This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Since each player sets its own rates, credit card processing fees can vary based on your choice of credit card processing service provider, their fee structure, and the types of transactions you process. Interchange and assessment fees are set by card networks and are non-negotiable. Chase, Bank of America, etc.),

The role of the BIN extends beyond simply identifying the cardissuer; it affects various aspects of the payment process: Transaction Routing : When a customer makes a purchase using a card, the payment processor uses the BIN to route the transaction to the right financial institution. Why is the BIN Important in Payments?

Chargeback Process When a cardholder disputes a credit card payment, the chargeback process is set in motion. The cardholder contacts their credit cardissuer, providing details of the disputed transaction and the reason for the dispute. Credit cardissuers must comply with the FCBA guidelines when processing chargebacks.

wrote to Visa on Tuesday to denounce an alleged new fee assessed by the company on credit and debit cardissuers that see their business shift to a competing card network. Dick Durbin, D-Ill.,

In a press release , the FTC said that it periodically reviews all of its rules and guidelines and wants comment on whether any modifications need to be made to the Red Flags Rule and the CardIssuers Rule. It noted that identity theft was the second largest category of consumer complaints made to the government agency in 2017.

As someone who has worked in fraud detection and mitigation for more than 30 years, I wanted to share some important facts on how banks and cardissuers protect their customers from fraudulent transactions: with multiple defenses that are often invisible, and more importantly, often intentionally frictionless.

Understanding Credit Card Processing Fees There are three main components to credit card processing fees. Understanding each of them is critical to learning how to lower credit card processing fees. Interchange Fees This fee is set by credit cardissuers like Visa, MasterCard, Discover, and American Express.

It is thus up to cardissuers and payment professionals to protect their data by carefully monitoring ATMs for unwanted hardware and other fraud tools. . Skimming can be almost impossible to detect, and cardholders often do not realize their information has been stolen until long after the fact.

Credit offerings mean the cardissuers — not the consumers — are the ones risking their money, should the other party turn out to be fraudulent. Nubank assesses customers’ behaviors from the point of credit card application and throughout the customer relationship to maintain clear pictures of risks.

Debit cardissuers face an ever-growing array of fraud schemes perpetrated against them and their account holders. Effective card offerings require financial institutions (FIs) to quickly and accurately detect myriad forms of fraud, forcing them into a delicate balancing act.

From coordinating a team of newly remote workers to assessing new business models, the coronavirus pandemic is drastically disrupting the way organizations run and it is forcing a complete rethink of almost every aspect of operations — payments included. A Surge In Commercial Card Interest.

Rewards and benefits programs: MCCs are key in rewards and benefits programs since credit card companies often offer cashback or points based on the category of purchase. For example, if your card has a home improvement benefit, you may get extra points for shopping at a wallpaper store. MCCs help enforce these restrictions.

It provides merchants with an overview of their payment activity and helps assess overall business performance. By analyzing AOV alongside transaction volume, merchants can assess the effectiveness of marketing campaigns, pricing strategies, and upselling techniques.

What are virtual credit cards? Virtual credit cards, as their name implies, are digital versions of credit cards. There is no physical card. Theyre linked to the customers account through their cardissuer and used (primarily) for online purchases. How do customers pay with a virtual credit card?

When you run any BIN number through a checking system, you end up with accurate information about the geolocation, cardissuer, and card type. Since online banking systems have become more popular and virtual cards have become a norm, BIN numbers aren’t necessarily bank-issued. Why is there an 8-digit BIN number?

It also ensures that data security best practices, particularly PCI DSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data.

In addition to issuer processing, SetldPay will also benefit from Tribe’s proprietary Risk Monitor platform, which allows for real-time assessment of card transactions against an array of pre-defined conditions, along with the real-time assessment against global sanctions, PEP and Adverse Media databases.

TL;DR Understanding how credit card companies charge merchants is crucial for optimizing costs and enhancing customer experience. Credit card fees, including interchange, assessment, and payment processor fees, impact businesses on a per-transaction or recurring basis. Usually, interchange fees will range between 0.3-2%

Here are five common payment processing fees to be aware of: Credit card processing fees: Credit card processing fees are the fees merchants pay to accept credit card payments from customers. The total cost varies based on factors like the type of card used, the transaction method, and the merchants industry.

Interchange fees are set by credit cardissuers, such as Bank of America, Citi, or Chase, and are adjusted every year in April and October. Assessment fees Assessment or network fees are directed to the credit card network- Mastercard, Visa, American Express, and Discover, to help settle costs associated with maintenance and operation.

Let’s start with the elephant in the room: are debit card surcharges legal? The short answer is no, it’s not legal to surcharge debit card transactions. Major cardissuers, including Visa and Mastercard , expressly forbid surcharging debit card transactions. How much do debit card transactions cost?

How Merchant Fees Are Made Up The unavoidable basics of credit card processing fees are interchange rates and assessment fees. Interchange Fees Although interchange fees go toward paying the issuing banks, the major credit card networks — Visa, Mastercard, and the likes — control the interchange rates.

This year, the startup raised US$6 million in seed funding and secured a license from the Bangko Sentral ng Pilipinas (BSP) to operate as a non-bank credit cardissuer. Jenfi uses a proprietary risk assessment engine that evaluates both a business’s creditworthiness and its marketing growth efficiency. With a US$6.6

Resolving disputes can be time intensive, forcing banks to take on the administrative tasks required to gather and assess evidence. Cardissuers that believe chargeback claims are valid then ask merchant acquirers to send funds on behalf of merchants to cover the transaction reversals — unless the sellers wish to dispute the claims.

