This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Lenders rely on credit scoring to assess consumers’ risk, and credit scoring relies on credit data. But what if an applicant is new to credit? Original module design inspired by Sternberg et al. The post Credit Scoring: Which Personality Traits Predict CreditRisk?

This comment from a participant in our recent EMEA Risk Leadership Forum caused a lot of chuckles and nodding heads. When it comes to evaluating creditrisk, everyone wants to know if, when and how lenders will start probing their Facebook account. Processing it can be time-consuming, but the data itself is generally clean.

We are thrilled and honored to be recognized by Aite Group as best in class and the overall rankings leader for our Loan Origination Solution. For nearly 50 years, FICO has pioneered intelligent creditorigination powered by world-class analytics. FICO Origination — A Loan Origination Solution You'll Never Outgrow.

When it comes to using alternative data in creditrisk assessments, the field has really opened up over the last few years. Here is useful information on how to assess alternative data and combine it with so-called traditional data to improve creditrisk models. It is also possible for a consumer to manipulate this data.

Credit scoring is widely used in South Africa to determine the risk of credit applicants — using this kind of objective, precise measure of risk lets banks, retailers and other organizations lend with more confidence, which in turn means more people get approved for credit. About the Empirica Score.

However, to get down to his concerns, the analyst said — per news reports such as CNBC — that the recently debuted “Square Installments” (which, as the name implies, offers payment plans) may expose the company in a way that makes it vulnerable to credit markets. Trade wars loom, and the consumer seems to be caught in the middle.

lakh crore as of March 2024, underscored the increasing demand for credit among Indian consumers. To make informed decisions, it’s essential to grasp the intricacies of the loan origination process. What is Loan Origination System (LOS)? The consumption loans portfolio, which expanded by 15.2% year-over-year to 90.3

Banks By 2020, Bhutan’s financial sector included five banks, three insurance companies, one CSI bank, five microfinance institutions, one pension institution, two telecom companies as well as a single stock exchange.

By actively working with lenders and consumers to navigate the current situation, it is apparent that precise analytics are as important as ever to help avoid over-tightening of credit which can delay an economic recovery. . For instance, higher-resilience consumers tend to have: More experience managing credit.

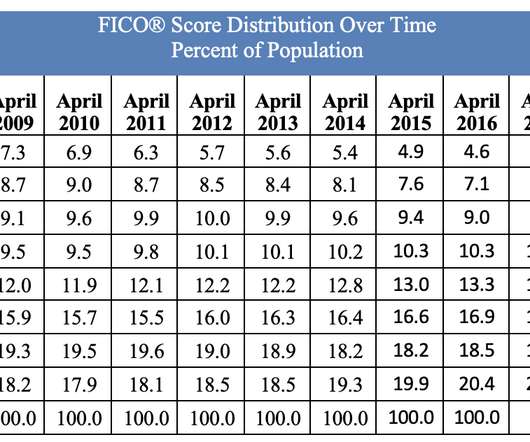

FICO® Score Stays Steady at 716, as Missed Payments and Consumer Debt Rises. Each year, we provide insight into the national average FICO ® Score to help ensure consumers have a baseline measure of credit health standing. consumer reporting agencies (CRAs). Average U.S. by Ethan Dornhelm. expand_less Back To Top.

As a leader in analytics and credit scoring, FICO will be there to showcase thought leadership and new innovations in credit scoring, fraud, originations, and more. Pacific: New Frontiers in CreditRisk Scoring for a Consumer-Centric Era.

Origination Scores Offer Targeted Insight. Origination scores add significant value above and beyond the FICO ® Score, which is based solely on the data found in a consumer’scredit bureau file. Machine Learning Enhances Origination Decisions. customers assessed only by their FICO ® Score).

After a 2018 that had its highs and lows, what might 2019 have in store from a creditrisk management standpoint? Here are three key developments in credit scoring that we will be keeping an eye on in the new year: Consumer-Contributed Data Takes Center Stage. Risk in Bankcard Originations on the Rise.

14) that the company is entering the small business finance space with a new platform that adds to its existing consumer lending, creditrisk and portfolio risk management offerings for financial institutions. Financial information firm Sageworks has announced its expansion into the world of SME lending. ”

A recent Bloomberg article asserted that “consumercredit scores have been artificially inflated over the past decade,” as credit scores have steadily increased over the past decade of economic expansion. FICO Scores Are Not Fixed Estimates of CreditRisk. So are FICO ® Scores “artificially inflated”?

FICO Fact: Can having no credit score be better for consumers than a low credit score? A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. Axios recently spoke on the demand to issue out more credit scores.

The key driver of this trend is the improved consumer financial health that has resulted from the steady economic growth that the U.S. consumers’ scores upwards as well. There has been increased consumer awareness around FICO Scores and credit education. Negative credit information is being removed from credit files.

In this new age where face-to-face interaction is severely limited and the view into consumercreditrisk can be cloudy, financial institutions need accurate analytic insights across the customer lifecycle in order to predict future behavior more than ever. Origination: Better gauge risk exposure and reduce your “bad rate.”.

Metrics: Ormsby Street is founded as a pin-off from BCSG, which owned a simple creditrisk product originally dating back to 2008. Product distribution strategy: Direct to Consumer (B2C), Direct to Business (B2B), through financial institutions. Product Launch: January 2015. HQ: London, UK. Founded: February 2014.

FCA’s Consumer Duty Mandates Sharper Use of Technology. Managing UK customers to better outcomes under the FCA’s Consumer Duty will require a true platform for understanding and action. Every UK bank, lender and financial services firm is likely to have the FCA’s Consumer Duty front-of-mind right now. Structure of Consumer Duty.

