This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

BNPL (Buy Now, Pay Later) burst onto the scene as a game-changer, transforming how consumers shop and pay over time. What started as a consumer-friendly alternative to traditional credit is becoming a more concrete financing solution in the digital payments ecosystem, particularly in emerging markets like BNPL regulation in Asia.

Buy now, pay later (BNPL) services have become significant in the realm of short-term unsecured consumer finance, often tied to specific products and offering instalment repayments, without accruing interest. The BNPL transaction involves three key players: the consumer, the merchant, and the BNPL service provider.

BNPL fraud in Southeast Asia is seeing a rapid rise with fraudsters exploiting weaknesses in these platforms and developing sophisticated methods to deceive users for financial gain. In these BNPL fraud schemes, borrowers in need of cash agree to use their BNPL credit to pay bills for lenders, expecting a cash transfer minus a small fee.

Abnk , Atome , Grab , and SeaMoney have been awarded the accredited Trustmark by the Singapore Fintech Association (SFA) and the Buy Now, Pay Later (BNPL) Working Group as of 19 April 2024. Buy Now, Pay Later Accredited Trustmark The trustmark signifies a commitment to responsible lending and consumerprotection.

Australia will introduce new legislation to amend the Credit Act, requiring Buy Now, Pay Later (BNPL) providers to hold an Australian credit license and comply with existing credit laws regulated by the Australian Securities and Investments Commission (ASIC). The new laws aim to balance consumerprotection with innovation and competition.

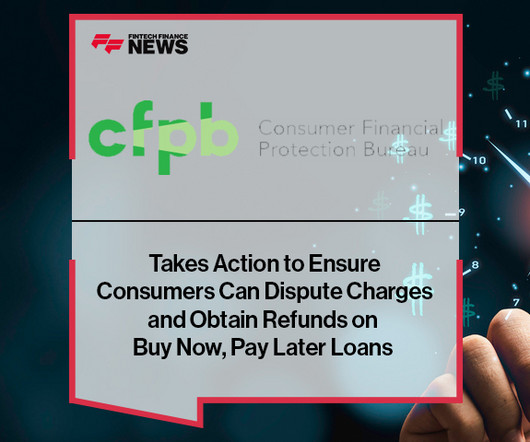

“Whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations,” CFPB Director Rohit Chopra said.

A report this month from the organization outlines a litany of complaints about buy now-pay later, such as hidden fees, and suggests the industry is trying to evade consumerprotection laws.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protectingconsumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections.

The American Fintech Council , the industry association representing responsible fintech companies and innovative banks, has welcomed new recommendations regarding buy now, pay later (BNPL) but warns that providers need more time to ensure compliance.

Regulatory changes in BNPL, cVRPs, and digital wallets aim to boost e-commerce innovation and competition while safeguarding consumerprotection and market stability. Read more

“Regulatory clarity and consistent standards are critical for providers offering safe, transparent and responsible financial services and even more important for consumers who expect protections when utilizing financial services including Buy Now Pay Later,” said Phil Goldfeder, Chief Executive Officer of AFC. “We

While buy now, pay later (BNPL) has enjoyed significant growth in recent years, an air of uncertainty remains around the space – whether that be due to a degree of untrust (seen by some as a debt trap ) or because of increased regulatory pressures being placed on the space. To find out more, we reached out to some industry experts.

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations already on the books.”

Having looked at some of the biggest technologies to impact the payments world, like buy now pay later (BNPL) and central bank digital currencies (CBDCs) , we now look to the future and what the next trend may be.

Over the past decade, the payments industry has developed and deployed AI tools that have made payments faster, more secure, and has unlocked numerous benefits for the payment industry and consumers alike. BNPL is one example of innovation in payments that, when adopted carefully and thoughtfully, provides additional payments choice.

Alternative payment methods like digital wallets, account-to-account (A2A), and buy now, pay later (BNPL) continue to gain popularity. Anil Nanda, Partner and UK & Europe Head of Payments said: “The payments industry is undergoing significant change and disruption.

The OCC outlines safety and soundness principles and appropriate risk management processes for its regulated institutions that engage in BNPL lending. The OCC expects that banks engaged in BNPL lending “do so within a risk management system that is commensurate with associated risks.” By Arthur S.

Late last month, the Consumer Financial Protection Bureau (CFPB) issued an interpretive rule stating that Buy Now, Pay Later (BNPL) lenders are credit card providers. This ruling is slated to have some significant impact on BNPL, which was once one of the hottest subsectors in fintech. territories.

For payments firms, the intersection of payments and credit is becoming a competitive battleground, especially as BNPL and embedded lending scale. While some governments prioritise competition and innovation, others focus on financial inclusion, consumerprotection, or market-driven adoption.

Open banking, BNPL, cybersecurity and AI will all be under the microscope for regulators and policymakers, but not all areas will see major action in 2023. There Will be Changes in the BNPL Market, but Major Regulatory Action Is at Least a Year Away. Consumers will likely see more transparency from industry participants going forward.