This involves using a physical point-of-sale (POS) terminal to process card payments. How It Works The customer swipes, inserts, or taps their card on the POS device. The terminal communicates with the cardissuer to approve the payment. How It Works Customers enter their card details during checkout.

Address Verification Service (AVS) A fraud prevention tool that checks the billing address provided by the cardholder against the address on file with the cardissuer. Annual Percentage Rate (APR) The annual interest rate charged by a credit cardissuer on outstanding balances.

The company offers a SaaS solution that manages all of the significant aspects of program management for cardissuers and BIN sponsors in a single interface. A pair of Canada-based Finovate alums – Coconut Software and PayTic – have earned spots in the first cohort of the UK Fintech CTA program.

This is happening at the present as the cardissuers become more aware of the need for businesses to get hard cash. Try your card. Cardissuers have enormous un-utilized credit, [and] this is a way of making it work for them.” Your 1040 and Self Assessment return will be next. Tax return late?

Conduct regular internal audits—preferably on an annual or biannual basis—to assess ongoing compliance with federal regulations. It’s mandatory for all merchants and service providers that accept credit card payments. PCI DSS requirements Businesses must complete a self-assessment questionnaire (SAQ) as part of the validation process.

Better security comes from better communication, and the fraud teams at businesses must speak with all parties involved in a transaction — cardissuers, merchants and the payment processors that connect them — that can benefit from sharing insights about consumers.

Breakdown of credit card processing fees Credit card processing fees are charged to merchants for each credit card transaction processed. Assessment fees Assessment fees are relatively small but consistent fees charged by credit card networks like Visa, MasterCard, American Express, and Discover.

Superior fraud detection is achieved by analyzing an abundance of transactional data in order to effectively understand behavior, and assess risk, at an individual level. It pools the f raud and non-fraud data from thousands of cardissuers worldwide to build the best training set in the industry for machine learning and AI models.

The complaints vary in their specifics, but all revolve around a basic premise: The old credit-scoring models are too backward-looking in a world where real-time data is available — and they are insufficient to the task of properly assessing risk. Aire, though, is a credit-assessment platform intended to fill in that extra data.

TL;DR Surcharges are additional fees that a business adds to a customer’s bill when they choose to pay with a credit card. These fees help the business offset the cost of credit card processing fees, which the merchant typically has to pay to the cardissuer and payment processor.

Learn where your money goes by looking up interchange and assessment fees. They are a fixed credit card processing expense, and they’re the same for all processors. Assessments are also a series of rates and fees charged by Visa and MasterCard, and they are the same across the board.

23, 2015, and June 14, 2016,” but also assessed that “most of the systems were affected during a shorter time frame,” according to a statement on the Omni corporate website. The firm had been working with payments processors and also cardissuers on investigating the Omni breach.

Separately, she said, issuers report roughly 60 percent of disputed transactions reviewed across Ethoca Eliminator in the call center channels (a tool that arms cardissuer agents with the merchant purchase information they need to alleviate cardholder transaction confusion when they call in) are resolved without resorting to chargebacks.

3DS is a messaging protocol that allows consumers to authenticate themselves with their cardissuer when making card-not-present eCommerce purchases. EMVCo is collectively owned by American Express , Discover , JCB , Mastercard , UnionPay and Visa , and focuses on the technical advancement of the EMV Specifications.

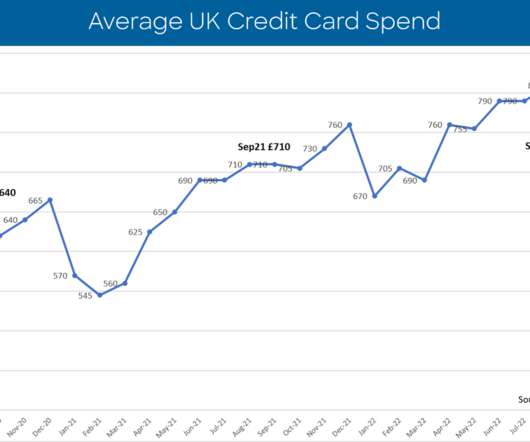

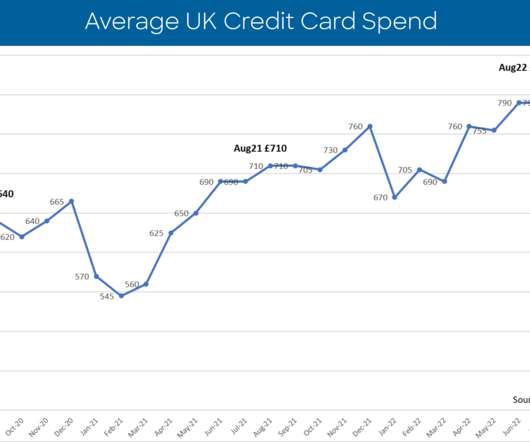

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

8) said that Commonwealth Bank of Australia (CBA) Chief Executive Matt Comyn is speaking out against efforts to nix interchange fees on electronic card payments. According to Grant Halverson, CEO of McLean Roche Consulting, interchange fees from commercial card payments account for more than $46 billion in revenue for cardissuers.

Cardissuers that are convinced of their customers’ truthfulness ask merchant acquirers to extract money from sellers’ accounts, which can then be used to refund consumers for disputed purchases. Keeping retailers and consumers satisfied thus requires quickly and accurately assessing chargeback filings. Combining Friendly Fraud.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK cardissuers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80%of UK cardissuers. .

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content