This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

PayMint , a leading financial technology company, has announced that it has obtained final approval from the Central Bank of Egypt to launch its first Meeza prepaid cards in partnership with Abu Dhabi Islamic Bank Egypt (ADIB-Egypt).

Egyptian fintech PayMint has received final approval from the Central Bank of Egypt to launch its first ‘Meeza’ prepaid cards in partnership with Abu Dhabi Islamic Bank (ADIB). PayMint plans for the new Meeza prepaid cards to enable its customers to carry out purchases, cash withdrawals, and online shopping in Egypt.

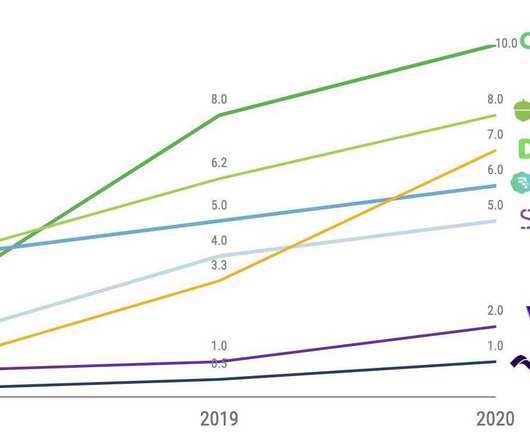

From digital payments to decentralised finance (DeFi), these companies are solving real-world challenges like financialinclusion and cross-border transactions, while setting new global standards for innovation. Coda aims to make digital transactions simple, inclusive, and accessible to everyone. Coda Valuation: $2.5

America Biometric Payments 2 Global, especially mobile-first markets Cash Payments 5 Emerging Markets, some developed regions Central Bank Digital Currencies (CBDCs) 1 Asia, Caribbean Credit Cards Overview : Credit cards allow consumers to make purchases on credit, paying later and often with interest.

MTN Mobile Money (U) Limited, in partnership with Mastercard , Diamond Trust Bank and Network International, has launched the Virtual Card by MoMo, an innovative payment solution designed to enable MTN MoMo subscribers to perform secure online transactions without needing a physical card or bank account.

GSMA and UK Finance have joined forces to provide a collaborative framework for the UK’s leading mobile network operators and banks to develop and launch Scam Signal, a new solution to help address Authorised Push Payment (APP) fraud in the UK. Data from UK Finance shows that £213.7

Armenia Population: +2,967,000 Capital, financial hub and largest city: Yerevan Gross domestic product (GDP) per capita: +$8,500 Access to a formal financial account (adults): 52.3 per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population.

Lloyds Banking Group is shutting down its mobile van banking service this year and closing 123 branches, sparking concern over reduced access to essential financial services, particularly in rural and underserved areas. is unhappy with Lloyds’ decision to stop its mobile van banking service.

The meteoric ascent of Brazilian neobank Nubank has sent shockwaves through the Latin American banking industry. As digital banks in the Asia Pacific (APAC) region aim to replicate this success, there are valuable lessons to be learned from the unconventional Nubank approach to banking.

In simple, layman’s terms, embedded finance is when financial services – like payments, loans, or insurance – are integrated directly into non-financial platforms. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

The Financial Barriers Facing SMEs in Emerging Markets SMEs face unique financial obstacles, particularly in emerging markets. Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Traditional banks typically require extensive documentation, credit history, and collateral, which many lack.

Senegal is one of many countries across the Middle East and Africa trying to diversify its economy and future-proof itself by hosting financialinclusion by employing fintech solutions. Mobile phone usage in Senegal has surpassed 60 per cent this year.

Growth is driven by financialinclusion, fintech innovation, and regulatory reforms. However, mobile payments, digital wallets, and real-time transactions are broadening financial access. How does the rise of real-time payments impact traditional banking in Latin America? trillion by 2027. Management Summary 3.

Cambodia is leveraging fintech innovations and strategic reforms to boost economic growth, financialinclusion and international partnerships, positioning itself as a key player in the Southeast Asian digital economy. per cent this year and six per cent next year, according to the Asian Development Bank. million in 2021 to 19.5

This incident disrupted operations across airlines, banks, and media outlets, resulting in billions in losses for major corporations. The Bank of England has emphasised the need for payment firms to enhance their operational resilience, mandating improvements by March 2025 to better handle disruptions like cyber-attacks or system failures.

