This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For companies looking to scale, Independent Software Vendors (ISV) are a crucial tool that provides specialized software solutions that integrate seamlessly with existing business tools. ISV integrations offer numerous advantages, from improved functionality to a superior customer experience. The Benefits of ISV Integrations 1.

Small business accountants have said they are now forced to manually transfer data between payroll and human resources solution providers Gusto and Zenefits after the two companies abruptly ended their application programming interface (API) integration, AccountingToday reported.

A pioneer in open banking, Neonomics unveils an innovative new product suite launched as Nello, with the goal to bring open banking to the next level through AI-driven solutions and seamless payments. Nello AI will be available as a white-label integration for financial institutions and others to easily integrate.

Through its wire transfer API, Galileo connects fintechs partnering with Community Federal Savings Bank (“CFSB”) with Fedwire via sponsor bank CFSB. By enabling Fedwire transfers, Galileo is helping fintechs capitalize on this growth, with a scalable solution that caters to the increasing demand for rapid financial transactions.

Conferma , the leading virtual card provider, has entered into a strategic partnership with the ground transportation automation and management platform, GroundSpan to facilitate simple, virtual payments for ground transportation. The strategic partnership was formed in direct response to customer demand for ground transportation integration.

These days, with the emergence of the cloud, open banking and application programming interfaces (APIs, the moniker “as-a-Service” applies to pretty much any business function that is now able to be outsourced to a third party. Technology brings the concept of flexible payments into reality. Flexibility Is Key.

Foursquare is offering small businesses (SMBs) and startups access to its geolocation API, according to VentureBeat reports on Friday (April 13). Now, Foursquare is extending this service to SMBs via its Places API for Startups.

In a major leap for subscription services, Trustly , the global leader in open banking payments, today unveiled its innovative AI-powered recurring payments solution poised to revolutionise how merchants handle repeat transactions through a single integration.

What it comes down to is a lack of integration and automation on both sides of the transaction.”. Instead, Grouchy said, application programming interface (API) technology can enable seamless integration of data within back-office systems and between the systems of two different businesses without forcing them into a particular solution.

While FinTech innovators continue to drive competition with a focus on product functionality and an optimal enduser experience, businesses are often forced to use outdated tools, according to Frank Dux , managing director of CoCoNet. The Drive To Upgrade. It can be much easier for banks to buy out-of-the-box solutions," he said.

The capabilities to unlock bank data and integrate new services into emerging FinTech platforms via APIintegrations is a FinTech trend that hasn’t ignored the B2B payments arena. Service providers are increasingly understanding that, like consumers, businesses demand a better and more seamless end-user experience.

The concept of embedded banking has opened up a new frontier for financial service providers to drive holistic, elevated experiences for end-users. What we’ve seen is an increasing demand from corporates to not have to do it themselves.”. Such functionality can drive retention for a firm’s own end-users, she said.

Founded in Edinburgh in 2018, BR-DGE is a payment orchestration provider on a mission for hyper-growth. The company enables enterprise merchants, financial institutions, platforms and payment providers access payment tools and products via a single integration.

Embedded versus integratedpayments: what exactly is the difference? Are these two payment models actually one in the same? Keep reading as we explain the key differences between embedded and integratedpayments. However, there are variations in each integration approach. of integratedpayments.

million in a funding round to go toward the startup's goal of providing a way for third parties to integrate banking services through an application programming interface (API), according to a report from TechCrunch. Unit has raised $18.6

The coronavirus pandemic was an unanticipated disruption for every business, but for organizations that remain mired in paper, it became what Dave Robertson , managing director of payment advisory services at Deluxe , described as “the ultimate stress test.” A Gradual Process.

SaaS companies deliver software applications over the internet on a subscription basis, simplifying access and management for users. ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. Primarily through direct-to-user subscriptions and third-party distributors.

Visa introduced a platform on Monday morning (April 22), complete with beta application programming interfaces (APIs), that will allow issuers and issuer processors to build and test new products. The initial beta APIs on offer will help those within the Visa ecosystem to create digital cards on demand and add digital services.

Instead, SaaS applications are hosted on cloud computing networks and users can access their functionality on-demand through the internet. In this article, we’ll explore the many benefits of SaaS and how to implement SaaS payments. What’s more, users don’t need to bear the cost of maintaining or updating the software.

The shift toward contextual banking has a tailwind in place as the financial institutions (FIs) that have been market leaders have been seeing strong deposit growth — and as corporate customers are growing those balances, they want to be able to see their account activity and cash balances visible within the same application on demand.

For those wanting to do more with QuickBooks, hundreds of third-party integrations step in to offer additional features and benefits beyond QuickBooks' native offerings. Still, with as many integrations as are available, some may find themselves overwhelmed.

Global tech firm Veritran has partnered with Swift , the world’s leading provider of financial messaging services, to enable financial institutions to offer an enhanced, streamlined and more transparent cross-border payment experience to their customers.

These days, with the emergence of the cloud, open banking and application programming interfaces (APIs, the moniker “as-a-Service” applies to pretty much any business function that is now able to be outsourced to a third party. Technology brings the concept of flexible payments into reality. Flexibility is Key.

