This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The investment will help AKUVO expand its cloud-native collections and creditrisk solutions, enhancing efficiency and customer experience for banks, credit unions, and fintechs. Digital collections and creditrisk platform AKUVO landed a new round of funding today. .

Managing creditrisk used to be a reactive process. Waiting until account holders fall behind to take action not only meant that customers’ credit scores would take a hit before their banks were alerted to a problem, but also that banks would lose the revenue from the scheduled payment.

Also, what’s a simple and legitimate matter of creditrisk ? Those questions also speak to the seemingly impossible tension in the world of payments and new card accounts: how to onboard and authenticate consumers as quickly and seamlessly as possible, while also protecting them and the institution from fraud. Bad Timing.

Lenders rely on credit scoring to assess consumers’ risk, and credit scoring relies on credit data. But what if an applicant is new to credit? Everybody has a personality which can help us understand their risk profile, making the EFL assessment universal – we can score anyone.

How will these trends affect managing creditrisk? Delinquency rates on consumer loans and credit cards, which are currently being suppressed with government and bank support, are expected to increase rapidly. According to global statistics, the ratio of state aid to GDP is 4.4 into “connected decisions”.

Depending on who is mouthing the phrase, one might hear it as “appetite for risk” or “risk appetite.” Risk is what someone takes on, ostensibly for some measure of gain, perhaps outsized gains at that. There is always the risk that these lenders will not get paid back. Risk Gets Riskier.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. This type of financial inclusion is good for the consumer and good for our business.

In fintech, Agentic AI could enhance fraud prevention, risk management, trading, and customer engagement by autonomously analysing financial data, detecting anomalies, and executing decisions in real time. Theres a risk that AI could inadvertently expose data through cyberattacks, algorithmic vulnerabilities, or insufficient safeguards.

Fraudsters, armed with advanced technologies and professional networks, are exploiting gaps in systems and consumer behaviour. Lin Tao ( Prezzee ) highlighted the disproportionate risk her industry faces: Gift cards are inherently attractive to scammers due to their high liquidity and minimal traceability.

One of the few clear implications from the initial two months of the lockdown with the changes to consumer behavior and the uncertainty ahead is the imperative for organizations to regain clarity on creditrisk by obtaining a more complete picture of consumer creditworthiness, says LexisNexis Risk Solutions' Ankush Tewari.

Credit scoring is widely used in South Africa to determine the risk of credit applicants — using this kind of objective, precise measure of risk lets banks, retailers and other organizations lend with more confidence, which in turn means more people get approved for credit. About the Empirica Score.

CreditRisk and FICO Score Trends? Consumers face debt burden challenges that could impact U.S. creditrisk and FICO® Score trends. economy, credit scores, and creditrisk trends were headed. At the start of the pandemic, uncertainty surrounded where the U.S. consumers?

In 2023, 27% of all point-of-sale (POS) payments were made using credit cards while 23% were made with debit cards. A survey by Forbes Advisor also revealed that 33% of consumers prefer to use credit cards as they’re safer than carrying cash. Credit card companies also use them to fund rewards programs.

Given the roller coaster ride consumer finances have been on for the last 10 months, managing risk has become critical for financial institutions (FIs), both in terms of rising fraud counts and in terms of rising consumer delinquencies. But AI, he said, can provide a lot more than that in terms of protecting FIs from risk.

AKUVO , a leading technology organization specializing in collections and creditrisk management, is proud to announce that Prosperity Bank , with $40 billion in total assets, has chosen AKUVO’s platform to streamline its collections processes. We are excited to see the long-term impact this will have on our collections process.”

The shift driven by fintechs could erode banks’ dominance, forcing them to modernise or risk losing a significant share of the market. While banks still hold the majority of merchant relationships and dominate acquiring market share in most regions, they face an existential risk. Why is it important? What’s next?

But it occurred to them that their solution was useful outside of HR — and that many of the things that made someone a good hire of over time could also make them a good creditrisk over time, if the artificial intelligence (AI) model they were using to screen with were modified to that task. Expanding Access to Credit With AI.

It serves as a broad-based, independent standard measure of creditrisk. It is relied upon by stakeholders across the entire lending ecosystem – from regulators, investors and boards to consumers, lenders, and brokers – as a baseline metric for assessing creditrisk that is fair to both lenders and consumers. .

Fraudsters, armed with advanced technologies and professional networks, are exploiting gaps in systems and consumer behaviour. Lin Tao ( Prezzee ) highlighted the disproportionate risk her industry faces: Gift cards are inherently attractive to scammers due to their high liquidity and minimal traceability.

Young consumers don't have long credit records, but they do make lots of recurring payments that can feed creditrisk decisioning, according to Barrett Burns, president and CEO of VantageScore Solutions.

Based on the 2020 US Census , the US credit-eligible population (those over 18 years of age) is 258 million people. But how many of those consumers can obtain a FICO® Score? . Calculations by FICO data scientists indicate that more than 232 million US consumers can be scored by the FICO® Score suite.

Fintech Partner Connect will “support new ways for businesses and consumers to seamlessly and securely pay, get paid, send money and more,” a spokesperson for the credit card and financial services giant said in an email announcing the new program on Visa on Wednesday (Nov.

Managing fraud is a balancing act that starts with knowing your fraud risk appetite. Fraud managers have to look beyond losses and loss prevention and consider consumers’ need for a frictionless experience, regulators’ stipulations and the competitive pressures of fintech disruptors. Step 3 – Collaboration with Risk.

Mastercard is harnessing artificial intelligence (AI) in a bid to hit fraudsters hard by searching for emerging patterns of criminal activity before they become major problems, two top executives told Karen Webster during Mastercard’s Virtual Cyber & Risk Summit. “In AI Also Helps Manage CreditRisk.

