This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the ever-evolving landscape of datasecurity, staying updated with the latest standards and regulations is crucial. The Payment Card Industry DataSecurity Standard (PCIDSS) is no exception. With the recent release of PCIDSS v4.0, Changes in Requirement 9 of PCIDSS v3.2.1

Welcome back to our ongoing series on the Payment Card Industry DataSecurity Standard (PCIDSS) requirements. This requirement is a critical component of the PCIDSS that has undergone significant changes from version 3.2.1 a: This one’s all about verification. Consequently, PCIDSS v4.0

Welcome back to our ongoing series on the Payment Card Industry DataSecurity Standard (PCIDSS). We’ve been journeying through the various requirements of this critical security standard, and today, we’re moving forward to explore Requirement 5 of PCIDSS v4.0. compared to PCIDSS v3.2.1.

In our ongoing series of articles on the Payment Card Industry DataSecurity Standard (PCIDSS), we’ve been examining each requirement in detail. In this blog post, we will delve into the changes introduced in PCIDSS Requirement 8 from version 3.2.1 Conclusion: PCIDSS v4.0

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 Today, we’re discussing Requirement 6, which is crucial for protecting cardholder data. It mandates the use of vendor-supplied security patches and secure coding practices for in-house developed applications. PCIDSS v3.2.1

Security features include Payment Card Industry DataSecurity Standard (PCIDSS) certification, transaction verifications like 3DS/AVS, and user-set spending limits. The service is intended for common business expenses such as online advertising, software subscriptions, and logistics.

Historically, datasecurity has been treated as featureless and burdensome—but a necessary expense incurred by organizations. Today, we can tokenize anything from credit card primary account numbers (PAN) to one-time debit card transactions or social security numbers.

Card Verification and Authentication : BINs support the verification process by providing immediate access to the issuing institution’s information. Payment processors use this data to authenticate the card details, ensuring that the card being used matches the card type, issuer, and other key characteristics tied to the BIN.

Theyre easy to integrate and set up, with the host taking care of datasecurity measures, including PCI compliance and fraud protection. Businesses using self-hosted gateways must handle datasecurity measures and comply with industry standards like PCIDSS.

Ensure the gateway offers PCIDSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. Look for PCIDSS-compliant payment gateways that optimize the security of credit and debit card transactions. Learn More What is a Payment Gateway?

Key steps include application review, risk assessment, credit checks, and compliance verification. Step 4: KYC and AML Checks Compliance officers or automated systems integrated with KYC and AML verification services verify the identity of business owners and ensure compliance with anti-money laundering regulations.

Tokenization : Converts sensitive card data into a unique token, reducing the risk of data breaches. 3D Secure Authentication : Adds an additional verification step for online transactions, such as a one-time password (OTP) or biometric authentication.

The first step is implementing robust authentication processes, including multi-factor authentication, biometric verification , and tokenization , to enhance user access security. Empowering customers to be vigilant about their own security is another key aspect.

PCI compliance fee – This fee is usually charged by the payment processor or acquiring bank to ensure the business follows Payment Card Industry DataSecurity Standard ( PCIDSS ) requirements to protect customer data.

The payment gateway : this is a cloud-based payments software integrated with your website thats responsible for the secure transfer of your customers credit card information to your payment processor. Some payment gateways use tokenization to secure sensitive customer details.

To stay ahead of fraud means merchants must understand the threats, use trusted and secure providers, and keep up to date on payment security trends. So, let’s dive into payment security, touching on the basics of what you need to know to ensure secure payments. Q: How do I ensure online payment security?

It also ensures that datasecurity best practices, particularly PCIDSS (Payment Card Industry DataSecurity Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data.

Multi-Factor Authentication (MFA) Implementing multi-factor authentication (MFA) adds an extra layer of security to the authentication process. MFA requires users to provide two or more verification factors, such as a password and a one-time code sent to their mobile device.

Payment security A reliable Sage 100 payment processing solution will protect customer payment information by implementing robust security protocols and ensuring full compliance with Payment Card Industry DataSecurity Standards (PCI-DSS).

Enhanced securitytokenization and two-factor authentication reduces the risk of data breaches As we mentioned earlier, Click to Pay uses a datasecurity approach called tokenization to protect sensitive financial data from malevolent actors.

The primary security standards that payment systems typically adhere to include: Payment Card Industry DataSecurity Standard (PCIDSS): PCIDSS sets forth requirements for securing payment card data, including encryption, access control, network monitoring, and regular security testing.

Additionally, it includes security features such as tokenization, encryption, and fraud prevention tools to ensure compliance with Payment Card Industry DataSecurity Standards (PCIDSS). In addition to compliance measures, implementing fraud prevention tools enhances security and minimizes financial risk.

Verification : The encrypted PIN is sent to the card issuer’s system, where it is matched against the cardholder’s stored PIN. Transaction Approval : Upon successful verification, the card issuer approves the transaction, and the payment is processed. If the PIN is correct, the transaction proceeds.

Implementing robust security measures is another essential step. Merchants should invest in secure payment processing systems, utilize encryption technologies, and comply with Payment Card Industry DataSecurity Standard (PCIDSS) requirements.

