This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

FV Bank, in partnership with Visa, has today announced at Money20/20 Las Vegas (October 27-30), the launch of FV Bank’s new debitcards and corporate expense cards. Businesses can order cards for authorized users, set individual spending limits, and track transactions in real-time through FV Bank’s platform.

As a merchant, understanding how a PIN (Personal Identification Number) works with credit and debitcard transactions is essential for running a secure and efficient payment process. This guide explains how a PIN functions in credit and debitcard payments and its importance for merchants. What is a PIN?

Collectively, ICBA Payments client banks represent over $43billion in credit and debit sales, $918million in outstandings, with 10 million cards issued, also ranking them as the 10th largest debitcardissuer.

Credit and debitcards have become the preferred payment methods for many, and it isn’t hard to see why. In 2023, 27% of all point-of-sale (POS) payments were made using credit cards while 23% were made with debitcards. This is a win-win situation for issuing banks and credit card payment networks.

While major cardissuers such as Chase and Wells Fargo roll out NFC-enabled credit and debitcards incrementally, Bank of America is taking much more aggressive approach.

New regulations will cap overdraft fees, drastically reducing them from around $30 to approximately $3, significantly impacting banks' revenue streams. Read more

New regulations will cap overdraft fees, drastically reducing them from around $30 to approximately $3, significantly impacting banks' revenue streams. Read more

In the complicated world of payment processing, understanding the nuances of debitcard and credit card payments, along with associated processing fees, is essential for businesses. TL;DR Card brands such as Visa and MasterCard along with state and federal laws prohibit debitcard surcharging.

“Credit and debitcards continue to play a leading role in the payment experience as money moves between banks, consumers, businesses and beyond in a complex, never-ending cycle. In the fight for customer loyalty, every payment card program is a vital opportunity to seize competitive advantage and drive growth.

One of the more notable differences is their tendency to favor credit cards online and other options such as digital wallets over debitcards. Thirty-five percent of credit card users believe they offer protection against theft of funds — twice the share of debitcard users with this same view of the payment method.

Certain prepaid debitcardissuers who didn’t initially adopt EMV technology — because of a lower perceived security threat for these limited-use cards — are now going the EMV route.

Set rate processing Subscription rate processing TL;DR Interchange fees are not collected by your payment processor or bank; they go directly to the card-issuing banks. Interchange fees vary significantly depending on the cardissuer, the issuing bank, type of transaction and/or merchant type.

If your plastic card is captured inside of an ATM, call your cardissuer immediately to report it. Sometimes you may think that your card was captured by the ATM when in reality it was later retrieved by a criminal who staged its capture. Either way, you will need to arrange for a replacement card as soon as possible.

A new study has found that the number of payment cards issued globally reached 14 billion last year and is predicted to rise to 17 billion by 2022, boosted by an increase in overall debitcard issuance. For many, a debitcard will normally be the first card they receive when they enter the banking system.

In payment processing, one component of the payment processing tech stack involving credit or debitcards is the Bank Identification Number or BIN. Card Network : Indicates the card brand, such as Visa, Mastercard, or American Express, helping processors verify the card’s compatibility with their systems.

How Credit and DebitCards Compare The fundamental difference between a credit and debitcard is whose money is being used in the transaction: with a credit card, the consumer is borrowing from the cardissuer , while with a debitcard they are using their own money, stored with the issuing bank.

Bank cardissuers say there isn’t enough network competition to meet the July debitcard routing rule deadline, adopting regulators’ argument to push back.

Consumers have more heavily leaned on debit during the pandemic, with the economic downturn making shoppers more cautious than ever about the prospect of taking on credit card debt. A recent study even estimates that shoppers could ultimately shift $100 billion worth of annual spending from credit cards to debitcards.

Fraudsters have grown adept at finding debitcards’ weak points, and merchants are struggling to keep up. Losses due to false credit and debitcard declines — in which merchants reject legitimate orders on the mistaken belief that they are fraudulent — grew to $118 billion last year and are projected to reach $443 billion by 2021.

In an effort to grow usage of its Android smartphones in Brazil, Google has introduced a debitcard payment program through Google Pay. Reuters is reporting that the company is making the move because many online retailers in Brazil only accept credit cards due to a preponderance of fraud. .

This indicates a shift away from physical debitcard usage toward using debitcards through digital wallets. 66% of Gen Z consumers, among others, are open to switching to digital service providers that offer new or enhanced digital wallet features beyond basic card payments.

GoHenry by Acorns , a debitcard and financial education app designed for 6-18 year olds, has announced a collaboration with Google Wallet to integrate GoHenry into the new Fitbit Ace LTE smartwatch for kids in the U.S.

Citing a growing frustration with how the EMV transition has interfered with merchants' options for PIN debit transaction routing and authorization, the Merchant Advisory Group for the first time is asking federal auditors to examine the practices of some debitcardissuers.

