This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Managing fraud cases has been a top challenge for cardissuers, according to recent studies. Rising operations and outsourcing costs and burgeoning fraud recovery caseloads make it especially challenging for issuers to meet chargeback deadlines and avoid cardholder write-offs.

This is why it’s vital to have a good understanding of: Why credit card chargebacks happen Why they’re becoming more common Steps you can take to reduce chargebacks What to do when you receive a chargeback Luckily for you, that’s exactly what this guide is for. What Are Credit Card Chargebacks?

Credit card network – Mastercard, Visa, American Express, and Discover are the biggest payment networks in the US. They facilitate transactions by connecting merchants, credit card processors, and banks while establishing rules, regulations, and fees for processing payments. Chase, Bank of America, etc.),

Mastercard chargeback reason codes consist of a series of identifiers utilized to categorize various chargeback circumstances, which represent the disagreements raised by cardholders against merchants. These codes play a crucial role in organizing disputes and guiding the subsequent actions required.

A new Mastercard initiative aims to improve online transaction clarity so that customers can know exactly who they purchased from, according to a press release Tuesday (Sept. Global chargeback volume, the study showed, will reach 615 million by 2021, largely coming from customers frustrated and disputing transactions, the release said.

An Overview of AMEX Chargebacks AMEX chargebacks differ from those of other card networks due to American Express’s unique role as both an issuing bank and, in some cases, an acquirer. Win Rates Merchants’ success in disputing chargebacks varies across different card networks.

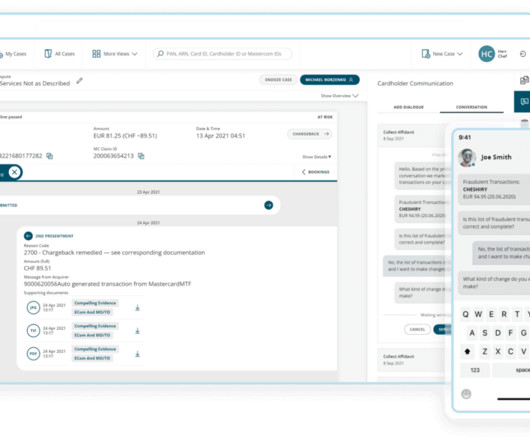

A chargeback is a reversal of a credit card transaction initiated by the cardholder’s bank, usually as a result of a dispute by the customer over the purchase. Key Activities of a Chargeback Team Reviewing Dispute Notices: Receiving and thoroughly investigating dispute notices from credit cardissuers is the first task.

Gan Kim Yong Deputy Prime Minister Gan Kim Yong emphasised the comprehensive security measures already in place, including safeguards implemented by global card schemes such as Visa and Mastercard, alongside cardissuers like banks. Over time, these measures have been strengthened to combat fraud effectively.

In other words, friction with a dash of intelligence mixed into the process can cut down on fraud, which helps, well, everybody in the commerce ecosystem — from consumers to issuers to merchants. Given the trio of acquisitions mentioned, Gerber noted that Mastercard will have a presence in and insight into the continuum of commerce.

Visa chargeback reason codes are a set of codes used by Visa to classify various reasons for chargebacks, which are disputes filed by cardholders against merchants. These reason codes help in categorizing the dispute and determining the appropriate course of action. Other Fraud: Card-Present Environment / Condition 10.4:

Customers of Microsoft can access digital purchase receipts through Canadian tech services firm Ethoca , a subsidiary of Mastercard , and its partnerships with a growing matrix of banks. It estimates that each dispute costs $15-$70 for both cardissuers and merchants.

There’s a legitimate wave of disputes and chargebacks that are hitting the travel and entertainment verticals as consumers cancel trips, postpone weddings or try to get credit for flights that simply cannot be taken right now. The Issuer Side Of The Equation. She noted that consumers can opt to turn their cards on and off.

American Express chargeback reason codes are a collection of identifiers used to classify different chargeback situations, reflecting the disputes raised by cardholders against sellers. These codes are vital for organizing disputes and determining the necessary next steps.

It also ensures that data security best practices, particularly PCI DSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data. When this happens, a chargeback process will be initiated.

When you run any BIN number through a checking system, you end up with accurate information about the geolocation, cardissuer, and card type. Since online banking systems have become more popular and virtual cards have become a norm, BIN numbers aren’t necessarily bank-issued.

