This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ACH Network volume surpassed 2 billion transactions in August, an increase of more than 10 percent compared to the previous year. This impressive growth demonstrates that businesses and consumers are choosing to use ACH payments.”. In July, NACHA announced that debit and credit transactions totaled more than 5.7

Summary of Statistics in this Article In the United States, contactless payments accounted for 34% of all debit card transactions in 2023, a significant increase from 19% in 2020. According to Visa, tokenized transactions accounted for 85% of all mobile debittransactions in North America in 2023.

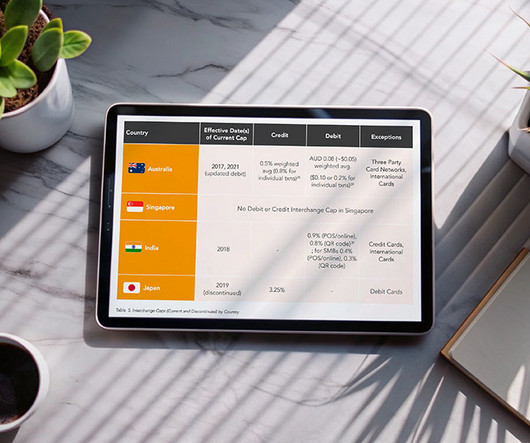

Covering four of the largest retail payment markets in APAC, namely Japan, India, Singapore, and Australia, the report examines the key trends around cost, consumer behavior, and regulation in each of these jurisdictions. Australia, for example, introduced caps on interchange fees in 2003 for both credit and debittransactions.

CO-OP saw credit and debittransaction counts fall precipitously in the early weeks of the pandemic, as low as 30 percent. After all, there are only so many groceries and essential items consumers can buy; now, they are increasingly looking to buy other goods and services. It’s slowly picking up just a little bit,” he said.

. “Governments, financial institutions, businesses and consumers are all reaping the benefits the ACH network provides.”. billion ACH debit and close to 2.3 billion ACH credit transactions made in the third quarter of this year. billion ACH debit and close to 2.4 According to NACHA , there were more than 3.3

That gives us a hint as to what might happen with debit spending, in a trend that was well-evidenced through the latest (and ongoing) earnings season. Namely, it will continue to be a favored payment method among consumers. Increases in debit spending helped to buoy results, overall. trillion, while credit slipped 9 percent.

Merchants, too, enjoyed the tailwinds of a strong economy and sanguine consumer mindset. Drill down into the numbers, and the term “falling off a cliff” comes to mind, as healthy transaction and sales volumes at key merchant customers faced massive headwinds — and only now are starting to show a bounce off their nadirs.

Visa posted fiscal second-quarter results that showed a precipitous falloff in cross-border volumes late in the quarter amid the coronavirus pandemic, alongside what it termed a “significant deterioration” in spending that was evident in March. Cross-border volume was off 2 percent. Card present volumes were down 45 percent.

He said increased sharing of account information through third-party apps supports consumers’ desires, but it is not without its risks. This provides consumers increased transparency and control over their payments, eliminating unintended overdrafts, and reducing fraud. This has resulted in some delays and consumer confusion.

consumers prefer credit cards—further drive costs. Larger merchants, with higher transactionvolumes, have more negotiating power and can often secure lower rates. Small Businesses: Small businesses, processing less than $1 million annually, typically pay higher fees, ranging from 2.5% to 3.5% per transaction.

As it stands, the bulk of the transaction fees consumers pay go back to the card issuers and the card networks, Hodges said – and, in turn, drive up costs for the merchant while triggering a proliferation in the size and number of individual fees. “I A Highly Personal Decision. Not For Everyone.

“Merchants and banks pass along those costs to consumers, either by raising prices or reducing quality or service. The complaint Filed in the US District Court for the Southern District of New York, the complaint explains that more than 60 per cent of debittransactions in the United States run on Visa’s debit network.

There will soon be rules in place that govern how merchants and other entities make sure the accounts presented for debittransactions are valid — and in the process, cut down on fraud and chargebacks. FIs who are processing WEB Debits from their Treasury clients, must ensure those clients have an account validation process in place.

As Phase 2 for debittransactions gets underway, the movement represents an option to transition to the two same-day windows now in place for credit transactions. With same-day debit , Larimer said, “consumers know their true balance faster.” “We’re seeing robust use of same-day ACH credits,” said Larimer.

To that end, the Big Tech companies that reported earnings over the last several days — Alphabet ( Google ’s parent), Amazon , Facebook , Twitter among them — showed that eCommerce, and the ads that keep eCommerce top of mind for consumers (and, of course, the corporates that cater to them), are on an upswing. Ads, Catching Eyes.

2017 marks another significant achievement in the evolution of the ACH Network, as transactionvolume was exceptionally strong and Same Day ACH was made fully available,” said NACHA Chief Operating Officer and General Counsel Jane Larimer. That propelled the value of the network’s transactions to more than double the U.S.

