This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Banks By 2020, Bhutan’s financial sector included five banks, three insurance companies, one CSI bank, five microfinance institutions, one pension institution, two telecom companies as well as a single stock exchange. These advancements offer the potential to boost economic development and prosperity across the Kingdom.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. In addition, we explored the power of tapping into alternative data in credit scoring in markets across the globe.

In an effort to bridge what is increasingly being known as the “inclusion gap” for minorities, Visa is finding promise in supporting products for financialinclusion in the credit union and community bank portfolio. To hurdle the financial gap that exists for these underserved populations in North America.

How Agentic AI Can Transform Fintech Operations Potential Use Case Without Agentic AI With Agentic AI Customer engagement Rule-based chatbots provide scripted responses and struggle with context retention AI-driven financial assistants adapt to user behaviour, proactively offer personalised insights, and autonomously act (e.g.,

Our work with both EFL and Lenddo is part of the FICO FinancialInclusion Initiative. Lenders rely on credit scoring to assess consumers’ risk, and credit scoring relies on credit data. But what if an applicant is new to credit? EFL’s models generally rely on 10-12 specific traits.

The scoring methodology was developed by EFL Global and marketed by FICO as part of our FICO FinancialInclusion Initiative , designed to open up credit markets around the world to a larger number of unbanked and underserved consumers. Expanding credit worldwide. EFL has been part of providing more than $1.3

This comment from a participant in our recent EMEA Risk Leadership Forum caused a lot of chuckles and nodding heads. When it comes to evaluating creditrisk, everyone wants to know if, when and how lenders will start probing their Facebook account. Processing it can be time-consuming, but the data itself is generally clean.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. This type of financialinclusion is good for the consumer and good for our business.

FinancialInclusion Using Analytics. As a data scientist working on credit models in the late 80s, it was a mission to help replace human bias with data-driven science. in 1989, it meant lenders of all sizes could leverage the technology of scoring and open up credit to consumers that they might not have lent to in the past.

Lighthub Asset and WeLab’s venture (the consortium) will improve financialinclusion in Thailand. Its features will be tailored to solopreneurs and micro, small and medium enterprises (MSMEs) facing unstable income and limited financial access. It has disbursed more than $15billion of digital loans to date.

When it comes to using alternative data in creditrisk assessments, the field has really opened up over the last few years. Alternative data is a hot topic, in part because of the data explosion of the last few years, and in part because of the drive in lending for financialinclusion. Multiple Types of Alternative Data.

The system got a major boost in the 1970s with the passage of The Fair Credit Reporting Act , which officially regulated what information would be collected as well as created rules that made credit reports something consumers had a legal right to both see and dispute. But is FICO keeping pace with modern financial services?

It serves as a broad-based, independent standard measure of creditrisk. It is relied upon by stakeholders across the entire lending ecosystem – from regulators, investors and boards to consumers, lenders, and brokers – as a baseline metric for assessing creditrisk that is fair to both lenders and consumers. .

Finding a way to score millions without credit history. Círculo de Crédito , the fastest-growing credit bureau in Mexico, has used unique creditrisk scores from FICO to boost financialinclusion in Mexico and help an additional 20 million citizens access credit.

CreditRisk and FICO Score Trends? Consumers face debt burden challenges that could impact U.S. creditrisk and FICO® Score trends. economy, credit scores, and creditrisk trends were headed. At the start of the pandemic, uncertainty surrounded where the U.S. consumers?

Just a few months ago at PYMNTS’ Innovation Project 2016 , PayPal CEO Dan Schulman told Karen Webster that “financialinclusion is really about financial health.”. Acquiring that financial health means financial institutions are able to not only know, but accurately identify, their customers.

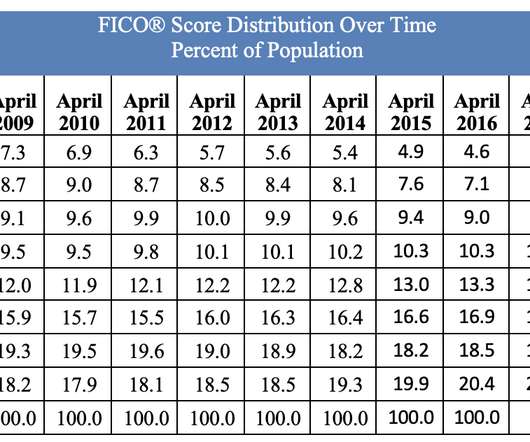

FICO® Score Stays Steady at 716, as Missed Payments and Consumer Debt Rises. Each year, we provide insight into the national average FICO ® Score to help ensure consumers have a baseline measure of credit health standing. consumer reporting agencies (CRAs). Average U.S. by Ethan Dornhelm. expand_less Back To Top.

This comprehensive approach is what we refer to as financialinclusion.” ” Data is the key Christian Widhalm, CEO, Bloom Credit Data has emerged as one of the most important assets an organisation can have. After all, as the saying goes: knowledge is power.

As a leader in analytics and credit scoring, FICO will be there to showcase thought leadership and new innovations in credit scoring, fraud, originations, and more. Pacific: New Frontiers in CreditRisk Scoring for a Consumer-Centric Era. Pacific: Wake up with the CEO.

While most financiers would run from an environment like that, CEO Toms Niparts of Jeff , an app-based lending platform based in Latvia, saw it as a huge opportunity. “We As Niparts explains it, the more consumers use Jeff, the more data they can gather to build a better credit score and in turn support additional future lending.

As time passes, consumers are seeing the number of embedded finance offerings increase across the wide range of products and services they use. This tailored approach allows for a more inclusive and fair assessment of credit products, moving away from a one-size-fits-all approach.

