This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The number of Americans without bank accounts is expected to spike again in the wake of the coronavirus pandemic after hitting a low last year, according to a new report by the Federal Deposit Insurance Corp (FDIC). households without checking accounts fell to 5.4 The unbanked rate jumped to 8.6 percent in 2011, up from 7.6

With increasingly few exceptions, the ranks of the unbanked seem to be on the decline, according to new data released by the FDIC. According to FDIC data, unbanked American consumers peaked toward the end of the Great Recession in 2011 at 8.2 The percentage of Americans going without banking services fell to 7 percent in 2015 from 7.7

Robinhood , the FinTech that garnered a lot of attention last week after announcing a checking and savings product with 3 percent interest, has retreated from that, removing any mention of checking and savings from the product. Had they called us, I would have told them what I just told you in that I have serious concerns about this.

If ever there was a time to kill the check, that time would be now. The remaining tens of millions, those who do not have direct deposit payment information on file with the IRS … will have to wait for the proverbial (paper) check in the mail. FDIC) has estimated that 8.4 They steal checks. percent of the population.

Financial institutions offering checkless checking is trending, and checkless checking accounts—as part of the FDIC’s 2011 Model Safe Accounts Pilot—appeared to perform well among the underserved consumer participants.

The bank is one of a few smaller lenders that has teamed up with FinTechs who need services only an FDIC-regulated institution can provide. Other FinTech startups, like Robinhood and Square , are looking into becoming banks so they can improve their profits and offer customers bank-like products, including checking accounts.

Stock trading app Robinhood , which offers no-fee trading, is re-launching a checking feature called Cash Management after it was previously shelved due to regulatory issues. Investors’ money will be covered by the Federal Deposit Insurance Corporation (FDIC) up to $1.25 As reported on Tuesday (Oct. Robinhood is valued at around $7.6

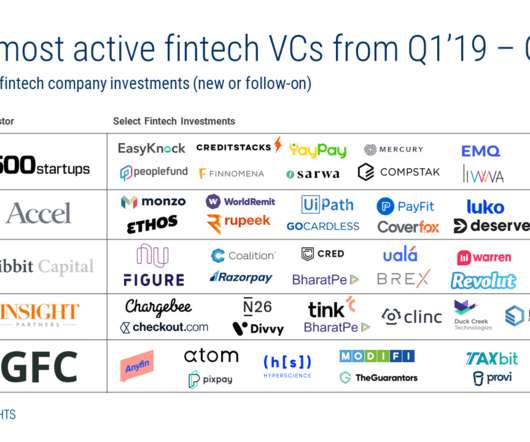

Some investors continued to cut checks in Q1, b ut which investors have remained active through the boom and bust over the past year? Mercury , which provides startups with FDIC-insured bank accounts. For all of the underlying data and insights, check out our State Of Fintech Q1’20 Report: Investment & Sector Trends To Watch.

customers to activate their FDIC-insured BlockCard bank accounts. The BlockCard accounts are crypto-friendly and function like regular checking accounts. Our customers will be able to link their existing financial institution to their crypto-friendly BlockCard bank account to easily move U.S. dollars between all of their accounts.”.

In today’s top news in digital-first banking, California FinTech Green Dot is rolling out the GO2bank mobile banking to help cash-strapped individuals, while stimulus checks are reportedly posing challenges for some users of H&R Block and TurboTax. Stimulus Checks Pose Issues For H&R Block, TurboTax .

28) at the Money20/20 conference, BlueVine Business Banking connects small businesses to checking account services and a debit card: the BlueVine Business Debit Mastercard. Banking services are provided via a collaboration with The Bancorp Bank, Member FDIC. Announced on Monday (Oct.

In today’s top news in digital-first banking, FIS is working with Quontic Bank on the Bitcoin Rewards Checking Account, while Aeldra has chosen i2c Inc. FIS, the bank software and payment technology firm, unveiled a collaboration with Quontic Bank on the Bitcoin Rewards Checking Account. to power its digital private banking offerings.

