This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Managing creditrisk used to be a reactive process. Waiting until account holders fall behind to take action not only meant that customers’ credit scores would take a hit before their banks were alerted to a problem, but also that banks would lose the revenue from the scheduled payment.

This comment from a participant in our recent EMEA Risk Leadership Forum caused a lot of chuckles and nodding heads. When it comes to evaluating creditrisk, everyone wants to know if, when and how lenders will start probing their Facebook account. Processing it can be time-consuming, but the data itself is generally clean.

The scoring methodology was developed by EFL Global and marketed by FICO as part of our FICO Financial Inclusion Initiative , designed to open up credit markets around the world to a larger number of unbanked and underserved consumers. Expanding credit worldwide. EFL was founded in 2006 when Drs.

Based on the 2020 US Census , the US credit-eligible population (those over 18 years of age) is 258 million people. But how many of those consumers can obtain a FICO® Score? . Calculations by FICO data scientists indicate that more than 232 million US consumers can be scored by the FICO® Score suite.

How will these trends affect managing creditrisk? Delinquency rates on consumer loans and credit cards, which are currently being suppressed with government and bank support, are expected to increase rapidly. According to global statistics, the ratio of state aid to GDP is 4.4 into “connected decisions”.

When it comes to using alternative data in creditrisk assessments, the field has really opened up over the last few years. Here is useful information on how to assess alternative data and combine it with so-called traditional data to improve creditrisk models. It is also possible for a consumer to manipulate this data.

Fintech Partner Connect will “support new ways for businesses and consumers to seamlessly and securely pay, get paid, send money and more,” a spokesperson for the credit card and financial services giant said in an email announcing the new program on Visa on Wednesday (Nov.

FICO® Score Stays Steady at 716, as Missed Payments and Consumer Debt Rises. Each year, we provide insight into the national average FICO ® Score to help ensure consumers have a baseline measure of credit health standing. consumer reporting agencies (CRAs). Average U.S. by Ethan Dornhelm. expand_less Back To Top.

Using a nationally representative sample of FICO scorable consumers as of October 2017, we compared homeownership rates (using presence of an open mortgage loan as a proxy) across Millennial consumers age 25 to 34. Key Findings: Consumers with closed student loans are more likely to begin their homeownership journey.

New FICO research shows that not this not the case. Looking at credit bureau data as of July 2016, medical collections reporting – both paid and unpaid collections greater than $99 – breaks down by age as follows: While the peak of this curve occurs at age 27, the rate of consumers with medical collections is uniformly high for ages 24 to 46.

These algorithms analyse extensive data sets to accurately evaluate creditworthiness, making financial services more accessible and responsive to consumer needs. “For consumers, payment and lending experiences become frictionless due to AI, with the technology able to process loan applications and payments more efficiently. .

The two executives said acquirers need to have better fraud management solutions than ever before, because the pandemic has prompted consumers to use credit cards for more online and app-based transactions. “We AI Also Helps Manage CreditRisk. Fighting Fraud in a Post-Pandemic World.

FICO's research team explored this topic in a new paper, “Developing Transparent CreditRisk Scorecards More Effectively: An Explainable Artificial Intelligence Approach”. This lack of transparency is particularly acute for consumer lending, where regulations require lenders to provide adverse action notices.

consumers think about artificial intelligence (AI) as it relates to their financial lives? This was a year that bent and broke quite a few risk forecasting models, thus all the more reason to bring AI smarts to bear on transaction volumes scaling far beyond a human pace. Per the Index , “PYMNTS’ research shows that 63.6

Does FICO’s minimum scoring criteria limit consumers’ access to credit? . Over the last 30 years, FICO has continued to analyze the minimum amount of credit bureau data that is necessary to deliver a reliable, predictive FICO® Score to the market - which benefits both consumers and lenders alike.

