This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As money moves between banks, consumers, businesses and beyond in a complex cycle, credit and debit cards continue to play a leading role in the payment experience, said Chris Como, Head of Cards and Money Movement at FIS.

Now with Fortis, the legacy is continued. Current and future Fortis users can expect seamless activation and enhancements with zero programming or implementation costs. Transactions are automatically reconciled, keeping all payment data in one place, making things efficient for endusers.

What’s more, financial barriers continue to impact quality of life for people globally. Describe how Almond FinTech ensures the affordability of cross-border transactions for end-users. Almond’s SOE puts end-users at the core of our mission. Today’s cross-border payment solutions also lack transparency.

In an interview with Karen Webster, Ariff Kassam , CTO at NuoDB , delved into the roadmaps FIs should develop as they move to the cloud over a timeframe that best aligns with endusers’ evolving (and sometimes rapidly changing) needs. A lot of people play lip service to continuity,” said Kassam.

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

Judges were looking for solutions that demonstrate genuine innovation that truly solves an issue and delivers benefits to endusers. The platform offers global and local acquiring, 100+ payment methods and comprehensive payment processing and orchestration—all accessible through a single, seamless API.

PayU continues to lead innovation in digital payments, making life easier for both merchants and end-users, while driving eCommerce growth in the country.

The fallout from the collapse of Synapse continues, with several partner banks facing a lawsuit alleging mishandling of customer funds, and one of those banks insisting that enduser funds it once held were moved by the BaaS platform before it went bankrupt.

Andrew Doukanaris Ambassador, The Payments Association While vIBANs have positive use cases, challenges exist in limited monitoring of the enduser, alignment with the PSPs risk appetite, and the lack of a consistent framework to mitigate financial crime and regulatory risks. Common standards would bring consistency and confidence.

Why do some embedded analytics projects succeed while others fail? We surveyed 500+ application teams embedding analytics to find out which analytics features actually move the needle. Read the 6th annual State of Embedded Analytics Report to discover new best practices. Brought to you by Logi Analytics.

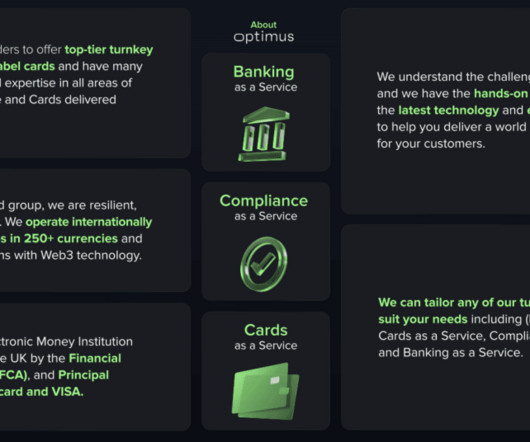

Optimus’s solution enables corporate and retail end-users to send payments utilising local banking rails. E-money license and technological prowess Optimus’s e-money license and advanced core banking/card processing technology platforms provide a solid foundation for its continued success.

Undoubtedly, fintech and payments will continue to serve as pivotal forces shaping the financial landscape, but what trends will define the market next year? Jeff Parker, CEO, says, “Digital payments will continue to grow rapidly, with mobile wallets expected to reach 4.8

Increasingly, consumer and corporate endusers of various platforms are seeking a more seamless experience, and the owners of those platforms are finding a big opportunity to integrate a range of financial products and services, from payments to financing. But across use cases, Bloh said two key themes are emerging.

Payment : If the user stops charging early, the final payment reflects only the electricity used, and the remaining reserved funds are released. Though it required complex operational changes, the result is the opposite for the end-user: A considerably simplified experience.

While Open Banking initiatives and data integrations between banks and FinTech firms have begun to target corporate and small business (SMB) endusers, new research out of the U.K. has warned that small businesses are largely shunning the opportunity to unlock their financial data. In a recent report from the U.K.

The payment landscape continues to expand each year, offering a vast array of payment methods for endusers and processing options for merchants. Payment gateways, processors, and service providers now provide comprehensive end-to-end solutions that maximize payment reach and minimize risk.

PayU continues to lead innovation in digital payments, making life easier for both merchants and end-users, while driving e-commerce growth in the country. The post Two Clicks and Purchased: PayU Brings Payment Simplicity to Colombia With Google Pay Integration appeared first on The Fintech Times.

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. Although the technology exists, it’s ultimately the enduser who will dictate how (or if) to use it. What Faster Payments Hasn’t Solved … Yet.

As commercial payments continue to evolve, Mastercards new programme will slash lengthy onboarding processes, unlocking efficiency for all VCN ecosystem participants and accelerating VCN usage in an $80trillion serviceable market. Mastercards approach is transforming commercial payments.

One thing is certain: The seismic shifts have shone a spotlight on the fact that cash (and even plastic cards) has seen – and will continue to see – dwindling use. To get there, according to some of the executives we queried, agility is key, and responding to endusers’ demands will be paramount.

By joining the Engage Programme, Sumsub aims to streamline customer onboarding, reduce fraud risks, and foster trust, ultimately improving the digital experience for end-users. They require continuous fraud prevention measures that extend beyond just the user onboarding phase.

