This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, to get down to his concerns, the analyst said — per news reports such as CNBC — that the recently debuted “Square Installments” (which, as the name implies, offers payment plans) may expose the company in a way that makes it vulnerable to credit markets. Trade wars loom, and the consumer seems to be caught in the middle.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. This type of financial inclusion is good for the consumer and good for our business.

ƒFord Motor Credit Co. 25) that it will implement machine learning credit approval models to determine if it will lend a consumer money as it goes after a segment of the market that doesn’t have a solid credit history. They are typically a good creditrisk and are expected to command $1.4

CreditRisk and FICO Score Trends? Consumers face debt burden challenges that could impact U.S. creditrisk and FICO® Score trends. economy, credit scores, and creditrisk trends were headed. At the start of the pandemic, uncertainty surrounded where the U.S. consumers?

For my predictions, I’ll focus on four areas of tactical concern within consumer banking that I feel confident bank executives will make significant progress addressing 2019. I’ll leave the speculation on the headline-grabbing technologies — your blockchains and your dancing robots — to others. Banks Will Get Smarter in the War for Deposits.

FICO® Score Stays Steady at 716, as Missed Payments and Consumer Debt Rises. Each year, we provide insight into the national average FICO ® Score to help ensure consumers have a baseline measure of credit health standing. consumer reporting agencies (CRAs). Average U.S. by Ethan Dornhelm. expand_less Back To Top.

It's not only consumer transactions that are feeling the pains of an industry reliant on cash, either. Because consumer transactions continue to rely on cash, the accounts receivable (AR) and accounts payable (AP) processes within the supply chain can be fragmented.

A recent Bloomberg article asserted that “consumercredit scores have been artificially inflated over the past decade,” as credit scores have steadily increased over the past decade of economic expansion. FICO Scores Are Not Fixed Estimates of CreditRisk. So are FICO ® Scores “artificially inflated”?

FICO Fact: Can having no credit score be better for consumers than a low credit score? A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. Axios recently spoke on the demand to issue out more credit scores.

Businesses certainly purchase differently than consumers do. The credit management platform automates aspects of customer credit management, from credit approval, to online ordering, to invoicing and collections. “We We call it ‘CMaaS’ for Credit Management-as-a-Service.”. And on the horizon now?

The FICO® Score has been a stable and highly effective tool for rank ordering creditrisk through prior fluctuations in economic conditions, and we expect the FICO® Score to continue to provide strong risk rank ordering through the current COVID-19 pandemic.

MoneyLion has teamed up with Nova Credit to integrate cash flow underwriting into its decisioning engine, enabling credit issuers on its platform to access more comprehensive data for evaluating consumers’ financial health.

But building financial services capabilities in-house is costly, time-consuming, and creates significant regulatory and financial risk. For Brex Embedded partners, their customers can make fast, secure global payments in virtually any currency, all while automating their existing financial workflows and payment reconciliation.

These algorithms analyse extensive data sets to accurately evaluate creditworthiness, making financial services more accessible and responsive to consumer needs. “For consumers, payment and lending experiences become frictionless due to AI, with the technology able to process loan applications and payments more efficiently.

But it occurred to them that their solution was useful outside of HR — and that many of the things that made someone a good hire of over time could also make them a good creditrisk over time, if the artificial intelligence (AI) model they were using to screen with were modified to that task. Expanding Access to Credit With AI.

After a 2018 that had its highs and lows, what might 2019 have in store from a creditrisk management standpoint? Here are three key developments in credit scoring that we will be keeping an eye on in the new year: Consumer-Contributed Data Takes Center Stage. Risk in Bankcard Originations on the Rise.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. In addition, we explored the power of tapping into alternative data in credit scoring in markets across the globe.

The system got a major boost in the 1970s with the passage of The Fair Credit Reporting Act , which officially regulated what information would be collected as well as created rules that made credit reports something consumers had a legal right to both see and dispute. But is FICO keeping pace with modern financial services?

There is also evidence in the US that BNPL users tend to have a riskier credit profile than those of traditional consumercredit products. Once the platform approves the credit line, it pays the merchant the full amount of the goods purchased, thus taking on the customer’s creditrisk.

This seems fitting since the underwriting and compliance processes can be a bit of a challenge. This holiday season, I wanted to give the gift of knowledge by sharing the top common compliance questions and how the right answers could keep you off the underwriter naughty list. And in a lot of situations, that answer is “no.” “Can

The debt funding was led by BHI, ConnectOne Bank, IDB Bank, Viola Credit and a large insurance company. Lendbuzz’s financing model, which is powered by machine learning and proprietary algorithms, allows it to better assess the creditworthiness of consumers with limited U.S.

The deal will help Empower expand into the credit card market. Empower also announced it closed the acquisition of Philippines-based consumercredit and lending fintech Cashalo. Empower , a fintech helping to extend credit to underserved consumers, announced plans to acquire underserved credit card provider Petal.

I had the pleasure of speaking on a panel at ABS East yesterday, entitled “Traditional vs Non-Traditional Underwriting, Does Machine Learning Teach Us Anything New?”. The panel primarily focused on the opportunities and challenges associated with the use of Machine Learning (ML) in creditunderwriting.

Although they both had similar ideas about the use of technology to improve credit decisioning at the consumer’s point of need, they pitched to different consumers and used very different channels to acquire customers. LendingPoint’s focus: near-prime customers who apply for credit online. Breaking New Ground. .

If we think of a lending portfolio as a night club, its underwriting policy acts as the doorperson, checking IDs and making sure anyone trying to enter meets documented criteria. FICO® Scores, often an important contributor to underwriting strategies, are designed to provide valuable risk rank-ordering through all economic cycles.