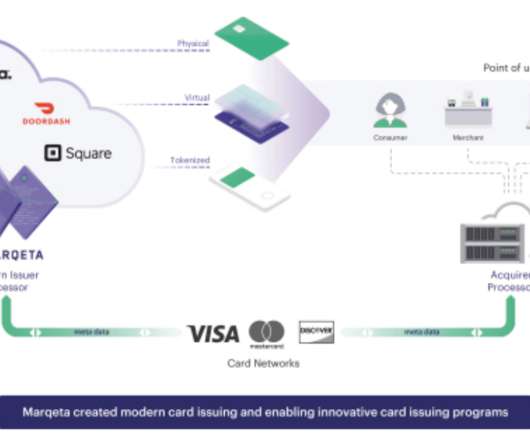

Marqeta , a cloud-based open API platform for modern card issuing and transaction processing, recently filed its S-1 in preparation for its shares to start trading publicly in June. Marqeta allows businesses to offer payment card products to customers without having to deal directly with a traditional bank. First name. Company Name.

That means financial functions beyond banking are taking advantage of application programming interface (API) data integrations, with productivity gains particularly large for business end-users of these products and services. Unlocking Data, Unlocking Opportunities.

EvonSys , a Global Elite Pega Partner and Platinum Sponsor for Pega World 2024, announces the launch of the EvonSys Payments Platform (EPP). This innovative platform is set to transform the landscape of cross-border payments, delivering new standards in traceability, transparency, and efficiency.

Fagan noted that payment networks such as Visa and Mastercard have been recording steep dips in credit card activity, where the shift has favored debit payments. The pandemic and the pivot to contactless payments have shown that consumers are open to using technology to conduct daily financial life.

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. Unlike payments facilitated by card networks like Visa or Mastercard, ACH payments are managed by a body called the National Automated Clearing House Association (NACHA). Let’s get started.

The new year has dawned with a number of cross-border payment pacts, done across blockchain and other means. In Pakistan, as reported by Coindesk, Telenor Microfinance Bank and remittance firm Valyou Sdn Bhd (a Telenor subsidiary) have launched a payment platform based on Alipay’s blockchain offerings. s Faster Payments service.

Veritran and Swift announce their collaboration that will enable financial institutions to offer an enhanced and streamlined cross-border payments experience to their customers. Users will also have full visibility of a payment cost, including the FX rate, upfront.

FinTech innovation has opened the floodgates for a stream of new platforms and products designed to help small businesses and corporates more efficiently manage money and make payments. Bridging the Payments Divide. Payments, and more specifically, initiating a transaction, can be a bit more difficult to accomplish.

Rather, banks around the globe began to understand the potential value in opening up customer data to third-party players, and with more bank APIs emerging in 2018, the year saw a surge in data sharing. Finserv Embraces The API. “I I think for our industry, APIs are a very positive innovation,” said Hubert J.P.

The financial services industry’s sudden support for application programming interfaces (APIs) has people talking about the power of data sharing. s Open Banking initiative encourage API development and adoption, with industry players acknowledging the technology’s ability to efficiently comply with data sharing rules.

Finastra , a global provider of financial software applications and marketplaces, today announced it has been selected by LGT to roll out instant payment services in Austria and Liechtenstein, with other markets to follow. Finastra’s payment hub provides banks with a future-proof, scalable and resilient payment processing system.

NYSE: JBL) today announced ongoing innovation between its payment solutions business unit and Revolut , a digital banking pioneer and global financial super app provider, to support the neobank’s rapid growth trajectory and global expansion in merchant acquiring.

With open banking technologies making their way beyond the world of consumer finance and into the business banking market, new use cases are emerging from the legislation that opens up bank account data and offers FinTechs opportunities for new functionalities via deeper data integrations. Bringing Order To Bank Data. Emerging Use Cases.

The company said in an announcement that business lending endusers are able to have an enhanced customer experience throughout the entire time of securing as well as drawing down on a loan. Ripple had joined forces with Finastra to let banking customers use blockchain payments network RippleNet per a report in October.

Competitive forces in the payments and financial services sector have driven two key trends in the U.S.: the acceleration of payments, and the adoption of open banking frameworks. Both are key to addressing the modern demands of end-users. Looping Into Faster Payments.

The Fall Member Meeting will bring together FPC members for two days filled with presentations on the most pressing issues in faster payments, panel discussions with industry experts, roundtables on timely topics, and engaging networking opportunities. Foundry Ballroom) Payment networks need volume to scale and keep costs low.

” The friction associated with manually downloading data across banking and financial platforms, and then having to normalize it to make it usable, presents a significant opportunity for open banking initiatives and APIs in the corporate cash management space. Open banking is not a regulatory requirement in the U.S.,

So it is with business, with payments, with the ways we pay — when and even where and certainly how. The overarching themes that cut across these interviews: The speed of payments is, of course, increasing. The scope of payments? It’s said that change is the only constant in life. That is broadening, too, and crossing borders.

For businesses, slow payments are more than a simple headache. When payments are not delivered on time, they can harm a company’s finances and can put a strain on business relationships. Given the stakes, it’s little wonder why real-time disbursements technology is gaining popularity in the B2B payments space.

The payments industry has been riding the wave of shifting consumer habits and demands, placing the end-user experience at the forefront of new products, services and infrastructure. Those users, both consumers and businesses, aren’t just demanding choice, however. But with the U.S. But with the U.S.

What is clear, however, is that Open Banking is gaining traction, largely driven by the competitive pressure for banks to enable their customers with the FinTech tools they demand. While Open Banking may seem like the obvious answer to the demand for data integration between banks and FinTech firms, the complexities of the U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content