This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At a time when organizations are increasingly exploring fiscal efficiencies, Adyen’s Intelligent Payment Routing ensures that enterprise businesses processing US debittransactions do not need to choose between cost, acceptance, or speed. Additionally, consumers are increasingly leveraging debit.

When the chips are down, consumers love and trust their debit cards. Among clear COVID-era trends is the embrace of debit for managing and mastering new realities. Debit cards remain the payment method of choice among U.S. Consumers have clung to debit even as the rest of their shopping behaviors have changed.

The ongoing pandemic has pushed more consumers online to carry out their shopping and banking, with fraudsters following suit. Bad actors have moved to take advantage of the rush to digital payments — particularly those made with debit cards — leaving banks and financial institutions (FIs) racing to keep them off their platforms.

US consumers are increasingly turning to debit cards for their everyday transactions, driving a significant surge in the number of transactions and overall spending. Card-not-present (CNP) transactions, which include online and digital purchases, also saw significant growth. per cent year-over-year increase.

Signature Debit Costs Maximizing Your Savings with AI Debit Routing One Caveat to Debit Routing Savings Debit Routing Background In order to cover the possible benefits of AI for debit routing, its important to have a solid understanding of what debit routing is and how it happens now.

Rent The Roo , an Australian firm providing consumer leases, is partnering with direct bank payments fintech GoCardless , in a move to remove punitive dishonour fees for its customers and deliver fully digital direct debit payments and increasing payment success rates.

Being too restrictive can result in a slew of false positives, however, irritating consumers whose cards are declined and frustrating merchants as would-be customers abandon their carts. Addressing security concerns is no trivial pursuit for debit issuers, as they incurred more than $1 billion in net fraud losses in 2019. 3D Secure 2.0

There are lot of PINless debittransactions available to capture, and First Data's migration to dual messaging on Star supports any method a consumer may choose at the point of sale.

Summary of Statistics in this Article In the United States, contactless payments accounted for 34% of all debit card transactions in 2023, a significant increase from 19% in 2020. According to Visa, tokenized transactions accounted for 85% of all mobile debittransactions in North America in 2023.

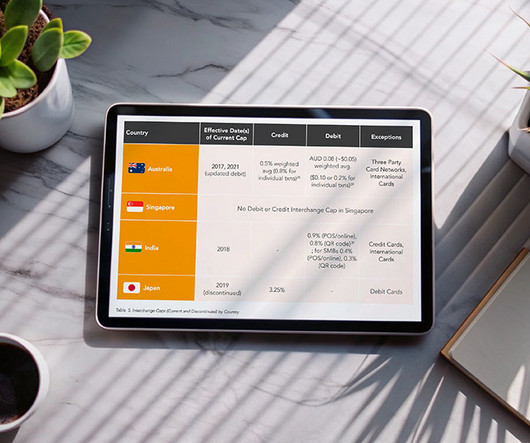

Covering four of the largest retail payment markets in APAC, namely Japan, India, Singapore, and Australia, the report examines the key trends around cost, consumer behavior, and regulation in each of these jurisdictions. Australia, for example, introduced caps on interchange fees in 2003 for both credit and debittransactions.

consumers worldwide are readying themselves for what they believe will be a long wait for things to return to something like pre-pandemic normal. Meanwhile, consumers are changing how they shop , how they pay , where they subscribe and what they consider secure. 70% : Share of consumers who prefer not to share biometric data.

That gives us a hint as to what might happen with debit spending, in a trend that was well-evidenced through the latest (and ongoing) earnings season. Namely, it will continue to be a favored payment method among consumers. But buy now, pay later (BNPL) options are gaining some traction.

As it stands, the bulk of the transaction fees consumers pay go back to the card issuers and the card networks, Hodges said – and, in turn, drive up costs for the merchant while triggering a proliferation in the size and number of individual fees. “I Not For Everyone.

The coronavirus pandemic has left consumers staying home when possible to stop the virus’s spread. These shifts have made digital banking and debittransactions more important than ever. FIs need to adjust their offerings accordingly to suit consumers’ new needs. Around the Next-Gen Debit World.

Whether it’s checking a bank account balance or placing an order online, consumers expect fast, convenient and immediate results. DE: The idea of fast funds continues to consume an outsized proportion of the industry’s headspace. Best of all, it’s instant, guaranteed and comfortable for the consumer.

Safety and convenience are twice as valuable when it’s your money (debit), and not the bank’s (credit). The September Next-Gen Debit Tracker® examines consumer behavioral shifts that are taking on an air of permanence as recovery and reopening unfolds all around. Broader Applications To Come. A recent survey of 1,000 U.S.

“Merchants and banks pass along those costs to consumers, either by raising prices or reducing quality or service. The complaint Filed in the US District Court for the Southern District of New York, the complaint explains that more than 60 per cent of debittransactions in the United States run on Visa’s debit network.

He said increased sharing of account information through third-party apps supports consumers’ desires, but it is not without its risks. This provides consumers increased transparency and control over their payments, eliminating unintended overdrafts, and reducing fraud. This has resulted in some delays and consumer confusion.

Recent studies have found that debit issuers lost approximately $1 billion to fraudsters targeting transactions at the physical POS or ATMs in 2019 — and this was before the ongoing pandemic expanded fraudsters’ opportunities to launch their schemes. Debit And The Fraud Catch .

Rent The Roo, an Australian company providing consumer leases, has announced a partnership with GoCardless , a global leader in direct bank payments. The partnership will allow Rent The Roo to remove punitive dishonour fees for its customers while delivering fully digital direct debit payments and increasing payment success rates.

As Phase 2 for debittransactions gets underway, the movement represents an option to transition to the two same-day windows now in place for credit transactions. With same-day debit , Larimer said, “consumers know their true balance faster.” “We’re seeing robust use of same-day ACH credits,” said Larimer.

