This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As a merchant, to understand tokenization for your own benefit, it’s critical to understand: What tokenization is, why it’s important for payments, and how it compares to encryption. How tokenization applies to being PCI compliant and meeting the 12 PCIDSS requirements.

Requirement 10 of the PCIDSS covers logging and monitoring controls that allow organizations to detect unauthorized access attempts and track user activities. In the newly released PCIDSS 4.0, to PCIDSS 4.0. Whether you’re currently compliant under PCIDSS v3.2.1 In PCIDSS v4.0,

Welcome back to our series on PCIDSS Requirement Changes from v3.2.1 PCIDSS v3.2.1 PCIDSS v4.0 c: Confirm that software applications comply with PCIDSS. - c: Confirm that software applications comply with PCIDSS. - In PCIDSS v4.0, In PCIDSS v4.0,

Ensure the gateway offers PCIDSS compliance, encryption, tokenization, and fraud prevention tools to safeguard transactions. The payment gateway collects and encrypts sensitive customer payment details and then securely sends them to the payment processor. Learn More What is a Payment Gateway?

The details are then encrypted and transmitted to a third-party payment gateway for authorization. Businesses using self-hosted gateways must handle data security measures and comply with industry standards like PCIDSS. But with more control comes great responsibility. This protects your business from any liabilities.

Card Verification and Authentication : BINs support the verification process by providing immediate access to the issuing institution’s information. Verification and Approval : The issuing bank reviews the transaction, confirms the cardholder’s account details, and assesses if there are sufficient funds or available credit.

Merchant Sends Transaction Request : The merchant’s POS system or online payment gateway encrypts and transmits the transaction data to the acquiring bank or payment processor. 3D Secure Authentication : Adds an additional verification step for online transactions, such as a one-time password (OTP) or biometric authentication.

Sends leverages AI to mitigate risks, comply with FCA, PSD2, and PCIDSS, and enhance client experience with secure and innovative services. Strict compliance with FCA, PSD2, and PCIDSS protects consumers and combats financial crime, but implementation demands resources and adaptation.

TL;DR The PCIDSS determines security protocols and sets the standards for payment security. It’s also critical to ensure card information is protected from data breaches with secure encryption and cybersecurity standards in place. How do two-factor authentication and “3-D secure” protect payment information?

Payment security A reliable Sage 100 payment processing solution will protect customer payment information by implementing robust security protocols and ensuring full compliance with Payment Card Industry Data Security Standards (PCI-DSS).

The payment processor : this is the payment services provider that handles the verification and transfer of data and funds between the financial institutions involved in that transaction. Payment verification Once the payment processor receives the now-encrypted payment information, it will be sent to the issuing bank for verification.

The gateway acts as the intermediary that collects, encrypts, and transmits transaction data to the payment processor. Fraud detection and security tools: Merchant accounts often include tools and standards to prevent fraud and enhance security, including Payment Card Industry Data Security Standards (PCI-DSS).

The first step is implementing robust authentication processes, including multi-factor authentication, biometric verification , and tokenization , to enhance user access security. Secure Network Configurations Configuring secure networks is fundamental to PCIDSS compliance.

Step 3: The payment services provider authenticates the transaction Once the customer selects a preferred card network, the merchants payment gateway will send the transaction details to the merchants payment services provider who will then contact the customers issuing bank for payment verification.

PIN Encryption : Once the customer enters the PIN, it is encrypted immediately to protect the information. Encryption ensures the PIN cannot be intercepted or stolen during transmission. Verification : The encrypted PIN is sent to the card issuer’s system, where it is matched against the cardholder’s stored PIN.

The primary security standards that payment systems typically adhere to include: Payment Card Industry Data Security Standard (PCIDSS): PCIDSS sets forth requirements for securing payment card data, including encryption, access control, network monitoring, and regular security testing. Digital Certificates.

Overall, the payment gateway acts as a secure bridge that encrypts sensitive data, such as credit card details, to ensure the transaction is processed safely and efficiently. Strong encryption builds trust with customers and reduces the risk of data breaches. Fraud detection and prevention are critical features of a payment gateway.

It also ensures that data security best practices, particularly PCIDSS (Payment Card Industry Data Security Standards) requirements , are followed to the letter to prevent any breach or loss of sensitive customer data. The company facilitates the transfer of information and funds between the customer’s bank and your business’ bank.

Its role is to encrypt and securely transfer your customers payment data to your payment processor. All the data transfer between the digital wallet and your payment terminal are encrypted and the system also uses tokenization to ensure iron-clad data security.

Additionally, it includes security features such as tokenization, encryption, and fraud prevention tools to ensure compliance with Payment Card Industry Data Security Standards (PCIDSS). Address Verification Service (AVS) and CVV verification should be enabled to prevent unauthorized transactions and reduce chargeback rates.

