This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Of the seemingly inexhaustible uses of artificial intelligence (AI) in the financial sector, its applications around managing creditrisk and optimizing payment services are among the most promising. Our research shows that 92.9 percent are doing so in creditunderwriting. Our research shows that 92.9

These circumstances have brought to the fore what has long been a central concern for lenders: assessing and managing creditrisk. This vital task is complicated even in normal times due to the multitude of financial risk factors in play at any given time. percent employ it for creditunderwriting. percent today.

. “AI’s contribution extends to intelligent underwriting, where it enables the creation of sophisticated risk profiles by analysing a wide range of data, including non-traditional indicators that might be overlooked in manual processes.

After a 2018 that had its highs and lows, what might 2019 have in store from a creditrisk management standpoint? Here are three key developments in credit scoring that we will be keeping an eye on in the new year: Consumer-Contributed Data Takes Center Stage. 2018 SCE Credit Access Survey. revolver vs. transactor).

a leading payments technology company, has achieved significant results by creating a centralized underwriting management solution on the FICO® Decision Management Platform (DMP). Additionally, we have transitioned certain processes downstream with no negative outcome on KYC validation and no increased risk to the organization.”.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. A key driver of successful financial inclusion is the ability for lenders to effectively gauge the risk of an underserved consumer.

A low FICO score for a consumer can have the perverse effect of preventing them from having access to a second chance through manual underwriting. We all know that having a higher credit score helps a consumer gain access to credit and get better terms from a lender. JessicaButalla@fico.com. Tue, 07/19/2022 - 16:11.

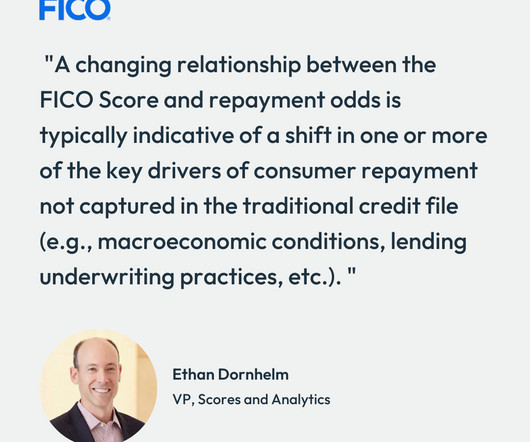

What the FICO Score is not designed to do is provide a specific, fixed estimate of creditrisk; we know from tracking the scores over three-plus decades that the relationship between the FICO Score and consumers’ likelihood of loan repayment can and does shift over time and across economic and financial cycles. and Canada.

In my last blog post , I shared a new FICO research study on credit trends in auto lending. This shift may signal an increase in creditrisk for the industry because six-year loans have historically had higher delinquency rates. The post Auto Loan Credit Quality: Hazardous Road Conditions Ahead?

As digital lending services continue to gain traction, lenders are prioritizing technology solutions for automated underwriting, fraud prevention, loan application, and creditrisk analysis. The post 102 companies automating loan origination for digital lenders appeared first on CB Insights Research.

The “innovation” VantageScore claims can score more people is simply the weakening of credit score criteria. The minimum criteria needed to produce the FICO Score aren’t arbitrary — they are the result of decades of research into risk assessment. In a previous post , I pointed out that our research showed around 7.4

As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem ranging from originations, underwriting and account management to collections and asset-backed securitization. in management science/operations research from UC San Diego. Ethan Dornhelm.

There has been much discussion and several studies over the years regarding the potential value of leveraging rental data in assessing consumer creditrisk. Which raises the question: Should rental data be widely reported to the three primary consumer credit agencies (CRAs)? Does Rental Data Make Thin Files Fatter?

A press release issued this week said that BNB Bank, a community bank operating across the New York and Long Island metropolitan area, will integrate PayNet technology to enhance its underwriting process for small business loans. In another statement, BNB Bank EVP and Chief Lending Officer Kevin L.

Thin-file credit applicants could go through a fairly painstaking process to build credit with low-value cards, but that wasn’t a good answer for him. The actual business, Varma noted, was the product of a long research period, since building a better credit-scoring experience is complicated.

This year our judges, in alphabetical order, are: Sidhartha Dash, research director at Chartis. He has held various roles in product development, risk management, software development and consulting for banks, hedge funds and software firms, including Standard Chartered Bank, TCG Group, HCL and Cognizant.

Primarily, Reckon provides small and medium-sized enterprises with cloud accounting solutions, but now, it’s utilizing the data it has about small businesses to its advantage by partnering with alternative lending company Prospa to underwrite loans to its SME users. “This is transforming the creditrisk analysis process. .

More than two-thirds told researchers that compliance and regulatory requirements are holding them back from providing more trade finance in the short term, while cost control pressures were identified as the top challenge for FIs’ (financial institutions) trade finance operations.

Developed by FICO in partnership with LexisNexis Risk Solutions and Equifax, this innovative credit score utilizes alternative data—data not included in the traditional credit bureau file. The inclusion of this alternative data leads to a more reliable estimate of consumer creditrisk and helps score more than 26.5

FICO Scores, of course, play an important role in the risk management and transparency that powers the secondary market. Now VantageScore is claiming that its score can be used instead in GSE underwriting (and by extension, securitization), as a one-to-one replacement for the FICO Score. Could a clean swap-out work?

Vitto (India) Vitto is a MSME focused fintech startup using behavioural data for creditrisk profiling and automating credit decisioning with AI assistance. It simplifies the complexities of financial research and trading management, providing an institutional investment process accessible to all market participants.

SMBs and SMEs are typically underserved by banks because they generate less revenue for banks and are riskier to underwrite. Traditional banks hesitate to underwrite business accounts for tech startups because startups are high-risk businesses with untested founding teams (regardless of previous work experience).

Today’s post is about solving the elusive problem of first-party fraud and features commentary from Julie Conroy (Research Director at Aite Group) and Jack Alton (CEO at Neuro-ID). Julie—I know you spend a lot of time researching this subject. For your benefit, we will periodically reproduce these conversations in FICO blog posts.

‘PayFac’ technology simplifies underwriting and onboarding. Additionally, the company must underwriterisk, and is on the hook in the event of fraud or returned items. ‘PayFac’ technology simplifies underwriting and onboarding merchants. TABLE OF CONTENTS. A decade of online payments innovation.

In fact, solutions developed by the FICO Scores team enable credit access for an estimated 1.3 It means investing in research to validate forms of alternative data. billion consumers globally using alternative data. Using new approaches to improve financial inclusion. Financial inclusion also means investing in innovation.

AI will lead to more tailored products and services, reduced risk, increased productivity and smarter decision-making in all areas of banking and finance – be it fraud prevention, creditrisk scoring, insurance underwriting, claims assessment or investment strategies.

In his 2016 annual letter to shareholders , Bezos outlined Amazon’s goal of expanding Amazon Lending: by continuing to work with partner banks to manage the bulk of the credit, the retailer can mitigate creditrisk and calm investor nerves. Today, Amazon has expanded its business lending to the US and UK. Amazon SMB Lending.

Digital life insurance startups offering easier underwriting processes for life insurance (like requiring no medical exam) are already seeing an increase in applications as customers don’t want to deal with agents or medical exams in the time of social distancing. appeared first on CB Insights Research. Banking and Lending.

India’s FinBox landed an undisclosed amount of pre-Series A funding, reports in Inc42 said this week, with investors at Arali Ventures leading the investment in the creditrisk management technology startup. FinBox plans to use the investment on product research and development. Australia’s ANZ Bank led a $1.56

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content