CO-OP saw credit and debittransaction counts fall precipitously in the early weeks of the pandemic, as low as 30 percent. After all, there are only so many groceries and essential items consumers can buy; now, they are increasingly looking to buy other goods and services. It’s slowly picking up just a little bit,” he said.

There will soon be rules in place that govern how merchants and other entities make sure the accounts presented for debittransactions are valid — and in the process, cut down on fraud and chargebacks. FIs who are processing WEB Debits from their Treasury clients, must ensure those clients have an account validation process in place.

In addition, the number of people making mobile payments in stores is on the move in Vietnam and more than four in 10 credit and debittransactions were processed through contactless technology in the United Kingdom last year. As it stands, consumers in the U.K. Finance, according to reports. In addition, almost 7.4

billion non-prepaid debit card transactions in 2018, solidifying debit as a staple payment type. Consumers only see a small part of what is involved in using this method, however. This month’s Deep Dive delves into merchants’ debit routing choices and the factors that can sway them to select one network over another.

A new year has begun, but the pandemic continues to throw financial and operational curveballs at banks, businesses and their consumers regarding how they conduct daily tasks or routine payments. This includes shifts in which consumers are shopping and paying, and in the payment tools or methods they are using to finalize their transactions.

consumers prefer credit cards—further drive costs. Debit Cards: Debit card transactions generally have lower fees, ranging from 0.5% to 2.0%. PIN debittransactions are less expensive than signature debittransactions. Unlike Europe, where interchange fees are capped at 0.3%

And though the bulk of that took place though direct deposit activity (think payroll) and B2B transactions, P2P and consumer bill pay saw tens of thousands of payments. This sets the stage for increased adoption of same-day payments across consumers and the merchants who serve them. percent on each transaction.

Widely publicized data breaches and hacks have made today’s consumers especially concerned about fraud. Cautious shoppers may find comfort in debit, with fraud losses associated with the payment method declining over the past several years. A Big-Picture Approach To Thwarting Debit Fraud. Get the full scoop in the Tracker.

Cybercriminals have more opportunities than ever to swipe debit card numbers and PINs from online consumers, and false websites, large-scale data breaches and skimming tools can compromise account information. Consumers — especially those in the U.S. — Fraud And The Problem Of Convenience.

The conversation took place against a backdrop where, as reported in the Next-Gen Debit Tracker , non-cash payments have been rising 6 percent a year, and where payroll cards and debittransactions are gaining ground.

To that end, the Big Tech companies that reported earnings over the last several days — Alphabet ( Google ’s parent), Amazon , Facebook , Twitter among them — showed that eCommerce, and the ads that keep eCommerce top of mind for consumers (and, of course, the corporates that cater to them), are on an upswing. Ads, Catching Eyes.

More than 40 years after its debut, the Automated Clearing House Network becomes the first payments system in the country to offer ubiquitous faster payments to every consumer and business in the U.S. The flexibility of the ACH Network allows debit payments to be scheduled in advance. via all banks and credit unions. Today (Sept.

In line with recent findings showing consumers’ preference for debit , growth of that payment method outpaced credit growth among owner CUs. Debit sales volume grew by 8.76 from last year and debittransactions grew 7.4 percent, while credit sales and transactions both grew by 6.4

Credit union service organization (CUSO) PSCU compared the 19 th week of 2020, which concluded on May 10, to the same timeframe in 2019 to discover the impact of the pandemic on consumer spending and shopping trends. The average debit card purchase amount rose 19.9 percent jump in debit card spend for the week ending May 10.

The pandemic and economic headwinds have spurred millions of consumers to eye their finances with caution. In an interview with PYMNTS, Steve Sievert , executive vice president of PULSE Network , said debit has clear advantages for users who want to spend what they have on hand — and not expose themselves to more debt.

Consumers who previously paid for purchases by swiping or inserting their cards at in-store point-of-sale (POS) terminals are now turning to contactless cards and online shopping to safely and easily obtain needed goods. These two forces appear to be driving an increase in consumers’ use of touch-free debit payment options.

But business was substantially disrupted, he said, as the pandemic hit, and consumers pulled back on discretionary spending. As had been seen with payments networking peer Mastercard, Visa said that its latest quarter showed greater traction in debittransactions than in credit. trillion.

Merchants, too, enjoyed the tailwinds of a strong economy and sanguine consumer mindset. Drill down into the numbers, and the term “falling off a cliff” comes to mind, as healthy transaction and sales volumes at key merchant customers faced massive headwinds — and only now are starting to show a bounce off their nadirs. In the U.S.

As of today (November 7), some services have now been restored such as Wifi, Moodle, DCB and debittransactions, among others. The attack was discovered on Thursday (November 1) and the lockdown lasted for nearly four days.

The company noted that the offering provides an easy and quick way for developers to tap into a trusted gateway for credit and debittransactions. The gateway can be configured for PWA in minutes, especially for current Braintree merchants.

In a new PYMNTS interview, David Barnhardt, executive vice president of product at GIACT , which offers fraud detection and account validation tools, talks about an upcoming change by NACHA, national administrator of the ACH network, to make internet-initiated debittransactions (WEB debits) safer and more seamless.

For NACHA, there’s a rollout of a different sort, with far-reaching impact on how, who and when consumers and enterprises see funds flow. First, an explanation: The movement is, for debittransactions, an option to move away from overnight processing, where “classic ACH” transactions reside, to the two same-day windows now in place.

For instance, when a customer of one bank opens an account with another institution, the new bank gains visibility into the customer’s transaction history and account balances from their original bank, while the new bank is also able to initiate fund transfers or debittransactions from the customer’s account at the original institution.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content