As many of us who have long been in the industry know, fraud remains a top challenge for debitcards. In 2019 issuers faced $4.2 billion in gross (attempted) debitcard fraud and ultimately incurred losses of over $1 billion on debit and ATM transactions; the need for an effective solution to this problem has never been greater.

New Orleans--As credit and debitcardissuers start to see the benefits of EMV-chip card security, prepaid would seem to be the logical next step. But prepaid issuers remain unconvinced of the security benefits of EMV.

Payments provider Elan Financial Services announced that along with Ondot Systems , the leading provider of mobile-based card services, they have enhanced the My Mobile Money app so that it now offers two-way fraud alerts for Elan processed debitcards.

In an effort to grow usage of its Android smartphones in Brazil, Google has introduced a debitcard payment program through Google Pay. Reuters is reporting that the company is making the move because many online retailers in Brazil only accept credit cards due to a preponderance of fraud. .

WASHINGTON, DC — It’s been nearly 15 years since the Durbin Amendment imposed price caps and routing mandates on debitcards, financially burdening small businesses, while corporate mega-stores, like Walmart and Target, have accumulated substantial revenue gains.

Samsung is fond of using cash rewards to drive Samsung Pay signups, offering consumers $25 to $100 in recent months for enrolling a payment card in the handset maker's mobile wallet. But that strategy is not a fit for all cardissuers, according to the fine print in the latest Samsung Pay promotion.

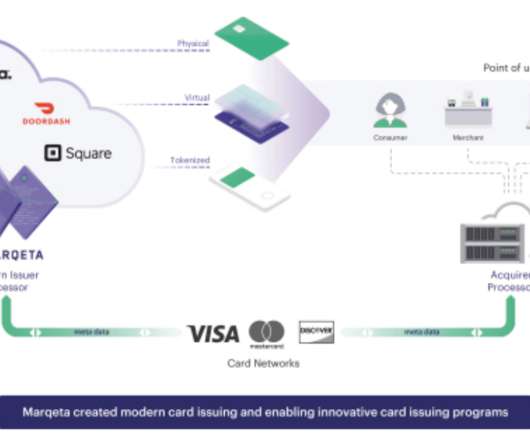

Corporate card providers : This year, Marqeta developed a credit card-issuing platform through a partnership with Deserve to power companies like Brex and Ramp , which leverage Marqeta’s technology to build their own credit card programs. . Digital banks : Square uses Marqeta for its cash app and merchant debitcard. .

. “As of the end of last year, 60% of the physical cards in our network had been transitioned to paper-based materials, and we are well on our way to achieving our original goal of converting 75% by the end of this year. However, it is unlikely we will ever see paper credit or debitcards.

According to the report, citing a senior bank official, the hackers used a malware attack to clone thousands of the bank’s debitcards over the course of two days. The cloned cards were Visa and RuPay debitcards of bank account holders that used the National Payments Corporation of India (NPCI) system, noted the report.

It splits transactions into three types—non-qualified, mid-qualified, and qualified—depending on the credit card type and payment mode used, and charges a different fee for each tier. Payments made with international cards, business cards, and specific high-benefit rewards cards are classified as non-qualified and have the highest fees.

It didn't take long for debitcardissuers affected by the Durbin amendment fee caps to cut back or eliminate rewards programs to recoup costs. Issuers now engaged in the increasingly competitive credit card rewards and loyalty environment may soon have to face that same decision.

The corporate card can have a home in the digital wallet thanks to collaborations and technology platforms designed for cardissuers. Furthermore, the collaboration will grow the reach of Volopay’s cards, letting its corporate customers and their staffers make card payments wherever they conduct business around the globe.

Acumatica allows businesses to accept and process credit cards, debitcards, Automated Clearing House (ACH) payments/eChecks, and other transactions seamlessly by integrating with payment gateways. This is because credit cards, debitcards, and digital wallets have different fees.

(The Paypers) Wirecard has been selected by TransferWise , a UK-based international money transfer company, to issue a debitcard, alongside its existing digital borderless account.

A consumer using a chip and signature card will sign for the purchase. The signature is compared with the one on the back of the card or with the signature stored in the cardissuer’s system. Currently, in the United States, most credit cards are chip and signature, while most debitcards are chip and PIN.

Debitcardissuers face an ever-growing array of fraud schemes perpetrated against them and their account holders. Effective card offerings require financial institutions (FIs) to quickly and accurately detect myriad forms of fraud, forcing them into a delicate balancing act.

Along with that growth in card numbers, said the firm, purchase transactions and volumes are also on the upswing. In a press release detailing the survey results, Entrust Datacard noted that instant issuance technologies were first adopted by smaller banks and credit unions almost a decade-and-a-half ago.

wrote to Visa on Tuesday to denounce an alleged new fee assessed by the company on credit and debitcardissuers that see their business shift to a competing card network. Dick Durbin, D-Ill.,

PYMNTS research has shown that approximately 40 percent of consumers would be very interested in downloading highly functional mobile card apps that can be used to manage multiple cards, track spending and issue transaction alerts, among many other features. There is an important underlying dimension to these findings, however.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content