.” Consumers will not see big changes Anish Kapoor, CEO, AccessPay Looking at the impact of CBDCs from a consumer’s perspective, Anish Kapoor , CEO, AccessPay , the bank Integration-as-a-Service provider, did not think users would notice a radical transformation.

As such, services integrated into mobile phones, tablets, computers, Internet of Things (IoT)-connected devices and more may mean a more convenient service for end-users, but as Cohen noted, this monumentally increases the “attack surface” upon which cyberattackers can infiltrate and compromise. A Regulatory Minefield.

. “As money moves between banks, consumers, businesses, and beyond in a complex cycle, credit and debit cards continue to play a leading role in the payment experience,” said FIS Head of Cards and Money MovementChris Como.

While this strategy can yield results, it can also create silos, hampering a bank’s ability to achieve one of the most vital goals of DX: seamless integration of operations that boost efficiency and improve the end-user experience. “Banks are technology companies,” Rio Tinto recently told PYMNTS.

While FinTech innovators continue to drive competition with a focus on product functionality and an optimal enduser experience, businesses are often forced to use outdated tools, according to Frank Dux , managing director of CoCoNet. The Drive To Upgrade.

Service providers are increasingly understanding that, like consumers, businesses demand a better and more seamless end-user experience. The higher the level of anti-fraud risk you build into your transaction monitoring rules and into your platform, the more clunky the system becomes for endusers,” he continued.

Over the last three years, the open banking model has continued to proliferate in markets around the world — even in jurisdictions, like the U.S., where there is no open banking regulatory mandate. Citi Drives ISO 20022 Adoption With Volante.

Alternative payment methods like digital wallets, account-to-account (A2A), and buy now, pay later (BNPL) continue to gain popularity. Companies across the payments value chain need to deliver exceptional end-user experiences and ensure technology, data and operations platforms are transformed to drive revenue, cost efficiency and control.

DBS continues to explore further blockchain applications, including securities tokenisation and digital trade finance. The bank is also exploring Programmable Rewards, a system for creating digital voucher programs with a focus on environmental, social, and governance (ESG) initiatives.

Judges were looking for solutions demonstrating genuine innovation that truly solves an issue and delivers benefits to endusers. The Payments Innovation category recognises a product, solution, or project that has broken new ground within payments.

This is part of Swiss4’s recently launched application that combines financial services and high-end lifestyle management, the first of its kind in Switzerland. With Marqeta’s platform, Swiss4 can swiftly design and introduce novel payment features, continually enhancing the enduser experience.

This partnership delivers significant value to endusers, and we act as an extension of the SI’s team, providing end-to-end payment support.” “Our Channel Partner Program is designed to meet these needs by integrating our robust global payment functionality with the expertise of System Integrators.

This collaboration with Newline further enhances Stripe’s ability to deliver compliant embedded money movement solutions for their platform clients and their endusers. Software platforms look to Stripe to simplify money movement so they can offer embedded, compliant financial services to their own business customers.

With its commitment to best-in-class technology and customer-centric products, Jaja consistently prioritises their endusers. TrueLayer’s open banking-powered instant payments capabilities means we can continue to harness the future of payments while optimising our technology and enhancing our customer’s user experience.”

Forter’s technology uses the speed and sophistication of AI to detect patterns across vast datasets and the savvy of fraud experts to continuously update its models. With over 400 banking channels, both global and local, we always put G2A.COM users first. G2A.COM continues to champion strong security measures across the industry.

“Daily use of mobile payment platforms is becoming increasingly common, with users citing the security, reliability and convenience of digital solutions as core driving factors. “As familiarity and understanding of NFC continues to grow, so too does demand for additional applications and use cases for the technology.

Devices and end-user computing emerged as the second most important investment priority for the finance sector, with over a third (36 per cent) of respondents planning to invest in this area in 2024. I look forward to continuing to work with our customers towards a brighter future!”

The collaboration between dLocal and iTransfer aims to address these challenges by offering competitive rates, real-time currency updates, and enhanced flexibility for end-users. “Offering our users competitive rates and reliable payout methods is crucial to our mission of supporting financial needs in emerging markets. .”

Galileo continues to power most of the leading fintechs in the US and provide a one-stop-shop for a wide variety of payment methods,” said David Feuer, CPO at Galileo. ” Enabling wire capabilities benefit endusers in several ways: Fast Transactions: Recipients receive their funds on the same day they’re sent.

. “Now, almost two years after the acquisition, a greater integration has happened, so critical capabilities got integrated into what we know as Visa Cross-Border Solutions” to continue delivering global money movement solutions for banks, fintechs, FX brokers, and other payment institutions, according to Rohit.

“Our partnership with Unlimit will provide massive benefit to endusers, by allowing Alchemy Pay to offer wider global coverage, lower costs, and improve transaction success rates.

Ensuring a smooth process with Tribe is key for end-user functionality. We look forward to continued growth over the coming months and years.” Joshua Vittori, CEO of Orenda, commented: “Orenda has been able to issue 10,000 cards in under two months with Tribe being the processor.

The concept of embedded banking has opened up a new frontier for financial service providers to drive holistic, elevated experiences for end-users. But the continued evolution of FinTech has made integration far more accessible, and today, it’s up to those FinTech providers to facilitate connectivity.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content