This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Wells Fargo & Co is seeking to sell its private-label credit card and point-of-sale (POS) financing unit as part of an ongoing strategic review of its businesses. Selling the private-label credit card unit would be a business reversal for the financial services group. Debit cardPOS purchase volume hit $102.9

Digital banks , for one, are teaming up with technology providers to accelerate settlement times for payments collected at the point-of-sale (POS). Legacy banks are similarly at work, with one major FI seeking to beat out FinTech competition by offering same-day access to credit card deposits.

We’re still navigating the pandemic — which means doing what we used to do offline, increasingly, through digital means. Merchants, he said, “need to make sure they not only accept credit cards but also contactless payments.”. Even waving the card at the point of sale (POS) may face headwinds because of transaction limits.

For SMBs, what’s in the cards … are more card readers. Morgan is focused on enabling payments for the millions of small businesses that are the lifeblood of Main Streets across the U.S. – Morgan seems to be banking on speed as a selling point to gain traction with smaller firms. To that end, the banking giant J.P.

That left FIs scrambling to “rapidly figure out how to get that same emotional and engagement outcome when the possibility of face-to-face is virtually nonexistent,” Randy Piatt , head of product solutions at card technology firm Ondot Systems , told PYMNTS in a recent conversation. Simple: Start with the cards.

A transformation toward contactless payments is underway at the nation’s credit unions as the public shuns cash and even physical cards to lower infection risks with COVID-19. It will likely alter global markets and regulations as the financial ecosystem becomes more digitized. The High Stakes Of Offering Contactless.

Contactless has existed for a long time, but consumers were slow to adopt, mostly because they didn’t have much of a compelling reason to do something differently — their cards worked fine. And at the point of sale (POS) at grocery stores, where they are still shopping in person, they are realizing something important.

Innovating on the point of sale (POS) for consumers isn’t a one-shot deal. They were staying digital because it was looking like the better game in town and one that consumers were actually enjoying enough to stick with. Because over the last six months, the consumer commerce journey has changed quite widely.

Quite to the contrary, if the various unnamed sources cited are correct, Amazon is thinking a lot about its hand-based payment technology these days, and not just about how it can be applied to the point of sale (POS) at Whole Foods and Amazon Go locations — as had been previously reported. JPMorgan Chase & Co.,

The trouble, Blackhawk Network CEO and President Talbott Roche told Karen Webster in a recent digital discussion, hasn’t been that consumers or merchants have had an adverse reaction to contactless payment methods — so much as they’ve had something of an inertial connection to cards. “A

For example, the digital channel — which had already been growing quickly to take up more of the holiday spending pie in recent years — is exploding as the pandemic has pushed consumers away from shopping in physical stores. The double-digit percentage growth didn’t come as much of a surprise. The Time To Engage Members Is Now.

With consumers being at the heart of a lot of startups, a new partnership between Yabx , the sustainable financial inclusion fintech, and PayCliq , the business payment tool provider, is looking to accelerate merchant credit capabilities. The Middle East and Africa (MEA) has emerged as a region that is no stranger to innovation.

Today at the annual Visa Payments Forum for Central and Eastern Europe, Middle East and Africa, Visa unveiled a suite of new products and services that will revolutionize the card and address the future needs of consumers, merchants and the financial institutions that serve them across the region.

That being obvious doesn’t make it any less true — or any less meaningful to those involved in payments and commerce. However, there is a growing hope that sound — yes, sound — can help solve the friction problem, promote omnichannel efforts and even reduce payment costs for merchants. Solving For Friction.

Supply and demand get a bit balanced in the digital realm. Card-not-present (CNP) transactions are increasingly eyed by fraudsters. Card-not-present (CNP) transactions are increasingly eyed by fraudsters. late last year, making it easier to pay for online purchases without entering credit card information.

Whether you run a small online store or a major brand, accepting electronic payments is a must for all businesses. According to Onbe, 73% of consumers prefer using digitalpayments like cards and payment apps. But to seamlessly receive these payments as a merchant, you’ll need merchant processing services.

With approximately 100 million MSMEs in Africa and 42 million in Nigeria alone, consumer payments on the continent are projected to exceed $2.1 AI scoring partner, Yabx is poised to speed up the uptake of digitalpayments by building a lending infrastructure for small businesses. trillion by 2025.

To address this, stakeholders including NETS Group and Liquid Group are working on interoperable QR payment solutions that are designed to simplify processes for merchants, Chia said. On the international front, cross-border payments have presented a different set of challenges.

Biometric payments are making another run at the grocery store, this time at the hands or Amazon. Amazon, the company that brought consumers scan and go, is about to bring consumers pay by hand — a new payment system designed to allow Whole Foods shoppers to pay for their groceries by merely waving at a scanner.

