This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The merchant underwriting process is a critical step that payment processors and financial institutions use to assess the risk associated with onboarding new businesses. Key steps include application review, risk assessment, credit checks, and compliance verification. Learn More What is Merchant Account Underwriting?

But after years of finding SMBs too unprofitable to finance, lenders have to play catch-up to develop better underwriting processes for greater accuracy and efficiency. “But at the same time, they have all lacked a credible tool to conduct an assessment of these [SMBs] in an independent way.”

Appian, a software company that automates business processes, and Swiss Re have expanded their partnership to streamline the life insurance underwriting process and enhance the productivity of underwriters. The workbench addresses this by offering a single login system, enabling underwriters to manage their tasks more efficiently.

From there, your users must go through an application and underwriting process that determines their eligibility to accept payments. TL;DR Merchant underwriting is the risk level assessment process an acquiring bank carries out on every new merchant before they grant them a merchant account. What Is Merchant Underwriting?

ChAI Protect is already utilised by large publicly traded firms and is underwritten by tier one, A-rated, underwriters. This innovative price risk insurance will be of most value for raw materials where hedging is currently not possible, as no accessible derivatives markets exist.

Merchant underwriting is an essential component of the payment processing industry, ensuring the safety and security of electronic payments. This article will explore the mechanics of merchant underwriting, from the essential steps involved in the process to the factors influencing it. What is merchant underwriting?

Traditional (manual) underwriting processes often struggle to keep pace with the growing complexity of modern risk assessment, data collection, and policy management. These include customer applications, financial records, medical reports, and external risk assessments such as geographic or weather-related data.

Alternative lending companies are one of the strongest examples of how leveraging rich financial transaction data can be used to go beyond traditional credit risk assessments, says Finsync's Eddie Davis.

SBCA uses anonymized, item-level transaction data to help lenders assess small business financial performance, enabling faster underwriting, reduced risk, and improved loan terms. “SBCA is a game-changer, offering unparalleled insights into small business performance.

Automation can have a significant impact on this process—particularly the loan underwriting process. Loan underwriting is the step before a loan is approved or denied, where a lender verifies a potential borrower’s income, assets, debt and property details in order to issue final approval for the loan.

Inaccurate and slow credit risk assessment for [small- to medium-sized business (SMB)] commercial loan requests is one of the major reasons that over 50 [percent] of loans are currently declined by financial institutions (FIs),” said Roger Vincent, chief innovation officer at Trade Ledger.

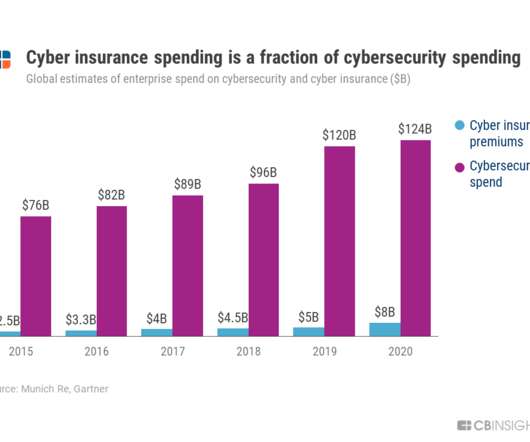

It is also an important assessment tool for third parties such as potential business partners and, notably, cyber insurance providers. The number of underwriters active in the US market is growing rapidly as well, with a double-digit CAGR. The lingua franca of cyber breach underwriting .

This includes employing machine learning algorithms to automate parts of the loan application and underwriting process, as well as using digital platforms to facilitate communication between borrowers, lenders, and other relevant parties. “One-click” loans become reality through instant credit assessments.

Open data, in turn, enriches these offerings, enabling innovative credit scoring and risk assessment beyond traditional banking channels. By combining payment flows with broader financial datasuch as rental history, savings patterns, and income variabilitylenders can offer dynamic, real-time credit assessments.

The plan, which illustrates the growing dangers of hacking, is meant to create an assessment system for the most viable cybersecurity defenses available to businesses. The participating insurers so far include Allianz , AXA SA, Axis Capital Holdings, Beazley, CFC Underwriting, Munich Re, Sompo International and Zurich Insurance Group.

But the reality is that–at the time–credit scores were simply the best thing an insurer could access in order to assess risk. Technology has evolved to provide real-time financial data to institutions, facilitating more accurate assessments of both creditworthiness and risk. There is a correlation , i.e,

A combination of superior risk assessment, fraud detection capabilities, and quick and accurate underwriting turnaround can transform a lender’s success rate with borrowers and reduce non-performing assets. The revenue growth and profitability of a lending business depend on several factors.

These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing credit risk. percent employ it for credit underwriting. percent reported using AI for underwriting and risk assessment purposes. Among banks that use AI, 92.9 percent do so in payment services, and 71.4

Affirm underwrites every individual transaction before making a real-time credit decision and only approves consumers following an assessment that evidences their ability to repay. Affirm’s expansion to the UK adds to its presence in the US and Canada.

FICO Applauds FHFA Inclusion of Rental Data in Underwriting. Last week, the Federal Housing Finance Agency (FHFA) announced that Fannie Mae will begin considering borrowers’ rental payment history in its risk assessment process. We share the assessment that the key to expanding access to credit is seeking alternative data.

Mastercard’s Small Business Credit Analytics provides lenders with data-driven insights, with the consent of the business, to help assess the financial performance and retail sales of small businesses.

