This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Financial institutions are trying to crack a data problem, and there is news from the world of fraudprevention. 30: Transactions under this amount are exempt from Strong ConsumerAuthentication. Data: 10 percent: Amount of FI data that contains personally identifying information.

So before we add another layer of authentication , we should ask, is this actually going to serve a purpose or solve our problem?”. What is necessary, said Xie, is a different, more holistic paradigm for fighting fraud – with a broad goal of not adding more authentication steps, but fewer. The Zero-Authentication Future.

22) that it has rolled out two enhanced consumerauthentication solutions, step-up authentication and identity verification, to mitigate card fraud within call centers. In a press release , Fiserv said the two new solutions expand beyond knowledge-based consumerauthentication that can be vulnerable to fraud.

That’s why fraud is always about identity.”. That’s Michael Reitblat, the CEO of Forter, a fraudprevention platform whose business is designed to make it harder for fraudsters to use those easy-to-come-by identities at a merchant. The Fraud Migration Trail. Anywhere that they happen to be transacting. ” she added.

The eCommerce fraud protection company, headquartered in Cleveland, Ohio, announced last Friday (Nov. 11) that it will be making its eCommerce authentication (CCA) platform available to thousands of small, emerging businesses; independent retailers; and entrepreneurs looking to get a piece of that $117 billion holiday pie.

For the eighth edition, Paladin has created a fraudprevention industry report with 15 solution providers for in-depth information—and researched an additional 40 solution vendors, to compile the most comprehensive snapshot of the fraudprevention industry to date. The report uses six categories to group vendors.

Strong consumerauthentication comes in several forms, and it’s time to pick one. “A This risk-based approach is key to detecting and stopping ATO attacks as well as preventing fraudsters from altering accounts to extend takeover while providing good [customer experiences] for [genuine] clients.”.

The foreseeable changes stem from the already delayed strong customer authentication (SCA) regulations that are due to go into effect in Europe by the end of the year. Under the new SCA rules, merchants will need to be able to securely authenticate every customer before authorizing eCommerce transactions. The Path Ahead.

(The Paypers) iovation , a provider of device reputation and behavioural insights for fraud detection and consumerauthentication, has announced several new capabilities to its FraudForce solution.

In the rush to get new products and services to market, he said, FIs may forget about some of the fundamentals of fraudprevention – and smaller banks and CUs, with relatively scarcer resources than their larger brethren, may find themselves overwhelmed by the challenges of preventingfraud. Proactive FraudPrevention.

includes enhancements to support new authentication procedures for online purchases, which could help stop unauthorized card not present transactions. Its EMV 3-D Secure Protocol and Core Functions Specification v2.2.0

How exactly fraud attacks and fraudprevention will change in the post-PSD2 world remains unclear, but change is certain, according to observers. In fact, call center fraud already costs companies $0.58 The report covers ways in which call center operations are fighting fraud — including in Europe, the home of PSD2.

Many of these consumers are exploring digital banking for the first time, however, and are frustrated by customer onboarding pain points. Time-consumingauthentication methods, redundant application forms and sluggish processes can all drive away potential customers.

Biometrics promise to take a larger role in authentication security in 2019, helping to stop online fraud and bringing speed, efficiency and security to transactions ranging from QSR mobile-order ahead to airport car rentals. Larger Trends. In fact, the Wendy’s fast food chain was recently hit with such a suit in Illinois.

Transaction validation in real time Firms may have difficulty validating incoming payments instantly, especially considering the need to check for insufficient funds and fraud, plus ensure compliance, all in real time. They can also use AI tools for fraud detection to help banks validate transactions without human intervention.

But there are other significant actions that, when implemented as a part of a layered approach to fraudprevention, can make a big difference in protecting consumers and lowering false positives. Discover how Customer Communications Services for Fraud can alert customers about potential scams in real-time. Debbie Cobb.

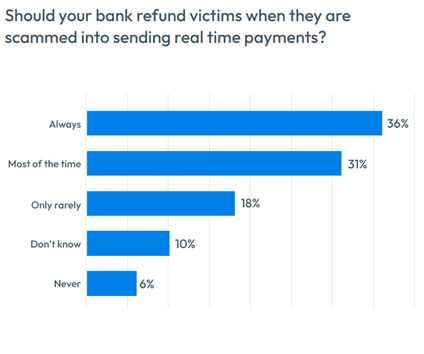

The challenge for banks is balancing the ease and convenience of RTP with fraudprevention for authorized push payment fraud (APP fraud) – without impacting customer experience. Debbie has 25 years product management and product marketing experience in fraud management and financial services. Debbie holds a B.A.

As my colleague Adam Davies, vice president of fraud and identity solutions here at FICO recently noted , “Banks can avoid reputational and regulatory impacts by using the latest in fraudprevention technology, such as the FICO Platform, which can help identify and stop existing and emerging threats before they can impact customers.”

Step Two: Demonstrate the effectiveness of a fraud model that relies upon social data based on a supervised learning approach to identity verification. consumers who were identified using names, addresses, phone numbers and dates of birth (DOB).

While advancements to digital commerce and authentication technology have revolutionized a number of industries, one where their influence is perhaps most visible in the travel sector. Following this ideology, Ziolkowski incorporated 3D Secure technology as the organization’s fraudprevention tool.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content