This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Somalia Payment Switch (SPS1) has successfully launched the country’s first ever InstantPayment System with QR payments support powered by BPC’s next generation SmartVista platform, a global leader in payment solutions2. The demand for secure, fast, and modern payment solutions has been pressing.

The Somalia Payment Switch (SPS1) has successfully launched the country’s first ever InstantPayment System with QR payments support powered by BPC’s next generation SmartVista platform, a global leader in payment solutions2. The demand for secure, fast, and modern payment solutions has been pressing.

The Interledger Foundation , an organisation building and advocating for an open, interoperable payment network, is introducing a new initiative to fund fintechs that leverage its Interledger Protocol (ILP) to bring payment capabilities to emerging markets and underserved populations.

Through the new connection with Thunes’s Direct Global Network leveraging existing Swift connectivity, financial institutions can now send instantpayments directly to mobile wallets in over 130 countries and 80 currencies.

Jeff Parker, CEO, says, “Digital payments will continue to grow rapidly, with mobile wallets expected to reach 4.8 Key trends will include the acceleration of cross-border, real-time and instantpayments and the rise of cashless economies. billion users by 2025, nearly 60% of the global population.

How can we look to this rapidly growing business for new use cases for instantpayments? A robust information exchange framework with common standards and protocols is a step toward enabling e-invoices and e-remittances support for instantpayment messages in the United States.

Combatting fraud As the world becomes more interconnected and instantpayments gain prominence, the threat of fraud also rises. Push payment fraud, where funds are transferred to fraudulent accounts, is a significant concern. The immediacy of instantpayments demands precision and validation.

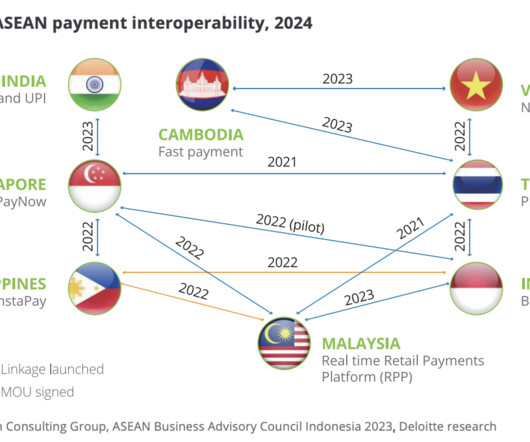

ASEAN payment interoperability, 2024, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Additionally, cross-continental interoperability programs were also introduced. Public-private collaborations also play a critical role in developing and promoting cross-border payments.

NPCI International Payments Limited (NIPL), the international arm of the National Payments Corporation of India (NPCI), has signed an agreement with the Bank of Namibia (BoN) to support them in developing an instantpayment system like Unified Payment Interface, UPI stack in Namibia. Mr. Johannes !Gawaxab,

It is common to receive instantpayments for ad hoc employment and other work-related reimbursements, but real-time Social Security and retirement payouts have yet to gain traction. Retirees are used to digital disbursement methods, but instantpayments have not become popular within the U.S.

Its fair to say that traditional financial systems left many people and communities underserved, but LPMsfrom mobile wallets in Africa to RTP schemes like UPI in Indiabridge this gap, and theyre empowering billions of consumers to participate in the digital economy.

Consider alternative credit scoring: in underbanked markets, open data allows lenders to assess creditworthiness using mobile payments, utility bills, and telecom data. For payments providers, this blurs the line between transaction services and credit enablement, with implications for product strategy and partnerships.

For example, in Mexico, despite having instantpayments, there’s still low banking usage. Kenya, however, skipped traditional banking and moved straight to mobile payments. “Unlike in established markets, the absence of existing systems and infrastructure allows the chance to start from scratch with payment technology.”

Financial institutions require 24/7 connectivity, real-time settlement and liquidity management, customer interfaces, and fraud mitigation tools to prepare their underlying systems for instantpayments. Attend this session to hear a discussion on financialinclusion, authentication, and consumer protections.

It also reduces costs through resource sharing, enhances system resilience, and supports economic inclusion by expanding access to financial services for underserved groups. Over these years, CBI has developed several open banking and open finance services and achieved a variety of goals at national and international level.

Leading digital banks also offer innovative features, including AI-driven financial planning, blockchain technology, and instantpayments. They provide a broad range of financial products, from competitive savings accounts to investment and loan services.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content