And in banking, financial institutions can incorporate artificial intelligence into their consumercredit strategies at a time when a retroactive approach to creditrisk management has become less feasible amid COVID-19. 48.8% : Portion of consumers who require a vaccine before returning to their routines.

By actively working with lenders and consumers to navigate the current situation, it is apparent that precise analytics are as important as ever to help avoid over-tightening of credit which can delay an economic recovery. . For instance, higher-resilience consumers tend to have: More experience managing credit.

The use of scores that rate a firm’s cybersecurity risk — such as the FICO® Enterprise Security Score — is picking up momentum. As more entities rely on these scores and ratings, their governing bodies and relevant regulatory agencies will care more about how these tools are used to drive decisions to mitigate risk.

Banks By 2020, Bhutan’s financial sector included five banks, three insurance companies, one CSI bank, five microfinance institutions, one pension institution, two telecom companies as well as a single stock exchange.

“By analysing big data and rapidly assessing risks, AI empowers financial companies to make well-informed decisions. Natasa Kyprianidou, senior director at Alvarez & Marsal “Traditional credit decision timelines, extending over weeks or months, have been dramatically shortened to seconds thanks to AI-driven algorithms.

Curve , the ultimate digital wallet, has announced the appointments of Robert Pasco as General Manager of Curve Credit and Ash Woolf as Senior CreditRisk Manager. With the UK’s unsecured consumercredit market valued at 232 billion, there is a great opportunity for responsible, innovative and ethical solutions.

The proposed credit card interest rate cap legislation , courtesy of Democratic presidential hopeful Senator Bernie Sanders and Rep. Alexandria Ocasio-Cortez is in serious need of an almost half-century-old refresher course in the unintended consequences of price caps on the American consumer. consumers by as much as 40 percent.

How can lenders best measure and manage creditrisk, given the disruptive patterns in consumer behaviour over the last 18 months? Last week a FICO team met with chief risk officers from some of the biggest UK banks to discuss these and other challenges, at our UK CRO Summit. Managing Risk Models in a Crisis.

Addressing Portfolio Risk in Economic Uncertainty: Part 1 (2022). This four-part series looks at embedding portfolio risk resilience into decisions across the credit lifecycle through targeted application of the FICO ® Resilience Index. risk that only manifests during periods of economic stress) more precisely.

Retail consumers, small and medium enterprises, and commercial entities are looking to banks for increasing levels of support and assistance, especially as government-introduced stimulus programs start to mature and expire around the globe. Here are our five recommendations for creditrisk managers.

Leveraging FICO’s heritage of scoring expertise, the new models outperform prior FICO industry version scores in key use cases while providing the same trusted user and consumer experience as prior versions. The FICO® Auto Score 10 provides strong performance for prime thin and new-to-credit files many of who maybe first-time auto borrowers.

Plus, FICO Score 10 T utilizes a consistent odds-to-score relationship as the prior FICO Score version used by the Enterprises, offering continuity and stability for lenders, investors and consumers. FICO® Score 10 T incorporates trended credit bureau data. FICO Score 10 Suite Available from All Three Credit Bureaus.

Creditrisk industry veterans who managed consumer loan portfolios through the Great Recession can recall the challenge of responding to swiftly changing borrower payment behavior and the resulting delinquency and default rate volatility during that time. risk that only manifests during periods of economic stress).

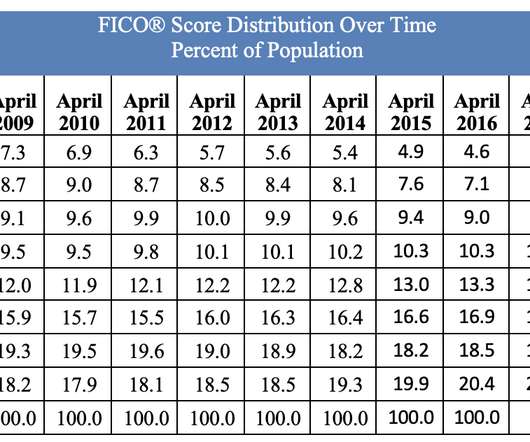

FICO® Score Stays Steady at 716, as Missed Payments and Consumer Debt Rises. Each year, we provide insight into the national average FICO ® Score to help ensure consumers have a baseline measure of credit health standing. consumer reporting agencies (CRAs). Average U.S. by Ethan Dornhelm. expand_less Back To Top.

For my predictions, I’ll focus on four areas of tactical concern within consumer banking that I feel confident bank executives will make significant progress addressing 2019. The post Consumer Banking Predictions 2019: Four Trends to Watch appeared first on FICO. Banks Will Get Smarter in the War for Deposits. The good times are over.

Creditrisk industry veterans who managed consumer loan portfolios through the Great Recession can recall the challenge of responding to swiftly changing borrower payment behavior and the resulting delinquency and default rate volatility during that time. risk that only manifests during periods of economic stress).

And if that consumer is looking to secure any type of credit, the party on the other end of the transaction will use the FICO Score to critically inform an important decision: should my organization assume business risk by transacting with this person? A score that quantifies cyber risk.

Addressing Portfolio Risk in Economic Uncertainty: Part 3 (2022). Building portfolio risk resilience into customer management. Lenders must adopt a similar mindset as they manage the financial health of their consumer lending portfolios to insulate their existing assets from potential portfolio risk volatility.

As well as the increasing application of AI in financial services for risk management and personalized experiences. Financial services are increasingly using AI to manage risks, combat money laundering, and offer personalized customer experiences. Lastly, consumers must see its value and start using the technology.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content