This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Creditrisk continues to remain one of the areas of concern for a majority of traditional and new-age lenders. Additionally, new-age lenders often cater to underserved or high-risk segments, increasing the […] The post Understanding the Different Types of CreditRisk appeared first on Finezza Blog.

The scoring methodology was developed by EFL Global and marketed by FICO as part of our FICO Financial Inclusion Initiative , designed to open up credit markets around the world to a larger number of unbanked and underserved consumers. The post A New Way to Score CreditRisk – Psychometric Assessments appeared first on FICO.

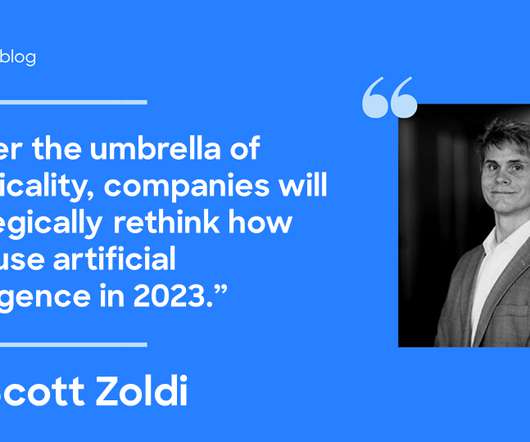

In fintech, this means AI systems that dynamically manage creditrisk, automate trading decisions, and even preemptively block fraud, all without human intervention.

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. They are one of our most sophisticated clients in terms of advanced analytics.”. by FICO.

In an effort to bridge what is increasingly being known as the “inclusion gap” for minorities, Visa is finding promise in supporting products for financial inclusion in the credit union and community bank portfolio. To hurdle the financial gap that exists for these underserved populations in North America.

The EFL score uses psychometrics and behavioral data to measure a person’s creditrisk based on an applicant’s answers to a series of interactive questions and exercises administered via an online assessment. 25% median Gini for its creditrisk models across geographies and segments. EFL has seen a circa.

Some of the top thought leaders in banking, finance, artificial intelligence, machine learning, and creditrisk came together in San Francisco to discuss the key trends and innovations in our industry. A key driver of successful financial inclusion is the ability for lenders to effectively gauge the risk of an underserved consumer.

It will provide localised digital banking services to everyone, including the underserved. I am confident that the consortium’s new virtual bank will bring fresh ideas and innovative solutions, to advance financial inclusion for underserved communities and instill diversity to Thailand’s financial landscape.”

Inaccurate and slow creditrisk assessment for [small- to medium-sized business (SMB)] commercial loan requests is one of the major reasons that over 50 [percent] of loans are currently declined by financial institutions (FIs),” said Roger Vincent, chief innovation officer at Trade Ledger.

“By contrast, growth in student loan debts outpaced inflation, being both greater in number as well as balances; this undoubtedly creates a drag on capacity for other forms of consumer credit.”. A New Way to Score CreditRisk – Psychometric Assessments. Using Alternative Data in CreditRisk Modelling.

Empower also announced it closed the acquisition of Philippines-based consumer credit and lending fintech Cashalo. Empower , a fintech helping to extend credit to underserved consumers, announced plans to acquire underservedcredit card provider Petal.

“We developed a unique underwriting platform based on alternative data points to evaluate creditrisk. Lendbuzz is addressing a large and underserved market, has innovative technological underwriting capabilities and unique customer acquisition strategy that supports their high growth.”.

In China , X Financial specializes in helping underserved prime borrowers and mass affluent investors by matching those borrowers with investors willing to loan them money. That means the big opportunity for X Financial comes from the 400 million or so Chinese consumers who have credit cards, but are hampered by limits that are too low.

Using remote sensing technologies on farmland, the bank assesses creditrisk based on crop growth and various factors. This approach ensures that even farmers in remote areas can access credit. This not only boosted the accessibility of SME loans but also contributed to the bank’s growth.

Instead, innovative analytic firms such as FICO are investing in identifying new predictive and compliant data sources to build models that accurately assess if underserved borrowers are in a position to successfully take on a new credit obligation.

The opportunity is also gigantic, Cheng told Webster, given that the country has some 800 million working adults, with less than half of them in possession of a credit card. X Financial specializes in helping underserved prime borrowers and mass affluent investors in China by matching those borrowers with investors willing to loan them money.

