This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau (CFPB), the consumer protection agency in the US, has hit Equifax with a $15million fine, after it found that the nationwide consumer reporting agency failed to conduct proper investigations of consumer disputes. Equifax processes approximately 765,000 disputes each month.

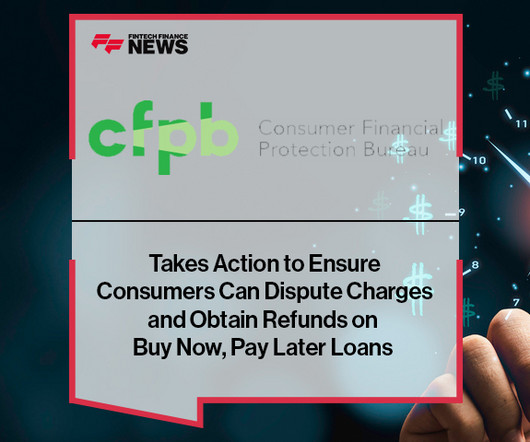

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule that confirms that Buy Now, Pay Later lenders are credit card providers. These include a right to dispute charges and demand a refund from the lender after returning a product purchased with a Buy Now, Pay Later loan.

Google has filed a legal challenge against the US Consumer Financial Protection Bureau (CFPB), the agency responsible for overseeing consumer finance, after it placed Google Payment Corp., The tech giant argues that the move, which the CFPB says is aimed at addressing potential consumer risks, constitutes regulatory overreach.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protecting consumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections. ” What’s next?

To say that 2020 has already started off as a busy year for the Consumer Financial Protection Bureau (CFPB) might be an understatement. In the most recent news late last week, the CFPB said it would change the way it defines and addresses “ abusive ” practices within the financial services arena. In the case, captioned Seila Law LLC v.

Later this morning the CFPB will begin taking comments on proposed rules that would ban financial firms from placing mandatory arbitration clauses within consumer contracts. The CFPB’s proposal is designed to protect consumers’ rights to pursue justice and relief, and deter companies from violating the law. .

Not steep enough to deter all bad actors, it seems – as the CFPB has recently spent time using some unusual tactics to expose redlining where it still exists. The CFPB interprets that as meaning they can’t seek personal information from government officials by the use of employees working undercover.

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumer protections under longstanding laws and regulations already on the books.”

consumer accounts were accessed by the hackers, as well as certain dispute documents with personal identifying information for approximately 182,000 U.S. Plus, there is the CFPB, which is widely believed to be about to lay a punishment down on Equifax using the same powers it has used against Wall Street’s biggest banks.

Credit scores and credit reports are increasingly relied upon by creditors, employers, insurers and even law enforcement. Per the memorandum offered by the Committee: “Our nation’s credit reporting system has an impact on almost every American. We need to start thinking about how we reimagine [the system], and rebuild it,” she stated.

While there is some dispute whether baseball Hall of Famer Yogi Berra uttered these words, it is irrefutable that making predictions is tough business. The CFPB's New Open Banking Proposal Will Accelerate Exciting Product Innovations. However, some have questioned whether the same consumer protection laws apply to all BNPL activity.

Compliance Risk Compliance with various consumer protection-related laws and regulations [1] is critical for banks furnishing BNPL loans to ensure that obligations are understood and met on both sides of the transaction.

Almost everyone – state law makers, federal law makers, consumer groups, industry groups and even short-term lenders themselves – agree that the industry should be regulated. Under the law, consumers will not be allowed to take out more than one loan at once. Kyle Koehler (R), a bill sponsor, said prior to passage.

The CFPB is moving toward a rule change that will make it much easier for consumers — or more specifically groups of consumers — to take banks and other financial institutions to court as part of class action lawsuits. It wasn’t surprising that the Field Hearing had a pro-CFPB rule feeling,” King told us shortly after. It’s official.

In 2020, the Consumer Financial Protection Bureau (CFPB) published two rules which implement the Fair Debt Collection Practices Act (FDCPA). This federal law, known as Regulation F goes into effect on November 30, 2021. As previously said, the CFPB announced final regulations amending Regulation F to implement the FDCPA in 2020.

The two firms, after consideration, decided that this was a case where they could not fight the law and win — and have thus withdrawn the deal. Trial Lawyers: Not the sizzle we want, but they get a boondoggle from arbitration rule “strike down” from the CFPB. Oh, and higher fees. Lawyers are happy, though. million consumers.

It was even more surprising to me that the CEOs didn’t have the data right in front of them, given the signals coming from regulatory bodies like the Consumer Financial Protection Bureau (CFPB) about the need for more oversight for real-time P2P payments networks. That idea of authorization is where deep divisions start to appear.

One week ago, the CFPB’s arbitration rule seemed more or less doomed to the scrap heap of financial regulatory history. The Comptroller of the Currency formally requested that the CFPB halt implementation of the rule while the OCC reviewed its effect on the banking industry. According to L.A.

Through transparent disclosures, dispute resolution mechanisms, and limits on consumer liability, regulations shield consumers from deceptive practices and ensure their financial well-being. It oversees compliance with federal banking laws, including those governing payments.

However, according to the CFPB , it has been providing inaccurate or false information on consumer reports, threatening their access to credit, employment and housing. Credit reporting errors can have serious consequences for a familys finances, and it is critical that credit reporting giants follow the law.

25), which was his last day as the head of the CFPB. Within a few hours, President Trump appointed Mick Mulvaney – the director of the White House Office of Management and Budget (OMB) – as the acting CFPB director. Democrats point to a law under Dodd-Frank that states the deputy director is to take over in the interim at the CFPB.

In the latest salvo in the legal wrangling between the Trump administration and the Consumer Financial Protection Bureau (CFPB), the Justice Department has signaled that it will embrace the argument laid out by PHH Corp. that the CFPB is unconstitutional. As noted by CFPBMonitor.com and disclosed in a court filing with the U.S.

So while the Dodd-Frank law may not be repealed in its entirety, capital requirements and stress testing may get a thorough look in the first few months of a Trump presidency. But the key debate and dispute as relates to the CFPB ties into the actual structure of the leadership at the helm of the bureau.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content