Merchants will also be able to avoid chargeback fees if customers file a dispute with their credit cardissuer, at least through the end of April. Merchants will also have twice as much time to respond to a customer dispute. Merchants will also have twice as much time to respond to a customer dispute.

Today’s latest is a report that a class action lawsuit might be happening across the pond against MasterCard this fall. billion antitrust settlement that included the marquee names in cards, Visa and MasterCard, and millions of retailers was thrown out on the grounds that a number of retailers were improperly represented.

Cardholders dispute a transaction with their bank, resulting in a reversal of funds. This occurs when customers intentionally dispute legitimate transactions just to get a refund of their payment for products or services they did receive. Last year, the payment business suffered an estimated 238 million chargebacks.

TL;DR Surcharges are additional fees that a business adds to a customer’s bill when they choose to pay with a credit card. These fees help the business offset the cost of credit card processing fees, which the merchant typically has to pay to the cardissuer and payment processor.

The former typically carry the same liability protections as those offered by a debit card, for example, while the latter do not offer consumers the same for unauthorized charges. Payroll cardissuers are also required to disclose their fee structures and customer dispute resolution process, but reloadable cardissuers are not.

Address Verification Service (AVS) A fraud prevention tool that checks the billing address provided by the cardholder against the address on file with the cardissuer. Annual Percentage Rate (APR) The annual interest rate charged by a credit cardissuer on outstanding balances.

Interchange fees are set by credit cardissuers, such as Bank of America, Citi, or Chase, and are adjusted every year in April and October. Assessment fees Assessment or network fees are directed to the credit card network- Mastercard, Visa, American Express, and Discover, to help settle costs associated with maintenance and operation.

Utilizing global payment networks (Visa, Mastercard, etc.) Compliance with Payment Card Industry (PCI) Standards The Payment Card Industry Data Security Standard (PCI DSS) ensures secure cardholder data processing, storage, and transmission. Mastercard Mastercard co-founded and co-developed the PCI DSS.

Today’s settlement agreement with merchants resolves claims against Visa, Mastercard and other defendants brought by the injunctive relief class in the lawsuit entitled In re Payment Card Interchange Fee and Merchant Discount Antitrust Litigation. MASTERCARD STATEMENT: PURCHASE, N.Y.–(BUSINESS

The exact rate can vary based on several factors, including the type of card used (debit or credit), the card brand (Visa, MasterCard, etc.), The purpose of an interchange fee is to compensate the cardissuer for the risk and operational costs associated with providing the credit or debit card service to the customer.

If a dispute was unfounded, they can start by responding through representment. This step allows merchants to submit proof to the cardissuer to demonstrate that the transaction was valid and should not have been reversed. Arbitration If representment does not resolve the issue, merchants can opt for arbitration.

This new feature applies to all instances of card reissuance, from replacing expired cards and EMV chip upgrades, to replacement in the case a card is lost, stolen or damaged. Customers will also be able to activate their card through the tracker. Citi customers in the U.S.

Breakdown of credit card processing fees Credit card processing fees are charged to merchants for each credit card transaction processed. Assessment fees Assessment fees are relatively small but consistent fees charged by credit card networks like Visa, MasterCard, American Express, and Discover.

The primary security standards that payment systems typically adhere to include: Payment Card Industry Data Security Standard (PCI DSS): PCI DSS sets forth requirements for securing payment card data, including encryption, access control, network monitoring, and regular security testing.

Each transaction incurs fees the cardissuer sets, varying based on the card type and associated risks. Debit cards typically carry lower fees due to lower payment risk, whereas credit cards involve higher fees to offset potential defaults. Limited customer support for disputes.

The company has two primary SaaS offerings: Kajo , a payment scheme compliance solution, and Amiko , which provides tools for fraud recovery and dispute management. “Globally, banks spend billions of dollars on scheme compliance and payment dispute management,” 6 Degrees Capital partner Thibault D’hondt noted.

Here are some other articles on chargeback management: How to Build a Chargeback Payments Team in your Company How to Win Chargeback Disputes What is a Good Credit Card Chargeback Rate for Merchants? Skills Required: Attention to detail, familiarity with card network rules, and proficiency in analyzing transaction data.

and $0.50), plus a percentage of each purchase (between 1% and 3%) on top of the interchange fees charged by the cardissuers. Tiered Pricing A tiered model puts credit card transactions into several categories—qualified, mid-qualified, and non-qualified. Interchange Plus Pricing A small fixed fee (between $0.10

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content