The growth in the forecast period can be attributed to expansion of bnpl services to physical retail, growth in cross-border e-commerce, adoption by traditional retailers, emphasis on responsible lending and consumerprotection, rise of embedded finance and bnpl as a service.

As much as a click from the Kardashians helped spread the brand awareness and jump-start his company, Molnar said, as a spending trend among young consumers set the stage for BNPL's success. There are a number of things that intersect here: data, privacy, consumerprotection. These are not easy issues.”.

Democrats and Republicans are going after this from different angles, he noted, but they’re all targeting Big Tech firms in the name of consumerprotection – even though that’s protection that consumers don’t really seem to want. “I He said that going after Big Tech is increasingly becoming a bipartisan issue.

Examples include Split X , offering a buy now pay later (BNPL) solution; TelyPay , providing a secure digital platform for individuals and businesses; and Wadiaa , focusing on crowdfunding and crowd-investing. Several homegrown fintech companies have emerged in Oman, reflecting this evolving landscape.

Phil Goldfeder, CEO, AFC “Under the guise of consumerprotection, these bills in Rhode Island and DC will harm consumers who need access to safe and affordable financial services and will put local state-chartered banks at a disadvantage,” said Phil Goldfeder , chief executive officer of AFC.

“When consumers check out and choose Buy Now, Pay Later, they don’t know if they will get a refund if they return their product or whether the lender will help them if they didn’t get what was promised,” said CFPB Director Rohit Chopra. The Buy Now, Pay Later market has expanded rapidly over the past few years.

The PSR’s chief aim is to improve consumerprotection, and it will introduce changes to the existing open banking framework to improve access to these services. Let’s take lenders, BNPL providers and other credit providers as an example. The PSR The PSR is intended to update and replace the parts of PSD2 not covered in PSD3.

” Is BNPL finally getting regulated? The long debated topic of buy now pay later (BNPL) regulation was discussed on stage at IFGS, with a panel of key industry players discussing how, despite industry feedback, BNPL regulation is still on hold.

million consumers and MSMEs through the platform. This business case was also awarded the Best BNPL solution at Finovate in 2023. They are implementing policies and regulations that promote innovation while ensuring consumerprotection and financial stability. Just in 2023 Yabx disbursed over 20 million loans to 2.4

Other areas that are likely to receive regulatory scrutiny in 2025 in the EU are crypto and Buy Now Pay Later (BNPL). BNPL, however, presents a different regulatory challenge. In many ways, BNPL is just a modern spin on subprime lending a long-standing issue in financial services when it comes to consumerprotection.

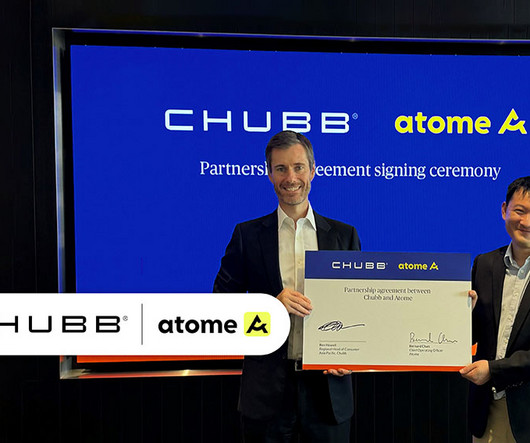

Buy Now, Pay Later (BNPL) firm Atome has teamed up with Chubb to co-create insurance products for its customer base across Singapore, Malaysia, the Philippines, and Indonesia. A second product, named “Shopping Secure,” is slated for release in the second quarter of the year, aiming to further extend consumerprotection measures.

the Consumer Financial Protection Bureau (CFPB) has been studying the BNPL industry since at least late 2021. At this point, much of the CFPB’s impact on BNPL has been minimal. There has some concern at the state level , with state attorneys general voicing consumerprotection warnings. In the U.S.,

AFC underscores how partnerships between regulated financial institutions and responsible fintech companies have fueled the development of transparent, technology-driven products such as responsible fintech loans, high-yield deposit accounts, credit builder tools, earned wage access (EWA), and buy-now-pay-later (BNPL) offerings.

Key developments include progress on stablecoin regulation with draft legislation anticipated, advancements in open banking and variable recurring payments (VRPs), outcomes from the PSR's review on card fees, and the introduction of buy now pay later (BNPL) legislation in Parliament.

Examples of embedded finance include buy-now-pay-later (BNPL) options at checkout and insurance products offered during travel bookings. Clear guidelines are needed to balance innovation with consumerprotection and market stability. This trend is gaining momentum as businesses seek to enhance customer journeys.

The landscape and ongoing tug: As new payment models like Buy Now, Pay Later (BNPL) and EWA took off in recent years, the Consumer Financial Protection Bureau (CFPB) has been watching how they affect consumers. 7428 in 2024, which classifies EWA as a non-credit product with consumerprotections.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content