This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

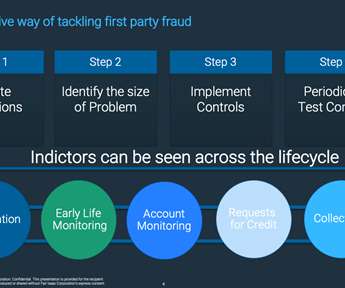

Here are some key types of risks that merchants should be mindful of in payment processing: Fraud Risk: Fraud risk involves unauthorized or deceptive activities aimed at exploiting the payment system for financial gain. This can include stolen credit card information, identitytheft, or fraudulent transactions.

Traditional third-party fraud entails some form of impersonation, whether through stolen card credentials or someone taking over your identity. In this scheme, criminal gangs have zeroed in on out-of-country students to buy their identitycredentials and bank accounts as they leave to return to their home countries.

Traditional third-party fraud entails some form of impersonation or stolen identity, whether through stolen card credentials or someone taking over your identity. Cross-border fraud is also exacerbated in the UK, EU and Middle East by a lack of cross-border credit bureau facilities.

The growth in digital payment fraud comes as activity has moved away from card-present transactions in an ecosystem protected by EMV authentication standards. The DoJ has since charged the man with one count of money wire fraud, three counts of money laundering and one count of aggravated identitytheft.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content