This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In anticipation of Black Friday and Cyber Monday, European Visa Fintech Partner, Rivero is urging banks, neobanks, and financial institutions to prepare for a potential spike in cardholder disputes. An analysis of the company’s internal data has highlighted a 25% rise in reported disputes over the past year.

The Consumer Financial Protection Bureau (CFPB), the consumerprotection agency in the US, has hit Equifax with a $15million fine, after it found that the nationwide consumer reporting agency failed to conduct proper investigations of consumerdisputes.

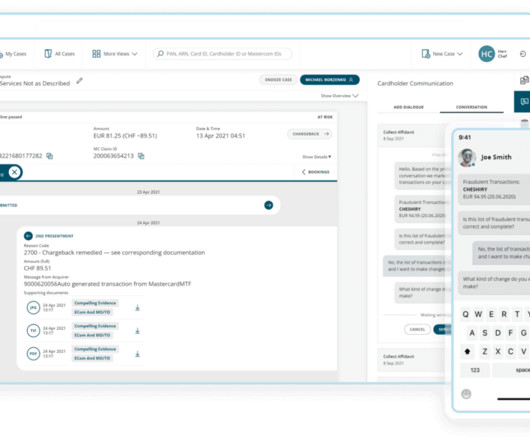

Fortunately, modern SaaS-based solutions enable financial institutions to automate and scale existing dispute management systems in record time and with minimal investment. One example of best-of-breed fintech solutions is Amiko, the virtual agent of Rivero’s dispute management solution.

Visa today announced that it is applying the company’s infrastructure, technology and capabilities to account-to-account (A2A) payments, giving consumers more control and protection on how they pay via bank transfers. In 2023, £3.7tn was paid via A2A Faster Payments in the UK, a 15% increase over the previous year[1].

Accordingly, Buy Now, Pay Later lenders must provide consumers some key legal protections and rights that apply to conventional credit cards. These include a right to dispute charges and demand a refund from the lender after returning a product purchased with a Buy Now, Pay Later loan. In 2021, people disputed or returned $1.8

Debit or credit card chargebacks are when a disputed charge made to a merchant’s account is refunded to the customer’s bank account. fraudulent charges) The main purpose of chargebacks is to protectconsumers from shady vendors or fraudulent activity. What Are Credit Card Chargebacks?

It is advised that firms ensure their custody arrangements, contracts and terms of service are aligned with these legal definitions in the interest of avoiding disputes while strengthening consumer trust. This could lead to disputes over ownership, custody, and liability in cases where the legal framework is yet to be fully tested.

The Payments Association , the trade group representing the payments sector, has launched its Payments Manifesto for 2025, urging the UK government to modernise the payment infrastructure to ensure consumerprotection.

Chargeback disputes represent a growing challenge for merchants and financial institutions. Originating as a consumerprotection mechanism, chargebacks were designed to ensure customers could dispute fraudulent or erroneous transactions. We dig into the facts and statistics on chargebacks.

A well-crafted refund and cancellation policy is essential for any business, as it provides clear guidelines that protect the company and its customers. These policies help set expectations, reduce disputes, and ensure efficient transactions by outlining the terms under which refunds and cancellations are allowed.

Winning chargeback disputes is important for merchants because chargebacks take time to deal with and lead to financial losses and increased processing fees. Here’s a guide to help merchants navigate and win chargeback disputes in credit card processing. Credit cards have a strong value proposition of consumerprotection.

A chargeback is a reversal of a credit card transaction initiated by the cardholder’s bank, usually as a result of a dispute by the customer over the purchase. It acts as a consumerprotection tool, allowing customers to reclaim funds for unauthorized transactions, fraud, or dissatisfaction with goods or services.

BNPL providers will need to assess whether their products are suitable and affordable for consumers. When consumers do get into trouble, they might not have access to effective dispute resolution and hardship processes. The new laws aim to balance consumerprotection with innovation and competition.

Curve , the ultimate digital wallet, has become the first to offer section 75 protection on purchases made through its Wallet. This is a step change in consumerprotection, allowing users to make payments without worrying about losing money if a product is faulty or if theres a problem with the purchase.

Separately, it is noted that the recent rulings in the EU and US requiring Apple to unlock the iPhone’s near field communication (NFC) capabilities have enabled Curve Wallet customers to make payments on their iPhone using Curve or their Curve card, which includes enhanced features from Curve, such as access to credit and purchase protection.

Push notifications, he noted, cannot be phished, unlike SMS OTPs, further enhancing consumerprotection. The chargeback mechanism under card scheme rules also offers recourse for cardholders to dispute charges and recover funds, particularly in cases where merchants fail to enable 3DS authentication.

This decision mandates that BNPL users will now have the right to dispute charges and obtain refunds for returned products, aligning BNPL services with the consumer safeguards traditionally associated with credit cards. In 2021, people disputed or returned $1.8billion in transactions at five firms surveyed.

Furthermore, the manifesto includes policies to encourage the use of interoperable dispute management systems to tackle first party fraud and reduce errors and the adoption of robust digital verification frameworks to create a safer financial ecosystem.

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations already on the books.”

The aim of this initiative is to establish a “trusted, world-leading payments ecosystem” by promoting innovation, competition and consumerprotection within the payments sector, that can help the UK regain global leadership in payments and unleash growth.

acquirers, they are now rejecting opt-out cross sales or negative options on payment pages due to regulatory concerns, primarily driven by consumerprotection legislation, pressure from the card brands to lower dispute rates, and the threat of legal action. .” In talking with our U.S.

