This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Just ask the estimated 42 percent of small- to medium-sized businesses ( SMBs ) that continue to use paper checks to make B2B payments. Today's Most Valuable UseCases. Payroll is one usecase that emerged early, and Ledford said this will continue to grow as businesses approach the holiday season.

Andrew Doukanaris Ambassador, The Payments Association While vIBANs have positive usecases, challenges exist in limited monitoring of the enduser, alignment with the PSPs risk appetite, and the lack of a consistent framework to mitigate financial crime and regulatory risks.

Increasingly, consumer and corporate endusers of various platforms are seeking a more seamless experience, and the owners of those platforms are finding a big opportunity to integrate a range of financial products and services, from payments to financing. But across usecases, Bloh said two key themes are emerging.

Over the last three years, the open banking model has continued to proliferate in markets around the world — even in jurisdictions, like the U.S., where there is no open banking regulatory mandate. Citi Drives ISO 20022 Adoption With Volante.

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. Although the technology exists, it’s ultimately the enduser who will dictate how (or if) to use it.

Galileo continues to power most of the leading fintechs in the US and provide a one-stop-shop for a wide variety of payment methods,” said David Feuer, CPO at Galileo. ” Enabling wire capabilities benefit endusers in several ways: Fast Transactions: Recipients receive their funds on the same day they’re sent.

But for B2B payment solution providers, the need for speed was coupled with another challenge: Technologies had to be built to address new and emerging usecases as payment scenarios were rapidly altered, perhaps permanently. Customers now have to adapt a lot faster to new usecases.".

Small businesses and corporate end-users have emerged as powerful drivers of exploring new use-cases for open banking and PSD2 regulations. But it’s not the only use-case for open banking. ” With new funding , Vaccino said Yapily will continue to focus primarily on the U.K.

Real-time rails continue to gain traction as solution providers debut new tools wielding existing instant payment infrastructure to enhance their offerings to business customers. They want a user-friendly solution, but most importantly, they want those funds," he said. Bank Of America Wields SWIFT gpi.

With experience and focus on innovative payment services across Real-Time Payments (RTP® and FedNow®), ACH, card solutions and alternative payment rails, Carl is well-positioned to support the FPC’s continued growth and innovation in faster payments.

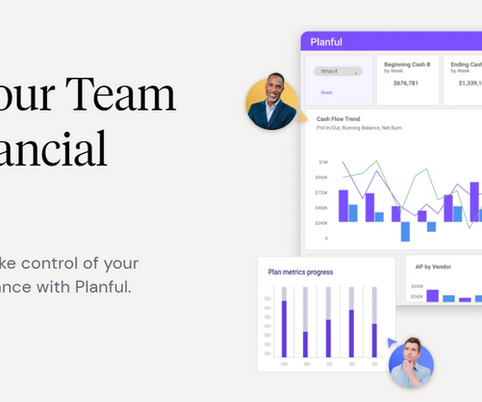

Key Features: 1) Enterprise-wide Connected Planning Seamlessly synchronize planning across organizations using clear, collaborative formats and dashboards. 3) Good Time to Value Rapidly model scenarios, collaborate with stakeholders and make swift decisions from a unified user experience.

Virtual Accounts, which enable instant refunds and payouts, among other key capabilities that help Payment Service Providers (PSPs) unlock the full potential of open banking payments for a vast range of markets and usecases.” “Our

ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. ISV software products are tailored to meet the specific needs of industries and users. Customer Support In-house support teams maintain direct relationships with end-users for assistance.

The small business FinTech arena continues to blossom as more developers explore ways to address a market historically underserved by traditional financial institutions (FIs). “We think of the user experience as critical and want to apply this philosophy on the business side.” The Back-End Strategy: Flexibility.

Speakers: Elizabeth McQuerry, Glenbrook Partners; Mike Sklow, Goldman Sachs; Samson Rajan; JP Morgan; Miriam Sheril, Form3 1:30pm-2:10pmCT: Panel Session – Business End-Users Mega UseCases (City Beautiful Ballroom AB) As more capabilities become available for faster payments, business endusers are finding creative ways to use the services.

Your Always-on Intelligent Assistant – Analyzes millions of data points and flags potential errors, working continuously to help you accomplish more. AI Integrations At Planful, their vision lies in delivering a complete, off-the-shelf AI solution for structured and dynamic planning usecases.

The telecommunications industry is an early first usecase of the technology, Clear Co-Founder and Executive Chairman Eran Haggiag told PYMNTS in a recent interview. The company plans to use the funding to ready its software for enterprise adoption and explore additional verticals into which it can expand. ClearMetal.

However, the idea that digital assets are exclusively some form of currency is slowly falling by the wayside as different usecases are emerging and being rapidly adopted. The potential usecases and benefits for users are hazy at best. In recent years, digital currencies have been all the rave.

FinTechs and banks continue to develop new solutions to address many of the biggest pain points of global business payments, from speed to foreign exchange. Yet in today’s fast-paced world, which is continually moving toward real-time payments, innovators are struggling to develop this ecosystem quickly enough.

It may be an open road for open banking as, three years after the rollout of the second Payment Services Directive (PSD2), bank-FinTech collaborations and new initiatives unlocking bank account data continue to flourish. But it may not always be smooth sailing ahead.