Discussion with senior regulators including the Commissioner of the SEC and the Former Chair of the FDIC. Check out the full agenda here. The post The Future Of Fintech 2019: Check Out The Full Agenda appeared first on CB Insights Research. GET THE 81-PAGE FINTECH TRENDS REPORT. GET THE 81-PAGE FINTECH TRENDS REPORT.

According to the Federal Reserve, about 19% of Americans are considered to be ‘unbanked’ or underbanked (defined as those who have a bank account but also use alternative financial services such as payday loans, money orders, or check cashing). Member FDIC. DailyPay is a financial technology company, not a bank.

Consumers in financial straits may find it difficult to maintain the balances necessary for them to keep their checking accounts open for one example, causing them to become unbanked. percent in 2019, its lowest rate in a decade since the FDIC first began tracking this statistic in 2009.

In an announcement, the bank said it would work with Google to debut a co-branded, FDIC-insured, digital-only bank account next year. In this way, Google gets new users for its Pay offering , and the banks get new customers and strengthen their respective brands. “It’s ” Looking Ahead.

High-yield checking and savings are now being offered by online wealth advisor Betterment as a way to attract new customers. . Like other FinTechs, Betterment will partner with FDIC-insured institutions since it doesn’t have a bank charter. Checking accounts will be insured up to $250,000 and savings accounts up to $1 million.

Check for: Penalties for access: penalties or fees for accessing funds could negate the benefit of higher interest earnings. Mobile banking services: A robust mobile app with comprehensive features like mobile check deposit, real-time alerts, and transaction capabilities allow for smooth management of finances on the go.

This older demographic also accounted for 20% of those who deposited mobile checks for the first time. . In the US, 16% of adults are underbanked — meaning that they have bank accounts but use alternative financial services like payday loans or check-cashing services — while 6% were unbanked, per the Federal Reserve. . Source: FDIC.

The company also offers an FDIC-insured checking account to help spur crypto-friendly banking, Johnson noted. Through that checking account, users can purchase crypto to be held in custody. “Or The company's crypto debit card, BlockCard , has seen 500 percent growth in usage rates, measured year over year.

To move toward retirement, and to have the money in place to get there, millennials need to make the leap from bare bones banking — checking and savings — into investing. In terms of mechanics, according to the company, Finch invests users’ checking balances into a tailored portfolio mix that matches account holders’ risk profiles.

and comes with other benefits like off-cycle payments, patented checks and optional prepaid debit cards, allowing workers full access to their pay through those solutions. residents in the near future, PYMNTS writes, according to a report by the Federal Deposit Insurance Corp (FDIC). In 2011, the number of unbanked Americans rose to 8.6

The Robinhood cash management feature is offered in partnership with a bank, and includes debit cards, and, critically, deposits backed by the Federal Deposit Insurance Corporation (FDIC). Earlier last year, Robinhood debuted a checking and savings product that did not have a bank partnership and ultimately was not successful.

resident and non-resident international clients of Aeldra can open an FDIC-insured U.S. The stars of financial services in 2021 will have something to do with credit,” Wain said, noting that the days of basic checking or demand draft accounts (DDA) are over. Aeldra, whose partners include Blue Ridge Bank, N.A,

However, it is combined with an FDIC-backed checking account called Zero Checking. The Zerocard and Zero Checking are combined together into one central app, so cardholders can see at a glance how much net funds they can access. The Zerocard, as it is called, is a World Mastercard that earns credit card cash back.

The teenager with a Fortnite habit who manages to clean out Dad’s checking account via the debit card linked to the gaming account. The company offers FDIC-insured bank accounts and a Visa -branded payment cards for teens (aged 13-18) with budgeting features and other financial education tools built in.

The accounts come with debit cards, digital payments and free check cashing, but do not allow overdrafts.”. She added that the annual $60 cost for the new accounts compares with charges of $200 to $500 per year at check cashing and money order service providers. a month and no minimum balance,” according to Reuters. In 2017, 6.5

A new report from the Federal Deposit Insurance Corporation (FDIC) shows that mobile banking can empower underserved customers to have greater control over their finances and ultimately open up access to mainstream banking.