Equipment finance company CapX Partners has announced an integration of Moody’s Analytics technology to strengthen its underwriting and risk mitigation capabilities. “Assessing the creditworthiness of small businesses in a cost-effective manner is one of a lender’s most challenging tasks,” he said.

It integrates an advanced cyber risk exposure scanning solution into the underwriting process. This technology enhances risk assessment by generating a real-time security posture score within a minute, allowing eligible small and medium-sized enterprises to obtain instant policy issuance in under 10 minutes.

We explore the innovations in personalised insurance products, the role of IoT devices in data collection and risk assessment, and the challenges faced by established insurance companies integrating new technologies. Enhanced Risk Assessment IoT data provides insurers with a more accurate understanding of risk profiles.

However, with a lack of reliable information available to feed into the underwriting process, how can insurance companies find an accurate way to assess the policy buyer’s risk profile? This is especially true for smaller firms where lower premiums will dictate a lower-touch, lower-cost assessment of risk during underwriting.

“Open Banking sits at the core of SME credit decisioning and brings confidence to underwriting risk assessments,” Capitalise Co-Founder Ollie Maitland said. Plaid reported that adoption of open banking by U.K.-based based SMEs has increased by 18% year-over-year.

Bloomberg is providing the data in the current global economic crisis to aid the markets with ready, accessible information that is timely and transparent for active credit assessments and predictive models to assess the volatility of the current market. They can also assess ongoing credit quality.

The introduction of the score has enabled Home Credit to underwrite and evaluate new clients with a thin file more objectively. This has been a big focus for the business in response to strong market demand for consumer loans in China. For its achievement, Home Credit was awarded the 2019 FICO® Decisions Award for Financial Inclusion. “By

Providing consumers with sufficient supports can address these potential obstacles and speed up loan underwriting timelines, benefiting both borrowers and lenders. Consumers must give approval to have these details sent, which helps lending FIs quickly assess potential borrowers and determine whether to offer loans.

But SMB loan underwriting at traditional FIs has, for the most part, remained unchanged, even as alternative lenders began exploring the role of alternative data in the risk mitigation process. “Lenders’ primary goal is to assess a consumer’s stability, ability and willingness to pay.

.” Flood risk Bob Schiller , director of product innovation at insurer SageSure addresses the significant gap in flood insurance coverage by highlighting the role of data in accurately assessing flood risk and facilitating insurers’ adaptation to evolving risks. times more properties that have substantial flood risk.

“By analysing big data and rapidly assessing risks, AI empowers financial companies to make well-informed decisions. However, a significant revolution lies ahead – the personalisation of services based on individual user assessments. “Finally, AI is reducing risk in the embedded insurance space.

This will impact how banks and fintechs use AI for customer interactions, underwriting, and fraud detection. Therefore, banks using AI systems must assess and reduce risks, maintain use logs, be transparent and accurate, and ensure human oversight.

Faster payment services could help such consumers get much-needed funds, as long as lenders can access equally fast underwriting tools. Underwriting tools boost the confidence of both borrowers and lenders, and help the latter more seamlessly access reliable bank data that supersedes credit scores. A Complete Banking Picture.

Bloomberg is providing the data in the current global economic crisis to aid the markets with ready, accessible information that is timely and transparent for active credit assessments and predictive models to assess the volatility of the current market. They can also assess ongoing credit quality.

Technology firm Microsoft is working with Axis Bank and Aditya Birla Capital, among others, to deploy processes using genAI to transform contact centers, boost sales and overhaul claims and underwriting processes. The book size of digital lenders in India is projected to grow from US$38.2

He offered the example of banks using analysis of financial statements to assess risk in the loan origination process. “This disconnect of all the different teams involved in the underwriting process is not just with the physical handoffs, but it also includes the data and analytics separations as well,” he stated.

By leveraging data sources across 220 countries & territories, the collaboration will provide region-specific solutions and access to business-relevant data along with documents and risk assessment models to help FIs onboard clients, vendors and dealers digitally and securely.

Allianz and Munich Re will integrate with Google Cloud in order to access customers’ data in order to better assess the cyber risks they face and provide more personalized protection. Other information like if the company uses 2-factor authentication will also be provided for underwriting purposes.

Jenfi uses a proprietary risk assessment engine that evaluates both a business’s creditworthiness and its marketing growth efficiency. This integration provides Jenfi with real-time data on a company’s revenue growth and marketing return on investment, enabling continuous monitoring and fast underwriting decisions. With a US$6.6

A survey by Accenture on underwriting employees found that up to 40% of underwriters’ time is spent on non-core and administrative activities. Risk Assessment and Compliance Prediction: AI can assist in proactively identifying potential compliance risks by analyzing historical data and patterns.

By leveraging line-by-line transaction data, Recap’s credit risk engine can assess a merchant and return a funding offer in under two minutes without any further underwriting requirements such as a credit check on the owner or management accounts or business bank statements.

Underwriting and claims automation. Why it matters: Insurers can use geospatial analytics to quickly and accurately underwrite policies and virtually assess claims for property insurance without needing in-person inspections. What’s next: Underwriting and claims teams have prioritized geospatial analytics in recent years.

” With ZestyAI models, carriers are able to move from territory-based segmentation to a property-by-property risk assessment. They also benefit from enhanced underwriting and portfolio optimisation and can more accurately align policies with coverage needs. “Amica earned the top spot in the J.D.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content