In the digital age of hospitality technology, restaurants have a trove of tools to help serve customers in their stores. Overall, merchants in the $1 trillion accommodation and food services market see digital innovation as key for staying competitive in the space. percent — innovated to remain competitive.

The pandemic required full-on digitization for many businesses to keep revenue flowing, but simply setting up shop online is no longer enough to keep customers happy. The sudden rush to digitize has led to an impressive transformation for many firms. Optimizing The Payments Experience. Brand Loyalty’s Surging Importance.

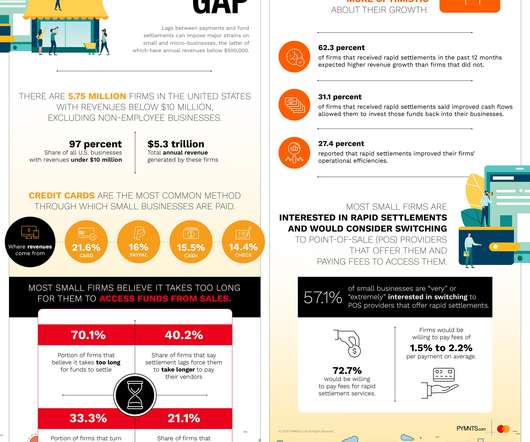

percent say it takes too long for funds to settle, which is felt when small business receive payments through checks or ACH. And nearly 66 percent believe it is “very” or “extremely” important for companies to have access to funds as soon as customers make payments. Even strong sales may not translate into a steady stream of cash.

That a market is massive and emerging as a target for digitization, does not necessary mean it will be an easy target to pursue — a lesson learned the hard way by Facebook in June when regulators hit the pause button on its adding payment capabilities to WhatsApp in Brazil. Leveraging an Ecosystem to Ride Out Uncertainty.

Volante CEO and Founder Vijay Oddiraju told Karen Webster during the latest This Week In Payments conversation that while the pandemic has been bad news, it has also opened up the door to innovation. . Digital innovations of every shape and size now all need to have been put into place yesterday. In the U.S.

A few weeks ago US economists were surprised when the Commerce Department reported that retail sales rose by 0.6% As consumers flock back to stores , some may be surprised and delighted to learn that they can use popular person-to-person (P2P) payment apps like Venmo and PayPal at the cash register. Let’s take a look. . Hello Panda.

The conventional wisdom that all a merchant must do to keep customers coming into stores or clicking through sites and pulling out wallets (digital and tangible) is to keep them satisfied is conventional, yes, but not wise. One way for retailers to offer a differentiating experience can be at the point of sale, said Vladic.

Since the migration to EMV in the largest card market in the world (the U.S. in October of 2015), the incidences of counterfeit card fraud at chip-enabled merchants have fallen sharply — some 76 percent, as reported by card networks. Once cards became significantly harder to clone, fraudsters took their bag of bad tricks online.

In the old world, he said, QSR transactions were all done at the point of sale (POS) in the store, and chargeback concerns weren’t high on the worry list because QSRs weren’t responsible for them. Making a digital addition is still a change to the customer experience.

Every weekday, 135 million American commute to work, an act that creates nearly $212 million in commerce potential a year according to the 2020 Edition of the PYMNTS Digital Drive report. But, he noted, it was also still just one of many to come. Unlocking Voice Commerce’s True Potential . And of those consumers, 51.2

Maybe a diner prefers to have the waiter bring the payment terminal to the table instead of disappearing with the credit card and all of its sensitive data — still common in the United States, though the famous European habit of settling the bill at the table is making inroads here at restaurants and even some upscale bars. Fresh Tech.

Visa announced that it will bring the power and ubiquity of installment lending to digital and physical points of sale (POS) through application program interfaces (APIs) that support the development of customized installment plan options for Visa cardholders. Where installment payments are available, they are well liked.

It’s the end of the workweek, and the PYMNTS Weekender is here to make sure you didn’t miss anything with the latest in payments and commerce news. The changes were outlined in a document sent to banks by the payments firm and would be the most sweeping structural change in a decade. and Canada.

Contactless payments market has been growing quickly. As digital infrastructure continues to advance, the ease and speed of contactless transactions are becoming increasingly attractive to consumers and businesses. What are Contactless Payments? Here’s a breakdown of each type and its growing significance: 1.

Through trial and error, the company has set up key financial pillars across payments, cash deposits, and lending. Amazon Payments. Amazon has aggressively invested in payments infrastructure and services over the last few years. Making payments more cash efficient for Amazon and frictionless for customers is a key priority.

There are billions of devices always on the internet, creating massive clouds of data exhaust whenever they are used to … enable commerce or make a payment,” Sondhi said. The device that nearly every Indian consumer owns and uses has become their onramp for digitalpayments — for both merchants and consumers. “The

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content