A more predictive credit score means more predictable cash flows which are, in turn, more attractive to investors for all types of securitized assets (e.g., mortgages, auto loans, credit cards, etc.) offering continuity and stability for lenders, investors, and consumers.

Here were the top 5 posts of 2017 in the Risk & Compliance category: US Average FICO Score Hits 700: A Milestone for Consumers. By contrast, growth in student loan debts outpaced inflation, being both greater in number as well as balances; this undoubtedly creates a drag on capacity for other forms of consumercredit.”.

As time passes, consumers are seeing the number of embedded finance offerings increase across the wide range of products and services they use. This trend is transforming traditional business models by integrating financial services into non-financial platforms, thereby offering a seamless experience to consumers.

FICO will present key insights gained from recent FICO® Resilience Index research and early lender adoption use cases across the consumercredit lifecycle at several key industry events starting later this month. The latest FICO® Resilience Index 2 will be available to lenders across all three credit bureaus by the end of summer 2021.

Managing fraud is a balancing act that starts with knowing your fraud risk appetite. Fraud managers have to look beyond losses and loss prevention and consider consumers’ need for a frictionless experience, regulators’ stipulations and the competitive pressures of fintech disruptors.

Creditrisk industry veterans who managed consumer loan portfolios through the Great Recession can recall the challenge of responding to swiftly changing borrower payment behavior and the resulting delinquency and default rate volatility during that time. risk that only manifests during periods of economic stress).

Different than traditional credit bureau data, trended data provides a historical view of information such as monthly account balances for the previous 24+ months, giving lenders more insight into how individuals are managing their credit. We have used FICO® Scores for many years.

Creditrisk industry veterans who managed consumer loan portfolios through the Great Recession can recall the challenge of responding to swiftly changing borrower payment behavior and the resulting delinquency and default rate volatility during that time. risk that only manifests during periods of economic stress).

We were seeking a tool with predictive analytic qualities that would accelerate and increase approvals, while qualifying consumers better, even the unbanked ones. It could take anywhere between 3 to 12 months whenever creditrisk wanted to make a change,” said Valera. The risk team rescheduled and froze repayments for USD$2.4

This four-part series looks at embedding portfolio risk resilience into decisions across the credit lifecycle through targeted application of the FICO ® Resilience Index. risk that only manifests during periods of economic stress) more precisely. Enhanced portfolio creditrisk management loss forecasting accuracy.

Lendbuzz’s financing model, which is powered by machine learning and proprietary algorithms, allows it to better assess the creditworthiness of consumers with limited U.S. credit history to help them secure financing for auto loans. As a result, car dealerships have the opportunity to attract additional business opportunities.

Consumers across the globe continue to look to buy the most up-to-date model and stay ahead of advances in device technology. CreditRisk Assessment Still Weighs on Telco Providers It’s a tricky balancing act for Telco providers to managing their creditrisk and assessment strategies.

Many lenders in markets outside the US use FICO® Scores to assess the risk of consumers applying for loan, but don’t continue to monitor those consumers’ risk using the FICO Score. The FICO® Score has been available in the Russian market through the National Bureau of Credit Histories (NBKI) since 2008.

The panel of experts assembled all agreed that an important part of upward economic mobility is access to credit, whether it’s to buy a car, own a home or start a business. That’s why FICO has been focused on finding new ways to demonstrate responsible financial behavior so that lenders can confidently extend credit to more consumers. .

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for creditrisk assessment. That’s because FICO® Scores are built to last. Ethan has a B.S.

consumers’ scores upward. FICO Score Research: Explainable AI for Credit Scoring. Credit Scoring Trends to Watch in 2019. In February, Ethan Dornhelm looked at 4 key developments in credit scoring that he thought would be talked about in 2019: Consumer contributed data. Risk in Bankcard Originations on the Rise.

Originally, it seemed that Apple Pay Later would act as a rival to other BNPL solutions. However, following the cancellation of the BNPL service, Apple has announced that it will partner with Affirm to offer consumers instalment loans at the point of purchase once iOS 18 is rolled out. One such potential rival was Affirm.

For FICO, customer development means working with customers through all the stages of the lifecycle – from marketing to originations to customer management. What kind of creditrisk does she pose? 2. “Financial companies will observe significant differences between consumer behaviours in pre, during and post COVID-periods.

China Construction Bank (CCB) hopes to reach more millennial consumers and is using alternative scoring services to improve decision making and improve financial inclusion efforts to reach this demographic. Partnering with the FICO team, we have significantly improved our origination efficiency while maintaining our risk profiles.

The company said Wednesday (April 5) that it is rolling out its Origination Manager Essentials solution for mid-market banks and credit unions. “Origination Manager Essentials delivers banks the same technical advantage so they can compete on experience and relationships rather than technology,” the company said.

How can lenders best measure and manage creditrisk, given the disruptive patterns in consumer behaviour over the last 18 months? Last week a FICO team met with chief risk officers from some of the biggest UK banks to discuss these and other challenges, at our UK CRO Summit.

Any rated organization shall be allowed access to their individual rating and the data that impacts a change in their rating. Rating companies shall not provide third parties with sensitive or confidential information on rated organizations that could lead directly to system compromise.

FICO® Scores, often an important contributor to underwriting risk management strategies, are designed to provide valuable risk rank-ordering through all economic cycles. Figure 1: Auto finance account origination default rates by FICO® Auto Score 8, Oct 13-Oct 15 and Oct 07-Oct 09 versus a theoretical 3% default rate cut-off.

FICO Resilience Index is designed to rank order consumers with respect to their resilience to severe economic stress. These benchmarking reports compare the distributions of new and existing accounts across different portfolios (and at the consumer-level). FICO® Resilience Index is calculated at a consumer-level.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content