Yaacov Martin : The Consumer Financial Protection Bureau (CFPB) recently released an interpretive rule for the BNPL industry, which classifies BNPL providers as credit card issuers under the Truth in Lending Act. What will this mean for both fintechs and banks operating in the BNPL space going forward? territories.

Add in the current climate of heightened geopolitical uncertainty, trade disputes, foreign exchange volatility and regulatory complexities, and corporate treasurers have their work cut out for them, often with reduced budgets and slim staffing. There are a number of things that intersect here: data, privacy, consumerprotection.

Compliance Risk Compliance with various consumerprotection-related laws and regulations [1] is critical for banks furnishing BNPL loans to ensure that obligations are understood and met on both sides of the transaction.

Digital payments giant Visa is set to debut ‘Visa A2A’ in the UK early next year, offering consumers an enhanced digital user experience, advanced security features, and an easy-to-use dispute resolution service that represents a significant upgrade to the existing pay-by-bank experience.

.” Reports pointed to the merchant cash advance industry in particular, an unregulated area of small business finance that often requires SMB borrowers to agree to confessions of judgment, which means those borrowers agree to lose any court dispute that may arise in the future as a condition of obtaining financing.

However, for open banking to take off for retail and P2P payments, the report says that consumerprotections need to be improved with a minimum form of dispute resolution. Without sustainable financials, it is hard to see that open banking can thrive over the long term.”

In all, around $85 million in consumer funds are missing due to discrepancies in Synapse’s records. Adding to the confusion, the dispute is ongoing in court, and because Synapse is a fintech and is thus unregulated, regulatory bodies are unable to protectconsumers, many of whom are still missing their funds.

While there is some dispute whether baseball Hall of Famer Yogi Berra uttered these words, it is irrefutable that making predictions is tough business. However, some have questioned whether the same consumerprotection laws apply to all BNPL activity. Tue, 07/02/2019 - 02:45. by Daniel Nestel. VP, Government Relations.

The companies vowed to protect small business borrowers, disclose pricing and resolve any disputes fairly. Prospa signed the code alongside Spotcap, Capify, GetCapital, OnDeck and Moula, reports said.

For higher transaction amounts, they typically require a PIN or biometric verification, offering enhanced consumerprotection. How do I handle disputes over payments? Handle payment disputes professionally by listening to the customer’s concerns and investigating the issue thoroughly.

Such practices can lead to legal and regulatory challenges, particularly if consumers are harmed or misled. Compliance with ConsumerProtection Laws: Affiliate marketers must adhere to various consumerprotection laws and regulations, such as the Federal Trade Commission (FTC) guidelines in the United States.

“Growth has been so dramatic that some of the regulatory framework surrounding the technology still lags behind – most notably in terms of consumerprotection. Integration into digital wallets will boost adoption, as will improvements to the dispute resolution process. “This will take years, not months.

In 2020, the Consumer Financial Protection Bureau (CFPB) published two rules which implement the Fair Debt Collection Practices Act (FDCPA). While the revised legislation currently offers greater consumerprotections, it is also likely to result in new consumer abuses.

CFPB Director Richard Cordray defended the database as “part of our DNA,” playing an important role in guiding the agency’s supervision of companies, enforcement actions, rulemaking and consumerprotection. The CFPB handled around 271,600 in 2015, up 8 percent from 2014. The CFPB says companies respond to 97 percent of the complaints.

While the intricacies of how exactly Cambridge Analytica gathered the data are still somewhat contested, no one is disputing that it got access to customer data that it wasn’t supposed to have. Customers that may have been impacted were offered consumerprotection services. Fitness Hacks.

The Commission educates consumers and businesses on their rights and obligations under the FCRA by creating materials such as the Start with Security and Stick with Security initiatives, and the Protecting Personal Information: A Guide for Business.

John Penrose MP, Member of Parliament for Weston-super-Mare; author of Power to the People 2021 , an independent report on ways to improve consumerprotection and promote competition. Marion King, OBL Chair and Trustee. Daniel Gordon, Senior Director of Markets, Competition and Markets Authority (CMA).

These rules will maintain core consumerprotections and transparency, replacing standards that had been updated in 2012. Visa and Mastercard must negotiate swipe fees in good faith with merchant buying groups, and the agreement provides a streamlined process for resolving disputes.

Chargeback Process (when customers dispute transactions) In some cases, cardholders may dispute a transaction, leading to a chargeback. Credit card transactions tend to have better consumerprotection features, such as extended warranties and purchase protection, compared to debit card transactions.

Inform them about the surcharge policy, highlighting the consumerprotection guidelines. Merchants may also face disputes from customers and chargebacks. Communicate surcharges to customers Know your customer’s preferred channels (e.g., email, social media, SMS), and tailor concise messages to those channels.

The main objectives of the DSA are to: Ensure high-level protection for users’ fundamental rights online, such as freedom of expression, privacy, data protection, non-discrimination, and consumerprotection.

If either party encountered a legal dispute on either website, there was no one to stand up and appeal for them, and they may lose their sales revenue entirely. Merchants collectively lost hundreds of millions on inventory in early 2016, for example, when Amazon decided to recall and refund hoverboards.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content