” In another statement, Moody’s Analytics Director of Product Management Ed Oetinger said the partnership with CapX will help the firm expand into an underserved segment of the market. . “We have not been able to find a comparable tool that incorporates both tradeline and financial statement data.”

But as more providers take steps towards extending mobile phone leasing to underserved markets, new demographics and segments with thin credit files, while offering the lasts handsets and access to high-speed services, they face a multitude of challenges.

Here's an example of why we need to focus more on practical uses of Generative AI: Open banking represents a huge revolution in credit evaluation, particularly for the underserved. Generative AI can be applied practically to produce realistic, relevant transaction data for developing real-time creditrisk decisioning models.

In total, Prosper extended more than USD $225M in credit access to these consumers. Prosper also proactively mitigates creditrisk and meets the increasing credit demand for creditworthy customers based on their monthly updated FICO® Scores. You can read more about this story in the full media release.

Machine Learning is simply another analytic technique; one that can help produce highly predictive credit scores which must also be explainable, with two important caveats: . The use of Machine Learning must be balanced with deep domain expertise in creditrisk modeling. ML does not create new data.

Finding a way to score millions without credit history. Círculo de Crédito , the fastest-growing credit bureau in Mexico, has used unique creditrisk scores from FICO to boost financial inclusion in Mexico and help an additional 20 million citizens access credit.

For example, variables such as screen resolution, the presence of banking apps, and the number and length of calls have all been shown to be predictive of creditrisk. Opening branches and installing ATMs in remote locations and lower-income neighbourhoods can improve access to credit for the underserved residents in those areas.”

They will integrate seamlessly with ULI through standardized APIs, enhancing risk management by leveraging comprehensive borrower data. This integration will help reduce operational costs, making credit more accessible to underserved populations and aligning with ULI’s goal of financial inclusion.

What these startups share is the goal of creating customer-centric banking products that target underserved individuals and businesses. Many of the startups disrupting banking are reaching customers who are either underserved by existing bank accounts or do not qualify to open an account (unbanked). Underbanked/Unbanked.

While the introduction of credit scoring technology introduced by FICO in the late 50's changed lending forever; it’s worth exploring what it takes to make a social impact today. It means the inclusion of credit markets that are less developed, where a larger part of the population is underserved. No, it's not.

The medical arena – including elective procedures like laser hair removal, dental, orthodontics and equipment, such as wheelchairs, Burnside noted – is a massive market that is largely underserved. Just one of Loan Hero’s medical equipment-focused practices, Burnside noted, pushes through $500 million in financing a year alone.

What those consumers — and the businesses that could potentially be serving them — need is a way to evaluate their actual risk level in the absence of the standard data that informs a traditional FICO score. Luckily, he noted, just such a font of data happens to exist for almost every member of that cohort.

A compliant bearer deposit token instrument would eliminate counterparty creditrisk and could enable a decentralised digital identity-based pre-validation protocol to deliver low-cost automated global compliance, transparency, and privacy. BIS Aurum) and interoperability solutions (e.g, Deutsche Bundesbank Trigger Solution).

When news of the financial crisis broke in 2008 and big banks all over the world were eschewing consumer and small business credit markets, Batine and Dunaev saw an opportunity — one that was particularly pressing in developing nations, an area of the world that was below the big banks’ radars.

Despite its benefits, Stripe’s PayFac model also means that the company absorbs more merchant risk by serving as a master merchant account, and that it’s responsible for downside risk in the event of chargebacks and fraud. Stripe’s market opportunity. Source: Stripe.

Here's an example of why we need to focus more on practical uses of Generative AI: Open banking represents a huge revolution in credit evaluation, particularly for the underserved. Generative AI can be applied practically to produce realistic, relevant transaction data for developing real-time creditrisk decisioning models.

We are excited by the value that Nubanks thought partnership and advice can bring to Tyme, particularly in areas like data analytics, creditrisk management, product development, and marketing. Recognising the systemic gaps in retail banking, especially for underserved communities, Tyme set out to redefine what a bank could offer.

Areas such as data analytics, creditrisk management, product development and marketing are key to achieving leadership in our markets. Coen Jonker, co-founder and CEO of Tyme Group “Nubank transformed financial services in Brazil. We are excited by the value that Nubank’s thought partnership and advice can bring to Tyme.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content