Having announced a partnership with Dun & Bradstreet , Velotrade is expanding the pool of data from which it draws to underwrite financing. The first and most obvious risk is creditrisk, or the risk that a business will fail to repay financing.

A more predictive credit score means more predictable cash flows which are, in turn, more attractive to investors for all types of securitized assets (e.g., mortgages, auto loans, credit cards, etc.) offering continuity and stability for lenders, investors, and consumers.

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumercreditrisk. Which raises the question: Should rental data be widely reported to the three primary consumercredit agencies (CRAs)? But how many?

a leading payments technology company, has achieved significant results by creating a centralized underwriting management solution on the FICO® Decision Management Platform (DMP). Additionally, we have transitioned certain processes downstream with no negative outcome on KYC validation and no increased risk to the organization.”.

As recent events have shown (China began a nationwide crackdown on P2P lending last year, following a series of multi-billion dollar scams in the space), consumer finance is challenging in the massive country. Technology serves as an advantage for X Financial, even beyond its underwriting engine.

In my last blog post , I shared a new FICO research study on credit trends in auto lending. So how are consumers affording these larger loans? This shift may signal an increase in creditrisk for the industry because six-year loans have historically had higher delinquency rates.

If we think of a lending portfolio as an exclusive night club, its underwriting policy acts as the doorperson, checking IDs and making sure anyone trying to enter meets minimum acceptance criteria. Traditional underwritingrisk management strategy approach in stressed versus unstressed economy. Senior Director, Scores.

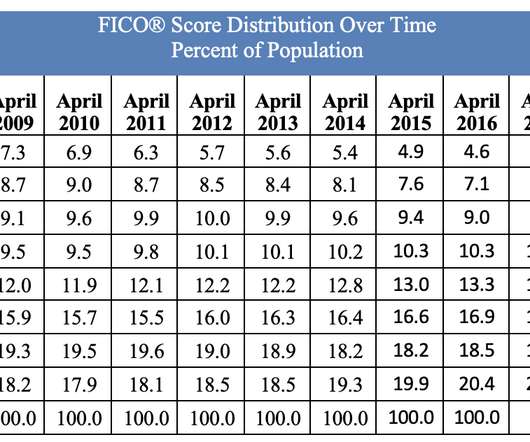

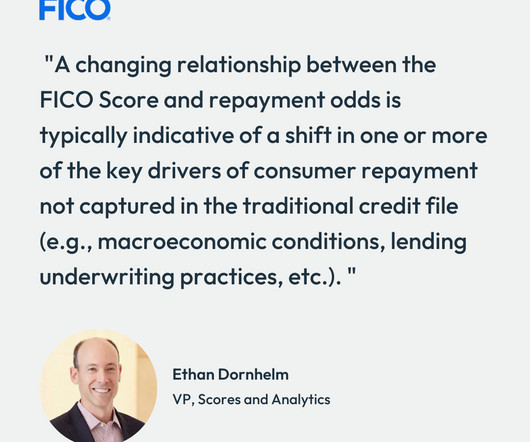

What the FICO Score is not designed to do is provide a specific, fixed estimate of creditrisk; we know from tracking the scores over three-plus decades that the relationship between the FICO Score and consumers’ likelihood of loan repayment can and does shift over time and across economic and financial cycles. Ethan has a B.S.

Participants and Influencers throughout the mortgage ecosystem have been told by the three main US credit bureaus through their jointly owned and controlled credit scoring firm, VantageScore, that the VantageScore can enable millions more consumers to gain access to a mortgage. million of whom will qualify for mortgage credit.

Traditional credit-scoring models are just drawing criticism, as well as a generation of competitors like Aire , which offer alternative credit-scoring models advertised as better-able to offer a “three-dimensional” view of customers in real time. The problem was he had no credit history.

China Construction Bank (CCB) hopes to reach more millennial consumers and is using alternative scoring services to improve decision making and improve financial inclusion efforts to reach this demographic. Partnering with the FICO team, we have significantly improved our origination efficiency while maintaining our risk profiles.

Once one gets in, their SAT score is officially useless to them; a mortgage underwriter won’t ask about it, credit card companies don’t care about it, and while we can’t be sure that no employer on Earth would make a hiring decision on the basis of it, we are fairly sure that the list of those that do is vanishingly short.

The Catch-22 is a familiar part of the early life of many consumers looking to get credit for the first time. They can’t secure underwriting because their financial file reveals no credit history, and they can’t establish any credit history because no one wants to underwrite them.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files. Read the full post 2.

Adjaoute said doing this goes far beyond what FIs can offer through manual, paper-based underwriting processes, which can keep applicants waiting for a month or longer. Evaluating creditrisk isn’t just about keeping fraudsters from getting loans under illegitimate identities. When Less Isn’t More.

Good news is ahead for those suffering from low FICO scores — according to reports this morning, civil judgements and tax liens will by and large be coming off of consumercredit reports. The move is one of the latest to keep negative information weighting down credit scores to a minimum. consumers, 6 percent of the total U.S.

FICO is best known for its consumercredit rating services, but the company revealed Tuesday (June 14) that it will launch a new product that rates the security of corporations. FICO said it hopes to provide a tool to underwrite companies’ cybersecurity levels. Known as Fair Isaac Corp.,

The consumercredit market has huge potential — trillions and trillions of dollars — and I wanted to ride that winner. The marketplace lending model is designed to offload the most pernicious risk in the lending business — creditrisk — to the investors who buy the loans from them.

So what were the loud points in an uncharacteristically quiet week in the race for the consumer’s whole paycheck? The partnership would apply Goldman’s lending technology to SMB loans on Amazon’s underwriting platform, according to unnamed sources. Big News of the Week: The Potential Goldman Partnership .

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content