the number of businessdays required to finalize a transaction.

Ach and Wire are two of the most popular ways of money transfer in the United States. You will have to make a choice based on your personal or business requirements. What is ACH? This payment method is widely used to directly settle payroll, bills, and business-to-business payments. What is a Wire Transfer?

Batching: The merchant compiles authorized transactions into a batch throughout the day. At the end of the businessday, this batch is submitted to the acquirer for processing. For instance, credit card payments often settle faster than Automated Clearing House (ACH) transfers or other methods.

Small business lending platform OnDeck is accelerating access to capital for its users through the launch of a same-day funding option. local time, as per National Automated Clearing House Association (NACHA) caps, as long as small businesses complete their booking or line of credit draw by 10:30 a.m. on a businessday.

Increased payment flexibility: Businesses can accept various payment methods, including credit, debit, and Automated Clearing House (ACH) /eCheck payments. and ACH/eChecks for direct bank transfers. Depending on the gateway, bank policies, and transaction type, this can range from instant to several businessdays.

These can include using a credit or debit card, an electronic check, or an ACH (Automated Clearing House) transfer. For businesses, your direct deposit service provider will typically set up ACH transfers to pay your employees. What’s the Difference Between EFT and ACH Payments? History of EFT Payments.

In fact, he said, they often create even more friction for small businesses because of interchange fees that can tack on a 3 percent processing charge for each of those dozens, or even hundreds, of transactions. Alas, ACH is a far-from-perfect payment rail, Koeppel admitted. We would love [ real-time ACH ]. “We

Gu said the company typically makes its payouts with ACH transfers instead of relying on checks. Same-dayACH deposits money straight into a customer's account, and funds usually appear the next businessday. Around 67 percent of Upstart loans, in addition, are fully automated on the platform.

Key regulations governing EFT payments include the National Automated Clearing House Association (NACHA) rules, which establish guidelines for ACH transfers, and the Payment Card Industry Data Security Standard (PCI DSS), which sets security standards for handling card information. Q: How do businesses implement EFT payments?

The significance of EFT transfers lies in their ability to facilitate immediate access to funds on nearly any given businessday. This immediate access is essential for both individuals and businesses to manage cash flows , make timely payments, and maintain financial stability. What is the Electronic Funds Transfer Act (EFTA)?

13, 2018, NACHA , the rules and standards body for the ACH network, announced that its voting members had approved amendments to the NACHA Operating Rules & Guidelines to establish a third Same DayACH processing and settlement window,” the Federal Reserve wrote in the announcement. “On Sept.

Merchant service accounts and how they work Merchant service providers assess your credit history, business type, and expected transaction volume during application. This bank account holds customer payments for 1 to 2 businessdays before transferring funds to your business bank account. ACH transactions), and more.

(The Paypers) Dwolla `s Same DayACH pilot programme has been launched in the US to transfer funds from one bank account to another within the same businessday through an API endpoint.

What is an ACH transfer? Automated Clearing House (ACH) transfers are a common form of EFT payment that facilitate the movement of funds between financial institutions in the U.S. ACH transfers are common for low- or mid-value payments that don’t require immediate settlement. Most other forms of EFT vary in speed.

Paper Check Comparison Benefits for Businesses Common Questions About eCheck Payments Getting Started with eCheck Payments Key Takeaways eCheck payments are electronic versions of paper checks that process funds through the ACH network Businesses save 60-80% on transaction fees compared to credit card payments Processing typically takes 3-5 business (..)

Corporate buyers that pay vendors, meanwhile, might seek to satisfy these business partners by delivering money via same-dayACH or over the RTP network. You can do standard ACH that’s free and it’s slow, or you can step up and go to same-dayACH or RTP,” she said. “It Managing Cash Flow Reporting in B2B.

The company noted there are 100,000 Visa cardholders who already use the SoLo Funds platform, which allows users to request and receive a P2P loan of less than $1,000 within minutes – faster than traditional ACH bank transfers, which can take up to three full businessdays to settle. “By

Here are some of the most common: ACH (Automated Clearing House) Transfers Wire Transfers Credit Card/ Debit Card Transactions as EFT Mobile Payments Electronic Checks (eChecks) Point-of-Sale (POS) Payments Direct Deposits Recurring Payments EFT accounts can be checking or savings.

Here are some of the most common: ACH (Automated Clearing House) Transfers Wire Transfers Credit Card/ Debit Card Transactions as EFT Mobile Payments Electronic Checks (eChecks) Point-of-Sale (POS) Payments Direct Deposits Recurring Payments EFT accounts can be checking or savings.

Digital methods for health insurance payments are on the rise, though, with claims processed via ACH payments now accounting for approximately 80 percent of all healthcare transactions. Many begin their move to electronic disbursements by creating support for ACH payments that are directly deposited into patients’ bank accounts.

When your business wants to make a check payment, ACH transfer, or process a transaction through its bank, it’s essential to understand bank cutoff times and their implications on the efficiency and timing of your financial operations. Any transactions made after this cutoff time are typically processed on the next businessday.

An eCheck is often referred to as a direct debit, ACH payment, or ACH transfer. With an electronic check, money is electronically transferred from the payer’s checking account to the seller’s checking account, where it is directly deposited after passing through the national ACH network. Name and address of your business.

Gu recently spoke with PYMNTS about how same-dayACH and other digital disbursements are affecting the lending industry, as well as why lenders should focus on security and data protection as payment speeds increase. Upstart makes the vast majority of its payouts via same-dayACH transfers rather than relying on checks, Gu explained.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content