This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau (CFPB), the consumerprotection agency in the US, has hit Equifax with a $15million fine, after it found that the nationwide consumer reporting agency failed to conduct proper investigations of consumerdisputes.

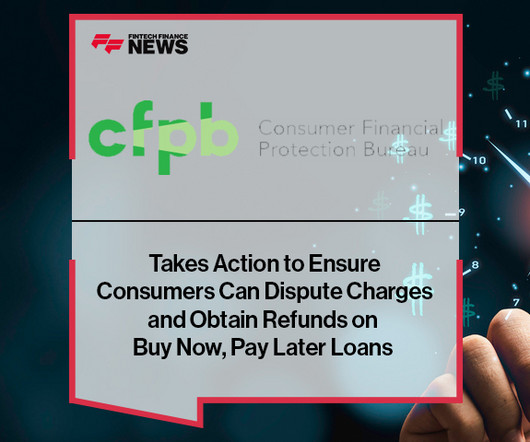

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule that confirms that Buy Now, Pay Later lenders are credit card providers. Accordingly, Buy Now, Pay Later lenders must provide consumers some key legal protections and rights that apply to conventional credit cards.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protectingconsumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections.

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations already on the books.”

Late last month, the Consumer Financial Protection Bureau (CFPB) issued an interpretive rule stating that Buy Now, Pay Later (BNPL) lenders are credit card providers. For those unfamiliar with the matter, summarize the CFPB’s recent ruling on BNPL. territories.

Moreover, given the fact that the CFPB uses these databases as part of its various enforcement actions, it has essentially created a version of Yelp, where enough bad reviews can net a multi-million dollar fine. A House bill introduced in June would require the CFPB to verify all claims made in complaints.

Compliance Risk Compliance with various consumerprotection-related laws and regulations [1] is critical for banks furnishing BNPL loans to ensure that obligations are understood and met on both sides of the transaction.

While there is some dispute whether baseball Hall of Famer Yogi Berra uttered these words, it is irrefutable that making predictions is tough business. The CFPB's New Open Banking Proposal Will Accelerate Exciting Product Innovations. However, some have questioned whether the same consumerprotection laws apply to all BNPL activity.

In 2020, the Consumer Financial Protection Bureau (CFPB) published two rules which implement the Fair Debt Collection Practices Act (FDCPA). While the revised legislation currently offers greater consumerprotections, it is also likely to result in new consumer abuses. Attorneys’ fees.

Its primary objectives encompass safeguarding consumers, maintaining financial stability, promoting market integrity, preventing fraud and security breaches, and ensuring legal compliance. It monitors and enforces regulations related to payment products and services to ensure fair treatment and transparency for consumers.

Separately, the ConsumerProtection Bureau (itself a creation of Dodd-Frank) is quite likely in the crosshairs of the incoming White House and the Republican Congress in early 2017. But the key debate and dispute as relates to the CFPB ties into the actual structure of the leadership at the helm of the bureau.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content