This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau (CFPB), the consumerprotection agency in the US, has hit Equifax with a $15million fine, after it found that the nationwide consumer reporting agency failed to conduct proper investigations of consumer disputes.

“Whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations,” CFPB Director Rohit Chopra said.

The Consumer Financial Protection Bureau is looking into how it can apply existing privacy and consumerprotectionslaws to emerging digital payments offered through Big Tech, as well as stablecoins and other cryptocurrencies.

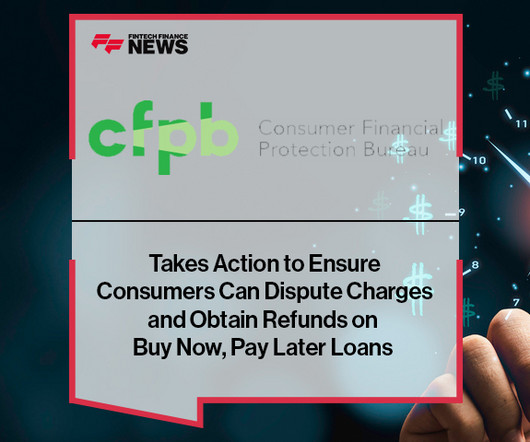

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule that confirms that Buy Now, Pay Later lenders are credit card providers. Accordingly, Buy Now, Pay Later lenders must provide consumers some key legal protections and rights that apply to conventional credit cards.

That’s according to a new report out from the Consumer Financial Protection Bureau’s (CFPB) Student Loan Ombudsman. The worse news is that the bureau is estimating a cost to consumers over the next two years of $125 million in unnecessary interest charges. 1, 2015, and May 31, 2016. Of that 8 million, about 1.2

The Consumer Financial Protection Bureau has once again made it clear that new AI- and machine learning-based technologies are held to the same consumerprotection regulations as established technologies.

The Consumer Financial Protection Bureau (CFPB) filed a lawsuit against Cincinnati-based Fifth Third Bancorp alleging that employees opened accounts for customers without their consent in an effort to reach sales targets, according to reports on Tuesday (March 10). The CFPB filed a complaint with the U.S.

ETA supports a uniform policy framework for AI that appropriately preserves the innovation and security AI brings, while ensuring appropriate consumerprotection. Modernize the CFPB The payments industry is committed to delivering innovative products and services in a transparent and secure manner.

The Bureau of Consumer Financial Protection (CFPB) has delayed the Aug. The CFPB is also correcting several errors in the rule. The Consumer Bankers Association (CBA) commended the delay. Compliance is being delayed 15 months, to Nov.

Things are getting tougher for the Consumer Financial Protection Bureau (CFPB) under the new political administration. More banks are now willing to challenge CFPB enforcement actions, said The Wall Street Journal. This already exceeds the total number of challenges the CFPB saw across 2016. The controversial U.S.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protectingconsumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections.

The Consumer Financial Protection Bureau (CFPB) announced on Monday (June 6) that it filed a lawsuit against Intercept Corporation and two of its executives, Bryan Smith and Craig Dresser, for the alleged illegal acts.

The Consumer Financial Protection Bureau said on Friday (March 18) that, at the agency’s request, a federal district court has entered a final judgment against Morgan Drexen, a debt relief company, with the resolution of a suit brought by the CFPB three years ago. Ledda was found by the court to have violated federal law.

The CFPB has its eye on the biggest marketplace lenders in the U.S., The new idea being floated involves classifying marketplace lenders, who operate online and also offer smaller loans with set payments, as installment lenders that are under the CFPB’s jurisdiction and regulations.

The CFPB has officially opened up its online forum for accepting consumer complaints geared at those who have experienced issues from online marketplace lenders. The bureau also released a bulletin about the marketplace lending industry and provided tips for consumers who are looking for alternative financing options.

That’s according to the Consumer Financial Protection Bureau , which announced on Monday (Aug. The CFPB’s order not only requires Wells Fargo to improve its consumer billing and student loan payment processing practices but also to provide $410,000 in relief to borrowers and pay a $3.6 million civil penalty to the CFPB.

s appeal of a $109 million penalty caused a legal battle over the constitutionality of the Consumer Financial Protection Bureau’s (CFPB) structure, agency officials are recommending that Director Mick Mulvaney dismiss the company’s case, American Banker reported. After PHH Corp. ’s In January, the U.S.

The Consumer Financial Protection Bureau (CFPB) is gearing up to sue Spain-based Santander Bank, claiming the bank has overcharged its car loan customers. Citing sources familiar with the CFPB’s plans, Reuters reported that the CFPB suit could happen as soon as Monday (Nov.

The US Consumer Financial Protection Bureau (CFPB) is proposing to subject large non-bank companies that offer consumer finance services including digital wallets and payment apps – such as Apple and Google – to the same regulatory scrutiny and oversight as banks, credit unions and other financial institutions.

This article will help you gain a better understanding of gaming and gambling laws in Down Under. USA: Stricter data-sharing laws, including the Gramm-Leach-Bliley Act (GLBA) and inter-agency reporting for suspicious activity over $3,000 USD. What are the Implications for Payment Companies (PSPs, PayFacs, etc)?

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations already on the books.”