As of April 2023, there were 1,000 active fintechs in Latin America (LatAm) with a vast majority focusing on financialinclusion, tackling the issue of 70 per cent of the population not having access to formal financial services. Our goal is to build an open and interconnected financial market.

Does FICO’s minimum scoring criteria limit consumers’ access to credit? . Over the last 30 years, FICO has continued to analyze the minimum amount of credit bureau data that is necessary to deliver a reliable, predictive FICO® Score to the market - which benefits both consumers and lenders alike.

These algorithms analyse extensive data sets to accurately evaluate creditworthiness, making financial services more accessible and responsive to consumer needs. “For consumers, payment and lending experiences become frictionless due to AI, with the technology able to process loan applications and payments more efficiently.

But I am so proud to be a part of the team that made the FICO® Score the trusted industry standard for helping lenders open the door to credit access and mainstream financial services for consumers in the U.S. It wasn’t unusual to hear from the head of creditrisk of a bank that the bank “didn’t book bad loans.”

consumer data not present in the traditional credit bureau files) to enhance the predictiveness and inclusiveness in credit scoring. This is especially critical for the approximately 50 million consumers in the U.S. More than 200 million U.S.

Q: Dale, to start with, can you provide a little background on your business motivation as a creditrisk executive for exploring the value of consumer-permissioned DDA data? Q: What insights have you gained (risk or otherwise) about consumers who are willing to permission access to their DDA data? Any surprises?

I recently had the opportunity to participate in a virtual event hosted by the Urban Institute entitled FinancialInclusion: Lessons Learned and What’s Next for Innovations in Alternative Credit Data. The use of this type of alternative data for credit scoring and, ultimately, consumer lending is promising for several reasons.

Endava, a technology services company, has teamed up with Finexos , an AI-powered creditrisk and analytics platform, in order to enhance credit decision-making for banks and lenders. This alliance aligns with Endava’s commitment to financialinclusion and innovation in the banking sector.

In total, Prosper extended more than USD $225M in credit access to these consumers. Prosper also proactively mitigates creditrisk and meets the increasing credit demand for creditworthy customers based on their monthly updated FICO® Scores. Millions of consumers in the U.S.

Here were the top 5 posts of 2017 in the Risk & Compliance category: US Average FICO Score Hits 700: A Milestone for Consumers. By contrast, growth in student loan debts outpaced inflation, being both greater in number as well as balances; this undoubtedly creates a drag on capacity for other forms of consumercredit.”.

Saudi Credit Bureau Delivers Access To Loans For Millions with Score. SIMAH wins FICO ® Decisions Award for financialinclusion using FICO ® Scores. This growth in Saudi financialinclusion was made possible by SIMAH’s advocacy efforts with financial institutions and a parallel education campaign with consumers. “We

China Construction Bank (CCB) hopes to reach more millennial consumers and is using alternative scoring services to improve decision making and improve financialinclusion efforts to reach this demographic. For its achievements, CCB won a 2018 FICO® Decisions Award for FinancialInclusion. by FICO.

Using remote sensing technologies on farmland, the bank assesses creditrisk based on crop growth and various factors. This approach ensures that even farmers in remote areas can access credit. Paytm Bank is India’s largest digital ecosystem for merchants and consumers.

Consumer awareness of their credit and FICO® Scores has never been higher. Whether planning to buy a car, home or head to college, millions of consumers know and manage their credit score. Now financialinclusion innovation is on the horizon that will change the dynamic of the lender and customer relationship.

How data sharing can improve creditrisk decisioning. The launch of the Open Finance Framework by Bangko Sentral ng Pilipinas (BSP) in 2021 was a big step forward in driving financialinclusion for millions of Filipinos across the market who still do not have access to credit. FICO Admin. Wed, 10/03/2018 - 23:42.

Credit bureau, business information, and creditrisk specialist CRIF has inked a strategic partnership with open banking API company Ozone API. The collaboration is designed to hep financial institutions enhance data-driven decision-making, streamline operations, and share data safely.

FICO has long-supported financial service institutions in fulfilling their obligations to comply with applicable adverse action notice requirements under regulations such as the Equal Credit Opportunity Act (ECOA). The use of Machine Learning must be balanced with deep domain expertise in creditrisk modeling. Can Arkali.

These products and services are safe, highly secure, and promote financialinclusion by allowing consumers including lowandmoderate income consumers who have historically not had full access to the financial system to conduct their everyday financial transactions. states and territories.

We were seeking a tool with predictive analytic qualities that would accelerate and increase approvals, while qualifying consumers better, even the unbanked ones. It could take anywhere between 3 to 12 months whenever creditrisk wanted to make a change,” said Valera. FICO had the strongest offering that filled the brief.”.

Our winners have innovated in lending, supply chain optimization, customer management, debt collection, fraud and financialinclusion. Procter & Gamble (P&G), has optimized its consumer product transitions, saving it millions of dollars and allowing it to reduce time spent on initiative planning. Fraud & Security.

Today, businesses in more than 100 countries use FICO’s technology and solutions to defend customers against fraud, advance financialinclusion, boost supply chain resiliency, and more. The company’s FICO Score has become the standard measure of consumercreditrisk in the U.S.,

The sudden nature of the lockdowns had an immediate impact on incomes for consumers and the businesses that supported them. Given the significant changes in credit and consumer behaviour, there has been a quest by lenders for new data and early warning indicators. Opening this market is a priority for lenders.

Paul Deall, head of risk, mortgages at Westpac (previous winner). An accomplished leader with 18 years’ experience in creditrisk, banking and analytics in the Australian market, Paul has a track record of using technology and data to develop and implement strategic change to drive tangible business outcomes. by Nikhil Behl.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content