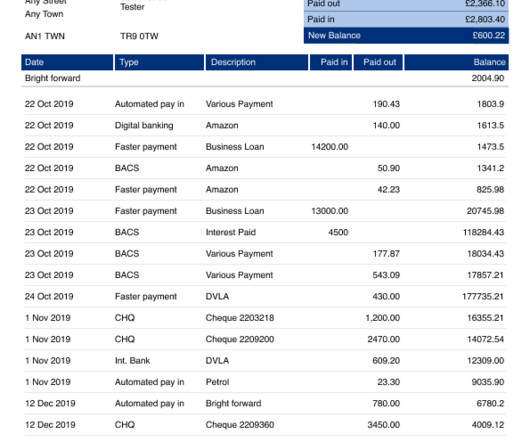

Whether you're a loan officer reviewing an application or a business owner ensuring your clients’ payments are in order, bank statement verification is integral to ensuring financial accuracy and fraud prevention. Let’s discuss bank statement verification and find answers to some of your biggest challenges.

Fraud detection and security tools: Merchant accounts often include tools and standards to prevent fraud and enhance security, including Payment Card Industry DataSecurity Standards (PCI-DSS).

Highest level of PCIsecurity compliance that keeps payment datasecure. Payment processors are responsible for communicating the details among various entities, whereas payment gateways deal with verification and approval. Not complying with the PCI can attract a fine of up to $500,000 per incident.

It will use magnetic secure transmission (MST) to transmit the relevant data when the smartphone is held at close range (a few centimeters usually) or tapped to your card reader. Step 5: Evaluate security and fraud protection The required level of vigilance will depend on the applicable regulations in your industry.

A little over two months ago, the FTC issued orders to nine card firms to provide information on how exactly retailers’ compliance with PCI standards is measured in regards to PIC DataSecurity Standards. In response, the PCI council has noted that the NRF’s letter is full of “unfounded assertions.”

Security Features Fraud and chargebacks are significant concerns for businesses accepting credit cards. To minimize risk: Look for PCI Compliance: The Payment Card Industry DataSecurity Standard (PCIDSS) is mandatory for all businesses that handle cardholder data.

Compliance and security Your PSP is responsible for ensuring that sensitive customer financial data is securely encrypted and stored according to the standards and regulations of the industry, such as PCIDSS (Payment Card Industry DataSecurity Standard).

Merchants must handle sensitive payment data to process their customers transactions, making it essential to protect this information. Acumatica-integrated payment solutions can meet various legal and regulatory requirements and keep your data safe using the latest security measures.

Biometric authentication, including fingerprint scanning and facial recognition, provides a highly secure and convenient method for user verification, reducing the risk of fraud and identity theft. Regulatory compliance is another critical aspect of ensuring security and trust in mobile payments.

Test different aspects of the solution, such as invoice creation, report customization, payment reminders, and payment verification. Also look for encryption protocols, user account access, and multi-tenant security measures. You can ask for a demo before investing in the software to gauge its usability and ease of use.

How Merchant Accounts Work The process of transaction handling When a customer makes a payment, their payment information is securely transmitted from the checkout to the payment processor for verification. PCI compliance. Scalability.

Overall, the payment gateway acts as a secure bridge that encrypts sensitive data, such as credit card details, to ensure the transaction is processed safely and efficiently. Finding a gateway that provides robust fraud prevention tools, encryption, tokenization, full PCI Compliance , and advanced verification is important.

Types of Debit Card Processing & Technologies Card-Present Transactions PIN-based Debit Cards : a debit card transaction where the customer enters a PIN for verification. PCIDSS Compliance This is the cornerstone of debit card security.

PCI Compliance Fees: Fees for maintaining compliance with Payment Card Industry DataSecurity Standards (PCIDSS). For example, transactions without proper address verification (AVS) may be downgraded, incurring additional charges of 0.1% per transaction.

Use Address Verification Services (AVS) AVS is a fraud prevention measure for online and card-not-present transactions. Train Your Staff To Handle DataSecurely For in-person transactions, it’s crucial your staff is able to take payments in an efficient and trustworthy manner.

With Plaid acting as the intermediary, your sensitive login credentials never get shared directly with Venmo, enhancing the security of your financial information. What Is Plaid Bank Verification? Plaid bank verification is the process employed by financial apps like Venmo to authenticate bank account ownership and verify funds status.

Enhanced Security & Trust for Gamers Players need a safe and seamless way to make transactions. A gaming payment gateway encrypts financial data, prevents fraud, and ensures compliance with security standards like PCIDSS, giving users peace of mind while making deposits and withdrawals.

Security and compliance are non-negotiable when dealing with credit card processing. Ensure the selected payment gateway complies with the Payment Card Industry DataSecurity Standards (PCIDSS) to protect your customers’ payment information.

Address Verification Service (AVS) A fraud prevention tool that checks the billing address provided by the cardholder against the address on file with the card issuer. Customer Information Protection The process of protecting sensitive customer information, such as payment card data, from unauthorized access or theft.

PCI-compliance fees – Businesses running credit card transactions must be compliant with the Payment Card Industry DataSecurity Standard (PCIDSS). This regulation is managed by the Payment Card Industry Security Standards Council (PCI SSC) and is meant to protect the cardholder’s data.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content