FDIC), U.S. households that have zero persons with a checking or savings account, otherwise known as the unbanked, declined to a record low of 7 percent in 2015. The FDIC also said that the percentage of U.S. don’t have a checking or savings account. The FDIC also said that the percentage of U.S.

Having a simple bank checking account costs an average a monthly maintenance fee of $13.58 In the sense that it is a bank, MoneyLion takes deposits and makes sure those deposits are FDIC insured through a backend partnership with a traditional bank, Choubey said. or $163 a year. ATM fees, on the other hand, average around $4.66.

This new service follows last year’s unsuccessful launch of a checking and savings account product, which was not well received. The cash management feature is offered in partnership with a bank, and has debit cards, as well as deposits backed by the Federal Deposit Insurance Corporation (FDIC).

Casca With Casca , FDIC-insured banks and non-bank lenders fund small business loans in under seven days with 90% workflow automation, reduced costs, and thousands of hours in operational efforts reclaimed. Commercial banks, community banks, credit unions, B2B fintechs, etc.

Which means it really doesn’t come as all that huge a surprise that as of June 6th, SoFi had applied for a new (de novo) bank charter according to the FDIC. Instead, SoFi as a bank will exist so it can “provide its customers an FDIC insured NOW account and a credit card product. SoFi has confirmed the news.

The Zibo tools are meant to help save time and implement new tools like Federal Deposit Insurance Corporation (FDIC)-insured business checking accounts, automated rent collection, online bill pay and expense management to help streamline tax preparation.

that will enable businesses to send and receive FDIC-insured payments in near-real-time. “We’ve brought open banking and instant payments together in an omni-rail solution that enables companies to check off all of their payments needs from a single gateway,” said Zūm Rails Co-founder and CEO Marc Milewski. FedNow, the U.S.

Small businesses can sign up for an FDIC-insured bank account in three minutes, and can customize the platform to add sub-accounts for payroll, large purchases and taxes. “Many of these entrepreneurs are looking for self-service options with features that help them with their finances, rather than get in the way. .”

The bank is limiting eligibility to customers who have had a BoA checking account for a year. FDIC), National Credit Union Administration and Office of the Comptroller of the Currency — urged bankers to begin offering such small-dollar loans to help consumers deal with temporary cash flow problems.

N26 partners with Axos Bank to offer a Visa debit card and FDIC-insured checking account. Since the initial product launch in 2015, N26 has reached more than 3.5 million customers in 25 markets in Europe. N26 started rolling out in the U.S.

FDIC) estimated that 6.5 percent of households remain unbanked, with no checking or savings accounts in place. In this case, prepaid cards can serve as a payments alternative to traditional banking offerings like checks, and more technology-driven ones like real-time bank deposits.”. Another 18.7

Emerging payment solutions — mobile wallets and P2P payment networks most notably — are slowly but steadily displacing legacy payment options like cash and checks and cementing themselves in the day-to-day lives of consumers (particularly Millennials and Gen Zers). Emerging Payment Solutions Will Grow Up. small-dollar lending market.

The app can also be used to upload checks, like many mobile banking apps. Netspend touts the ease of signup and use: There’s no credit check requirement, no late fees and no interest payments, although cardholders will be charged an annual fee of $85, deducted after the first time they load the card.

Of course, those more than beat the national average on checking accounts, which is currently at a 0.08 In addition, Wealthfront works with FDIC-insured partner banks — including East West Bank , New York Community Bank and others — to hold customers’ deposits. In addition, Ally Bank and Barclays have high-yield offerings that earn 2.2

Chime noted in its press release that it began March with more than three million FDIC bank accounts. Chime launched in 2013, offering debit cards, savings accounts and checking accounts to consumers without any fees. The company also plans to double its size to more than 200 employees and expand its leadership team.

One particularly useful example is checking and savings account data. Studies conducted by the FDIC show that there are tens of millions of U.S. As with any data source, the use of checking and savings account data will provoke questions with respect to potential data bias. Positive Data Brings Predictive Value.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content