Equifax , the credit scoring company still reeling from a massive data breach last year, announced news on Monday (Feb. In a press release , the company said the dataset provides information for researchers and modelers, including “creditrisk scores, geography, debt balances and delinquency status at the loan level.”

In an interview conducted by Karen Webster with Rob Meloche, Senior Director of Global Financial Inclusion at Visa, the conversation focused on the payment company’s research, conducted in partnership with Filene Research Institute , that revealed the spending power that exists within the minority community in the U.S.

ID Analytics, a consumerrisk management company, announced Wednesday (Oct. 26) new research that revealed over six out of 10 millennials declined for credit are not seen applying again for at least 12 months. A frequently referenced Bankrate.com study reported that 63 percent of millennials do not have a credit card.

Many American consumers are feeling the financial squeeze as the holiday shopping season goes on and will be turning to flexible spending plans to help put them at ease. More merchants are embracing buy now, pay later (BNPL) options to allow consumers to pay in four installments interest-free. In fact, only 20.7 In fact, only 20.7

How are advances in artificial intelligence and machine learning changing creditrisk assessment? On Tuesday, April 17, 1:30-2:30, my colleague Ethan Dornhelm and I will show that machine learning offers tremendous efficiencies for research “in the lab”. Join me at this session on Thursday, April 19, 10:15-11:15.

FICO Fact: Can having no credit score be better for consumers than a low credit score? A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. Axios recently spoke on the demand to issue out more credit scores.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. In addition, we explored the power of tapping into alternative data in credit scoring in markets across the globe.

Below, we take a look at how tech companies are unbundling Bank of America’s front office, from consumer deposits and payments to equity research and business credit cards. . Consumer payments. This has provided an opportunity for other research providers to gain market share among banking clients. . Company Name.

After a 2018 that had its highs and lows, what might 2019 have in store from a creditrisk management standpoint? Here are three key developments in credit scoring that we will be keeping an eye on in the new year: Consumer-Contributed Data Takes Center Stage. Risk in Bankcard Originations on the Rise.

consumer data not present in the traditional credit bureau files) to enhance the predictiveness and inclusiveness in credit scoring. This is especially critical for the approximately 50 million consumers in the U.S. More than 200 million U.S.

Participants and Influencers throughout the mortgage ecosystem have been told by the three main US credit bureaus through their jointly owned and controlled credit scoring firm, VantageScore, that the VantageScore can enable millions more consumers to gain access to a mortgage. million of whom will qualify for mortgage credit.

The National Consumer Assistance Plan (NCAP) is a comprehensive series of initiatives intended to evaluate the accuracy of credit reports, the process of dealing with credit information, and consumer transparency. Medical collections that are identified in the credit file as being ‘paid by insurance’ are even less common.

As time passes, consumers are seeing the number of embedded finance offerings increase across the wide range of products and services they use. According to recent the latest Juniper Research report , the global embedded finance market currently boasts a total transaction value of around $92billion.

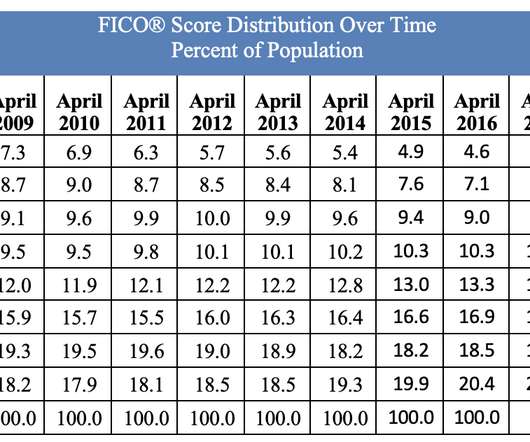

Key drivers of this trend are the steady economic growth experienced over this period, as well as improved financial behavior driven by consumer awareness of their FICO® Scores. There are consumers who weren’t using credit back in 2009 but who have since established a sufficient credit history to meet the FICO minimum scoring criteria.

