This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The company were asking me to advise them on the production of a ratings model, to help them rank their customers, old and new, for risk. For example, many industry sectors have bespoke credit reference agencies (such as Dynamar ) that offer risk grades and recommended creditlimits.

Credit scoring is widely used in South Africa to determine the risk of credit applicants — using this kind of objective, precise measure of risk lets banks, retailers and other organizations lend with more confidence, which in turn means more people get approved for credit. About the Empirica Score.

Addressing Portfolio Risk in Economic Uncertainty: Part 3 (2022). Building portfolio risk resilience into customer management. Lenders must adopt a similar mindset as they manage the financial health of their consumer lending portfolios to insulate their existing assets from potential portfolio risk volatility. Saxon Shirley.

Lenders must adopt a similar mindset as they manage the health of their consumer lending portfolios to insulate their existing book of business from potential risk volatility. Of course, creditrisk is only one aspect of portfolio health. Two-layered risk appetite approach to customer management without FICO® Resilience Index.

Banks offer creditlimits to borrowers that would seem punitively low in much of the Western world, so there is a pent-up demand for online alternatives. That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have credit cards, but are hampered by limits that are too low.

Many operations can now be automated, such as remote account opening, requesting creditlimits, deposits, and brokerage accounts. . “They are adopting user-friendly web and mobile applications, significantly reducing service delivery costs. It’s a win-win.”

That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have credit cards, but are hampered by limits that are too low. X Financial’s offerings include a balance transfer credit card product and an unsecured, high-credit-limit loan product.

In total, Prosper extended more than USD $225M in credit access to these consumers. Prosper also proactively mitigates creditrisk and meets the increasing credit demand for creditworthy customers based on their monthly updated FICO® Scores. Millions of consumers in the U.S.

Calculating an appropriate and timely offer for a creditlimit increase is made more accurate by reassessing customers with the FICO® Score, which analyzes their credit bureau data from all their credit accounts. The post LIFECARD Uses FICO Score to Grant More Credit appeared first on FICO.

The “innovation” VantageScore claims can score more people is simply the weakening of credit score criteria. The minimum criteria needed to produce the FICO Score aren’t arbitrary — they are the result of decades of research into risk assessment. A mortgage would be a big leap up the credit ladder.

The changes will create a bigger gap between consumers deemed to be good and bad creditrisks,” noted the Journal. The changes seem to herald more conservatism in credit scoring , and greater attention to risk tied to debt. We definitely are finding pockets of greater risk.”.

In some instances, this helps them offer consumers new credit opportunities, and in other cases it might illuminate risk,” noted Paul DeSaulniers, Experian’s senior director of Risk Scoring and Trended/Alternative Data and Attributes. For the credit invisible, the data can show lenders should take a chance on them.

The ability for lenders to start analysis of transaction flows such as level, frequency and volatility allows them to better track performance and risk in real-time. For example, it can be used in onboarding a customer, determining a creditlimit extension, a recovery treatment and even to pick up suspected fraud.

Doing it right means using customer data and rapidly delivering hyper-personalized, risk-aware offers that match customers’ needs and financial commitments at any given time via a channel that matches the customer’s preference to maximize the response rate on every interaction. .

Many lenders in markets outside the US use FICO® Scores to assess the risk of consumers applying for loan, but don’t continue to monitor those consumers’ risk using the FICO Score. This regular monitoring also enables FICO analysts to identify any developing creditrisk trends occurring in the Russian market.

Home Blog FICO Top 5 Customer Development Posts of 2022: Digital Banking and Pricing Opti The most popular posts in our Customer Development category dealt with digital banking, optimizing credit line increases, loan pricing and machine learning for creditrisk models. Here are extracts from those customer development posts.

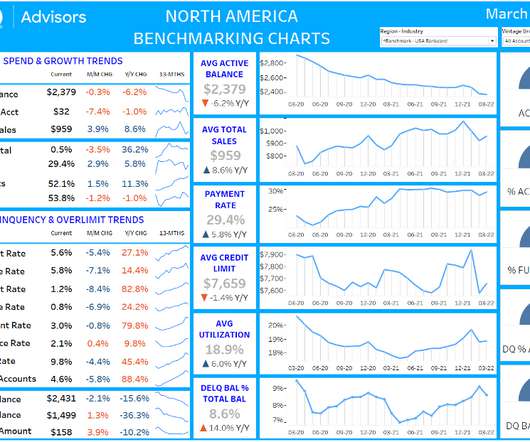

The following credit card performance figures represent a national sample of approximately 130 million accounts that comprise FICO® Advisors’ Risk Benchmarking solution. Overall credit card utilization has been trending back up but is more a function of creditlimits rather than increasing balance.

The credit bureaus below consider payment history and other information to determine business credit scores and risk factors. In turn, these credit scores inform business credit vendors, lenders, and external stakeholders about any credit issues and provide suggested creditlimits for specific businesses.

This can include strategies such as offering discounts for prompt payment or revising credit policies to reduce the risk of bad debts. Furthermore, the receivables turnover ratio can help businesses to set creditlimits for their customers. Q: How does the receivables turnover ratio assist in financial decision-making?

Additionally, the company must underwrite risk, and is on the hook in the event of fraud or returned items. This risk is reflected in processing fees, which are higher for online transactions. These companies can leverage private data to price creditrisk for customers already on their platform. Source: Finix.

The two entities will work together to help newcomers from countries including Australia, India, Kenya, Mexico, and Nigeria to leverage their credit history from their home country to help them access higher creditlimits when applying online for financing in Canada.

That may start with a secured debit card, she said, or a low-limitcredit card. The fraudster uses those cards, pays the bills on time, applies for higher creditlimits and gets a bank account. These are well-oiled machines.

Banking and CreditRisk: Ramps card is a charge card (balance due monthly) typically with a creditlimit based on the businesss finances. Ramp partners with a bank (Synchrony Bank initially, now Citibank for issuance and credit facilities) to offer the card. Any economic stress on its customer base (e.g.,

This blog dives into 10 major types of Loan Management Systems (LMS), exploring how these powerful solutions can automate your processes, mitigate risk, and drive growth. Co-lending module: Facilitates collaboration between multiple lenders for joint funding, risk sharing, and efficient loan management.

The area where the action of closing a credit card account may have impact on a FICO® Score is with evaluation of revolving account utilization. This is simply a ratio that looks at how much of your available revolving creditlimits are being used. The higher revolving utilization percentage the greater the risk.

In his 2016 annual letter to shareholders , Bezos outlined Amazon’s goal of expanding Amazon Lending: by continuing to work with partner banks to manage the bulk of the credit, the retailer can mitigate creditrisk and calm investor nerves. Today, Amazon has expanded its business lending to the US and UK. Amazon SMB Lending.

Banks are reserving tens of billions of dollars against potential credit card and loan defaults. They’re eyeing risk exposure while at the same time trying to help consumers get back on their feet. Recalibrating Risk. The prospect of extending credit, of course, brings key issues into focus, primarily those of risk and fraud.

Section 1071 amends the Equal Credit Opportunity Act to require financial institutions to report information concerning applications made by women-owned, minority-owned and small businesses.

But getting a clear picture of customers’ true financial position, while treating at-risk borrowers appropriately, continues to pose a headache for lenders. On the one hand, reducing mortgage default enforcement and the promotion of payment holidays are distorting unsecured creditrisk analysis.

These metrics provide valuable insights into how well your team collects payments, manages risk, and maintains customer relationships. Accounts receivable turnover ratio Accounts receivable turnover ratio, or AR turnover ratio, is a financial metric that measures how efficiently a business collects its outstanding credit sales.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content