Unlike Europe, there is no centralised regulatory framework governing open banking, though the Consumer Financial Protection Bureau (CFPB) has proposed a new rule that could establish a more standardised approach. As of 2023, account-to-account (A2A) transactions in the U.S. reached $1.1

Senator Elizabeth Warren also announced that she has begun an investigation into the hack, explaining in a letter to the Consumer Financial Protection Bureau (CFPB), the agency she helped create after the 2007-2009 financial crisis, that it may require additional powers to ensure closer federal oversight of credit reporting agencies. “Is

6), with the announcement that the Consumer Financial Protection Bureau (CFPB) will overhaul a series of 2017 payday loan regulations, set to go into effect in August 2019. The next chapter in the ongoing saga that is payday loan regulation officially began yesterday (Feb. The Tumultuous Response.

A small business (SMB) in Massachusetts borrowing funds via marketplace lender Kabbage has sued the platform, igniting new debate in the conversation over the definition of a “true lender,” according to reports in the National Law Review on Tuesday (Oct. Usury laws regulate how much interest can be charged on a loan.

Five federal financial regulatory agencies are encouraging banks, savings associations and credit unions to offer small loans to consumers and small businesses in response to the coronavirus pandemic.

Ever since the Dodd-Frank Act gave the Consumer Financial Protection Bureau (CFPB) jurisdiction over just about every US business that provides some form of consumer credit, Republicans have been complaining that the agency has too much power. Most bankers support moves to rein the CFPB in a bit.

As noted by the news outlet, the government will leverage existing antitrust law, and any fines or regulatory actions tied to the new mandates would be the purview of the Fair Trade Commission (FTC). CFPB Files Suit Against Citizens Bank. Digital Currencies, Too. million credit card customers. million credit card customers.

The CFPB's New Open Banking Proposal Will Accelerate Exciting Product Innovations. The Consumer Financial Protection Bureau (CFPB) has indicated it will publish rules , not guidelines, aimed at strengthening consumers’ control over and providing portability of their financial account data, sometime in 2023.

Compliance Risk Compliance with various consumerprotection-related laws and regulations [1] is critical for banks furnishing BNPL loans to ensure that obligations are understood and met on both sides of the transaction.

In 2020, the Consumer Financial Protection Bureau (CFPB) published two rules which implement the Fair Debt Collection Practices Act (FDCPA). This federal law, known as Regulation F goes into effect on November 30, 2021. In total, these laws were in the works for more than five years. Attorneys’ fees.

It’s been a dramatic 12 months for the CFPB. But that might not have been any big surprise given the title of the hearing: “ The CFPB’s Assault on Access to Credit and Trampling of State and Tribal Sovereignty.”. There were the hearings earlier this year in the House that devolved pretty quickly into dueling insults.

The CFPB will issue its final debt collection rule in the fall of 2020. Forty-two years after the enactment of the Fair Debt Collections Practices Act, the CFPB proposed the first set of rules governing third-party debt collection activities. The FCC will issue updated interpretations of the Telephone ConsumerProtection Act in 2020.

CFPB Debt Collection Rulemaking Will Likely Move Forward. The panel discussed the CFPB’s continued focus on developing new debt collection regulations. However, the law does not apply to pre-rule and proposed rulemaking activities. While our experts spoke on a number of hot-button topics, three main themes emerged.

According to American Banker , the Senate is expected to vote this week on legislation that would use the Congressional Review Act to repeal the CFPB’s regulation on discriminatory pricing by auto lenders. The rules were created to protect drivers who use indirect auto loans financed through a dealership, which are backed by banks.

The Kansas businessman – facing a 2017 conviction for violating federal truth in lending and racketeering laws in connection with his online lending business – attempted to apologize for the $3.5 According to Reuters, it served to convince the judge that Tucker had not really accepted that his actions were against the law.

California lawmakers are considering legislation that would extend disclosure requirements currently required by consumer lenders to lenders of small business loan products, according to Manatt, Phelps & Phillips, LLP. The amendment includes commercial and investment banks in those requirements. ”

Learning experiences have included $185 million in fines and penalties from regulators (including the CFPB) and a few rounds of public excoriation for its executives on Capitol Hill. Since that revelation, Wells Fargo has enjoyed a six-month lesson in why fraudulently using customer information doesn’t pay.

Consumer Financial Protection Bureau (CFPB): Established in response to the 2008 financial crisis, the CFPB is tasked with protectingconsumers in the financial marketplace. It monitors and enforces regulations related to payment products and services to ensure fair treatment and transparency for consumers.

the EU’s AI Act is set to become law early next year. the Consumer Financial Protection Bureau (CFPB) has been studying the BNPL industry since at least late 2021. At this point, much of the CFPB’s impact on BNPL has been minimal. Unlike policy in the U.S., The only question was when. In the U.S.,

According to a report in the Financial Times , more than a dozen attorneys general in states around the country in December expressed alarm about the appointment of Mick Mulvaney as the acting director of the CFPB, pointing out he once called the government watchdog a “joke…in a sick, sad kind of way.”

The implementation of Section 1033 of the Dodd-Frank Act , the 2010 post financial crisis legislation ushered-in to bring greater consumerprotections in financial services, is set to jump start the U.S. When 1033 becomes law and we have a precise timeline we are going to have a plan around it and make U.S. Mostly because U.S.

It seems an era has drawn to a close at the Consumer Finance Protection Bureau (CFPB) as that under Mick Mulvaney, interim director and Office of Management and Budget (OMB) head, gets underway in earnest. And, under his leadership, the new CFPB seems bent on doing things very differently than it has in the past.

However, a new era of Open Banking innovation is emerging, driven by a shift to an API-based system supported by stronger consumer regulations and standardisation, which will enhance competition and boost adoption. did not need to increase privacy laws and 71 per cent say consumers are not aware of consent management for data sharing.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content