Plati Potom develops post-payment solutions for eCommerce and offline retailers, as well as data analysis and creditrisk management tools. For QIWI, this transaction is another step in implementing its M&A strategy of investing in promising teams and technologies in the FinTech space.

According to the release, the company’s research and development as well as analytical functions will remain in its Ra’anana, Israel offices. Behalf said that B2B sellers can use its product to “receive payment upfront, without the need to assume creditrisk.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for creditrisk assessment. in management science/operations research from UC San Diego.

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumercreditrisk. Which raises the question: Should rental data be widely reported to the three primary consumercredit agencies (CRAs)? But how many?

The panel of experts assembled all agreed that an important part of upward economic mobility is access to credit, whether it’s to buy a car, own a home or start a business. That’s why FICO has been focused on finding new ways to demonstrate responsible financial behavior so that lenders can confidently extend credit to more consumers. .

consumers and the global economy. . And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

Research from Juniper Research has revealed that by 2028, the BNPL userbase will increase by 107 per cent to, from 380 million users in 2024. The state of BNPL in 2024 Juniper Research found that despite fintech companies commanding the BNPL market for years, 2023 saw a major shift, as superapps and banks gained traction.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. FICO ® Resilience Index tools that measure consumer resiliency, benefit lenders in a recessionary environment. Building resilience into credit portfolios. asokolowski@speednet.pl. Fri, 06/03/2022 - 12:24. by Moma Chakraborty.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. FICO ® Resilience Index tools that measure consumer resiliency, benefit lenders in a recessionary environment. Building resilience into credit portfolios. asokolowski@speednet.pl. Fri, 06/03/2022 - 12:24. by Moma Chakraborty.

You are about to pitch a new capability that will address the need for short-term liquidity for nearly half of US consumers. When it comes to addressing short-term liquidity, the market size is likely 40%-50% of all consumers. Possibly your investor panel would like to hear about solutions that align to small dollar credit.

consumers’ scores upward. FICO Score Research: Explainable AI for Credit Scoring. Credit Scoring Trends to Watch in 2019. In February, Ethan Dornhelm looked at 4 key developments in credit scoring that he thought would be talked about in 2019: Consumer contributed data. Read the full post.

FICO will present key insights gained from recent FICO® Resilience Index research and early lender adoption use cases across the consumercredit lifecycle at several key industry events starting later this month. To learn more, watch the recent Consumer Bankers Association webinar.

In my last blog post , I shared a new FICO research study on credit trends in auto lending. So how are consumers affording these larger loans? This shift may signal an increase in creditrisk for the industry because six-year loans have historically had higher delinquency rates.

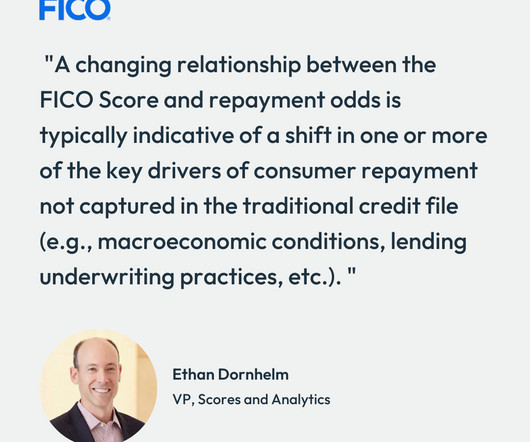

What the FICO Score is not designed to do is provide a specific, fixed estimate of creditrisk; we know from tracking the scores over three-plus decades that the relationship between the FICO Score and consumers’ likelihood of loan repayment can and does shift over time and across economic and financial cycles. and Canada.

Our first patent in this field was over 25 years ago regarding the use of neural nets to detect credit card transaction fraud. Machine learning is used throughout the company, not just in our industry-leading consumer fraud solutions, but in solutions ranging from cybersecurity risk detection to adaptive marketing profiles.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content