With a focus on addressing these data pain points, EvoluteIQ connects businesses to technology designed for "citizen users" — that is, endusers that are not data analytics by specialization.

As Red Hat ’s Global Director of Financial Services Richard Feldmann explained, the heart of the embrace and appeal of open source technology is the need for speed, and to evolve usecases for endusers (consumers and enterprises) in a more robust and secure fashion. Making Old ATMs New(ish).

At present, he continued, what has been challenging to consumers is that any one of those behaviors is usually tied to individual cards within their wallets, but the siloed nature of those activities can change with the APIs that bundle functionality. Defining The Visa Next Ecosystem And UseCases. The Roadmap.

In a recent interview with Karen Webster, Kaplan said that the core of AI in banking is to facilitate better, faster, more informed decision-making for the enduser to improve their experience (and boost their lifetime value to the FI). Another usecase is application processing. That’s not good customer service.

Money management, said Turner, is part of “an end-to-end” financial experience that leverages other Mastercard assets, such as Ethoca , for dispute resolution. The partnerships with FinTechs, she said, allows the flexibility to create “customized” solutions for different endusers’ money management desires.

Australia's New Payments Platform (NPP), its real-time payments rail, continues to gain traction according to the latest figures from the network. As more payment usecases emerge from distributed ledger technology (DLT), some solution providers are looking toward industry-specific applications of blockchain.

We do, however, see merchant enthusiasm for wallets increasing, as well as continuous improvements in consumer adoption. Additionally, our tech partners are really starting to understand merchant challenges and working with our merchants to address key usecases to help streamline a secure checkout experience.”.

In this comprehensive guide, we'll explore everything you need to know about RPA - from what it is and how it works to its benefits, usecases, pitfalls and more. Robotic Process Automation (RPA) is a game-changing technology that enables businesses to automate repetitive and mundane tasks using software robots.

The FPC conducted the latest survey of payments system stakeholders to gauge progress and perceptions around faster payments, trends, usecases, and challenges in the United States. This current installment of the Faster Payments Barometer illustrates that faster payments adoption continues to rise.

Liability needs to be shared across the chain, he said, but the first pieces of data and the initial relationships between the end-user and the organization that they are directly interacting with are the most important. The Micro Level. Integration must be simple and developer-friendly, he advised.

Before that, Greenland worked in enterprise sales for GoCardless, where he built global customer solutions and expanded customer relationships with varying usecases, including platforms, marketplaces and e-commerce businesses.

Virtual Accounts, which enable instant refunds and payouts, among other key capabilities that help payment service providers (PSPs) unlock the full potential of open banking payments for a vast range of markets and usecases.” “Our Todd Clyde, CEO of Token.io Todd Clyde , CEO at Token.io

Integrating native USDC and CCTP enhances Sui’s utility, security and interoperability for users and developers, with the intent of bringing more liquidity to the network, streamlining transactions, and improving market efficiency across the ecosystem. Users can seamlessly send, spend and save with digital dollars.

The inaugural Faster Payments Barometer was widely circulated and received well over 700 responses from a broad array of payments stakeholder segments including financial institutions, core processors, payment network operators, business endusers, acquirers, fintechs, and more. The survey was conducted from Sept. 18 – Oct.

However, there is a new game in town [in which] the FinTech actually empowers the bank to enable its own services, such as disbursements, for its corporate clients and all the way through to the clients’ endusers or recipients.”. Consumerization Continues.

As open banking frameworks continue to encourage bank-FinTech collaboration , the financial services market is exploring new ways to unlock data — not only with banks, but with each other. The impact of open data and data integration frameworks on the payroll sector is only one of several industry shifts the market is witnessing today.

Do clarify your card’s purpose and intended user benefits. Different usecases require different security, regulatory, and technological configurations. When possible, opt for providers that maintain continuity between sales and operations teams to ensure alignment and accountability. Also, clarify support structures.

These features collectively enhance budgeting, forecasting, month-end closes, and what-if scenarios, offering a single source of truth in real time. It allows finance teams to continue leveraging their familiar Excel models while taking advantage of modern automation and AI capabilities. Limited out-of-the-box apps and reporting tools.

Efforts were also made to advance digital assets, tokenization and central bank digital currency (CBDC) experimentation with initiatives such as Project Guardian and Project Orchid expanding to include more usecases and moving towards “live” pilots.

FinTech still exists as a fragmented market, where businesses striving to offer payment services to endusers pick and choose among providers, integrate with those providers, and must often navigate across complex technological and regulatory hurdles as they expand into new markets.

Head of Digital Transformation Jonathan Holman said in a statement, pointing to the “speed, transparency and ease of use” that endusers require from their banking services. Earlier this year, the bank announced “an experiment with Telefonica to explore potential usecases for superfast 5G networks in banking.”

With new technologies and even more usecases, prepaid cards are being used to deliver access to a wide range of payments, whether it’s from an employer or simply a gift card amount from a friend. which can provide ways for providers to ensure these products are valuable to the enduser. The Move Away From Cash.

Banking and financial services continue to be disrupted by leaner, new-to-market fintechs andchallenger banks, as well as shifting economic and regulatory conditions. Amid the pressure to deliver results, IT teams continually face challenges in keeping up with the day-to-day demands of the business. Thu, 08/22/2019 - 12:37.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content