In line with recent findings showing consumers’ preference for debit , growth of that payment method outpaced credit growth among owner CUs. Debit sales volume grew by 8.76 from last year and debittransactions grew 7.4 percent, while credit sales and transactions both grew by 6.4

A new year has begun, but the pandemic continues to throw financial and operational curveballs at banks, businesses and their consumers regarding how they conduct daily tasks or routine payments. This includes shifts in which consumers are shopping and paying, and in the payment tools or methods they are using to finalize their transactions.

Credit union service organization (CUSO) PSCU compared the 19 th week of 2020, which concluded on May 10, to the same timeframe in 2019 to discover the impact of the pandemic on consumer spending and shopping trends. The average debit card purchase amount rose 19.9 percent jump in debit card spend for the week ending May 10.

Consumers who previously paid for purchases by swiping or inserting their cards at in-store point-of-sale (POS) terminals are now turning to contactless cards and online shopping to safely and easily obtain needed goods. These two forces appear to be driving an increase in consumers’ use of touch-free debit payment options.

The added attribute of speed provides additional flexibility and options to a system that has the capacity to process credit and debittransactions, payments and robust information together, domestic and international transactions, business and consumer payments, and more.

For NACHA, there’s a rollout of a different sort, with far-reaching impact on how, who and when consumers and enterprises see funds flow. For this calendar year, Larimer said NACHA is projecting 50 million transactions: “We are pleased with the volume so far … and we are expecting to see more use from same-day debits.

For instance, when a customer of one bank opens an account with another institution, the new bank gains visibility into the customer’s transaction history and account balances from their original bank, while the new bank is also able to initiate fund transfers or debittransactions from the customer’s account at the original institution.

Merchants, particularly those with substantial transactionvolumes, should negotiate terms and fees with their payment service providers or switch to a low cost payment processor like Clearly Payments. Encourage Debit Card Usage: Debit cards generally have lower interchange fees compared to credit cards.

In the first 6 weeks of 2024, Thredd , a leading modern payments processor serving clients globally, has seen an atypical early-year uptick in debit and prepaid payment transactions. Both in terms of month-over-month and year-over-year (YoY) growth, volumes have grown across several business verticals.

Gross dollar volume was up 9 percent to $1.2 the company said, total volumes stood at $388 million, up from $378 million a year ago and bifurcated between $199 million in debittransactions and the remainder in credit transactions. Cross border volumes were up 13 percent. percent year over year to $2.76

Vending machines aren’t about soda and salty snacks anymore — even if, at the consumer level, that’s what most people think of when they think about the technology. That volume increases over time and then levels out at about month 10.”.

Within that top line, payment volumes were up 10 percent to $1.9 trillion, as measured on a constant dollar basis — up on consumer credit and higher holiday spending — and where the United States was about 43 percent of that tally. do not require a signature anyway, with transactions under certain dollar thresholds.

As consumers become used to, and increasingly embrace, life lived digitally, financial institutions (FIs) of all sizes must prepare for seismic shifts in how customers access financial services, communicate with their FIs and make payments. She added that the commercial card side of the business has “tanked” as travel volumes disappeared.

Tomorrow, April 13, signing a receipt at the end of a Mastercard credit or debittransaction at the physical POS will become a relic of payments history. It’s a change that’s long overdue for many consumers. Consumers like Karen Webster, who – in a conversation with Mastercard U.S. transaction … and had to sign.

As transactionvolumes or the complexity of the ACH services increase, institutions or service providers must enhance their fraud detection and prevention mechanisms. Authorization requirements Before initiating ACH debittransactions, NACHA requires that entities obtain explicit, written authorization from the customer.

In some situations, a transaction that has already been processed may not stay that way if it’s reported by the RDFI as a failed transaction later on. Consumers also have 60 days from the date of any statement containing an ACH debittransaction to dispute it with NACHA. per transaction.

This is without friction, and where consumers, borrowers and businesses receive funding 24/7, in the ways they want and on demand. Much has been made in this space about push payments , which assures instant and “safe to spend” funds (meaning the payment cannot be reversed) delivered to a consumer’s account.

Among the advantages are the ability to offer installments, offering local-based credit cards (that don’t even use the Visa or MasterCard brand), the option to offer better approval ratings locally, avoiding international charges for the consumer, and superior fraud management. In Brazil, 80 percent of all transactions involve installments.

For example, over 70 percent of Walmart’s chip-based transactions are debit – and giving customers the option to sign instead of key in PIN is a big deal. Visa] has demanded that we allow fraud-prone signature verification for debittransactions in our U.S. percent to 2.08

Consumers today have more payment options than ever, but debit and credit cards remain the most commonly used methods. As we move through 2025, shifting economic conditions, technology advancements, and changing consumer habits continue to influence payment preferences. Debit Cards U.S. Total credit card debt 0 $1.2

Lawsuit Details According to the lawsuit, at least 60% of all US debittransactions run on Visas debit networks. Since many people use debit cards every day, the Justice Department is alarmed by what it sees as a systematic effort to limit competition for debittransactions. As Attorney General Merrick B.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content