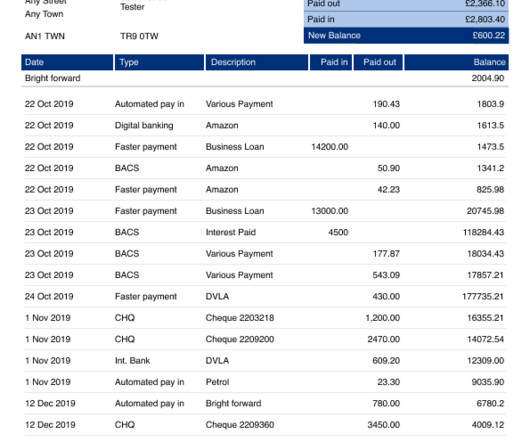

Whether you're a loan officer reviewing an application or a business owner ensuring your clients’ payments are in order, bank statement verification is integral to ensuring financial accuracy and fraud prevention. Let’s discuss bank statement verification and find answers to some of your biggest challenges.

Merchants should invest in secure payment processing systems, utilize encryption technologies, and comply with Payment Card Industry Data Security Standard (PCIDSS) requirements. Implementing robust security measures is another essential step. Promptly reporting any suspected fraud to the payment processor is essential.

At the heart of mobile payment systems are Near Field Communication (NFC), Quick Response (QR) codes, and secure elements such as encryption and tokenization. Encryption ensures that data transmitted during a transaction is scrambled and unreadable to unauthorized parties. Security is a critical component of mobile payment technology.

The payment gateway encrypts the data and securely transfers it to the card issuer for approval. To minimize risk: Look for PCI Compliance: The Payment Card Industry Data Security Standard (PCIDSS) is mandatory for all businesses that handle cardholder data. Ensure your provider complies with these standards.

Compliance and security Your PSP is responsible for ensuring that sensitive customer financial data is securely encrypted and stored according to the standards and regulations of the industry, such as PCIDSS (Payment Card Industry Data Security Standard).

Types of Debit Card Processing & Technologies Card-Present Transactions PIN-based Debit Cards : a debit card transaction where the customer enters a PIN for verification. PCIDSS Compliance This is the cornerstone of debit card security. Signature-based Debit Cards : Transactions verified by the customer’s signature.

Acumatica payment providers should comply with legal and regulatory requirements like Payment Card Industry Data Security Standards (PCI-DSS) , which safeguard payment data by implementing various security protocols. 3D Secure authentication requires an additional verification step during a credit card transaction.

Test different aspects of the solution, such as invoice creation, report customization, payment reminders, and payment verification. Also look for encryption protocols, user account access, and multi-tenant security measures. You can ask for a demo before investing in the software to gauge its usability and ease of use.

Advanced encryption techniques are used to protect sensitive data during transmission, ensuring that personal and financial information remains confidential. Compliance requires implementing robust security measures, such as encryption and authentication protocols, regularly auditing processes, and staying updated on regulatory changes.

Key Features of a Merchant Management System Merchant Onboarding The onboarding process begins with merchants submitting applications along with required documentation for verification. Compliance monitoring ensures adherence to regulations like PCIDSS and AML laws.

Here’s how it works: Encryption & Secure Transmission: The payment gateway encrypts the player’s payment details and securely transmits them to the payment processor. Solution with Segpay: Built-In Compliance Tools Segpay is a fully PCIDSS Level 1-compliant payment processor, ensuring secure transactions.

Ensure the selected payment gateway complies with the Payment Card Industry Data Security Standards (PCIDSS) to protect your customers’ payment information. Adhering to PCIDSS and employing advanced security measures like encryption and role-based access helps mitigate the risk of fraud and ensure compliance.

What Is Plaid Bank Verification? Plaid bank verification is the process employed by financial apps like Venmo to authenticate bank account ownership and verify funds status. Compliance Plaid adheres to data protection regulations like GDPR and CCPA, as well as financial industry standards such as PCIDSS.

Here are the security protocols that should be in place for new-age lenders: Data Protection: Advanced encryption and multi-factor authentication safeguard borrower information, ensuring that sensitive data remains secure.

Address Verification Service (AVS) A fraud prevention tool that checks the billing address provided by the cardholder against the address on file with the card issuer. Encryption The process of encoding sensitive data to prevent unauthorized access. A Acquirer The financial institution that processes payments on behalf of merchants.

Each transaction will include the standard details needed: address verification (billing address and zip code) card number; and card expiration date. Security and compliance Ensure that the payments platform prioritizes security and compliance with industry standards such as PCIDSS (Payment Card Industry Data Security Standard).

It also enhances security, as modern contactless payment options like digital wallets and chip cards are equipped with advanced encryption, protecting sensitive customer information from potential fraud. For higher transaction amounts, they typically require a PIN or biometric verification, offering enhanced consumer protection.

To reduce this risk, merchants should: Employ up-to-date security measures such as encryption and tokenization for transactions. Use secure payment gateways and adhere to Payment Card Industry Data Security Standard (PCIDSS) guidelines.

Positive Pay Files transmit a file of issued checks to corresponding banks daily, enabling verification of authorized payments. This includes implementing encryption, multi-factor authentication, and regular monitoring of access logs. Compliance with these regulations can help protect the business from legal and financial risks.

Verify that the provider is PCI-DSS compliant to ensure that your customers’ data is protected according to industry standards. Beyond compliance, look for processors that offer advanced security features like tokenization and encryption, which add layers of protection to payment information.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content