Having looked at everything in the banking-as-a-service (BaaS) space and online marketplaces, our final focus in April is on embedded finance in e-commerce and the checkout experience. We hear from industry experts on how embedded finance ensures the checkout experience is financiallyinclusive.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? CEO Linda Yaccarino framed the move as a leap forward, but the real story is bigger: tech giants are no longer just facilitating payments, theyre actively reshaping the financial industry.

Decentralisation, through DeFi and CBDCs, is driving financial innovation, addressing challenges like financial crime and cybersecurity, and meeting growing demand for secure, efficient solutions. The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services.

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

Hibret Bank , in collaboration with Mastercard , has announced the launch of the Prepaid Hibir Mastercard services, marking a significant milestone in the journey towards financial digitization in Ethiopia.

Cooperative Bank of Oromia and Mastercard have unveiled a groundbreaking collaboration with the launch of the Coopbank Prepaid Mastercard and the introduction of the Community Pass technology in Ethiopia. Transactions will be effortless through a dedicated mobile application, providing efficient card management capabilities.

of India (NPCI) that facilitates inter-bank transactions, has propelled the growth of online payments, the Financial Times (FT) reported. UPI was established by the central bank and is owned by a group of local lenders. Its proponents insist UPI has revolutionized financialinclusion in the county of 1.4

NOW Money , one of the leading inclusive digital payroll and banking platform for migrant workers, today announced its new strategic partnership with Mastercard , a global technology company in the payments industry. Customers can handle payments, transfers, and other financial operations directly from their mobile phones.

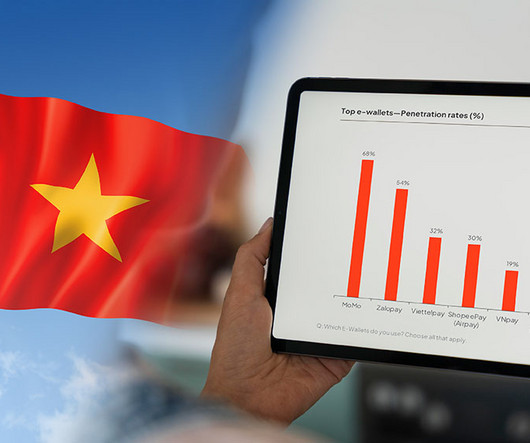

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

billion) in 2022, according to Thant Mam Hein, assistant manager of sustainability at uab bank. Reports also show that approximately 50% of Myanmar’s adult population had a bank account in 2020, reflecting growth in financialinclusion and creating new opportunities for businesses and individuals. trillion (US$3.8

PYMNTS’ November 2020 Disbursements Tracker® , done in collaboration with Ingo Money , states that “FIs that support digital and mobile payment tools could help these consumers access financial solutions without using traditional accounts, but many FIs must address age-old challenges before they can roll out such tools.”

Sherrod Brown (D-Ohio) asked, “Why on earth would we trust big tech with our banking system?”. After all, it takes days to settle retail bank transfers. dollar would offer a seamless way to integrate with existing banking and payment functions, distributing funds to digital wallets. But Giancarlo said a digital U.S.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. First name. Company Name. Phone number. Source: PwC.

SecurityTech company Giesecke+Devrient (G+D) is making digital payments independent of online connectivity. The token-based payment solution G+D Filia® Unplugged enables consecutive, secure offline payment transactions anytime and anywhere, bridging the gap between seamless online and offline payments without a reliable internet connection.

In Pakistan, and elsewhere, the stars are aligning for greater use of digital banking and payments to improve financialinclusion. A widespread embrace of mobile devices, said Wain, “made it possible for new players in that ecosystem to build and deliver services on top of the mobile telecom infrastructure.

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

Orange Middle East and Africa (OMEA) ( www.Orange.com ) and Mastercard have announced a strategic partnership to expand access to mobilefinancial services across Sub-Saharan Africa. Orange Money customers will be able to instantly obtain a virtual or physical debit card, linked directly to their Orange Money wallets.

This article delves into how fintech is reshaping financial services in these regions. We will explore success stories, the pivotal role of mobile money , and the unique challenges faced. The Role of Mobile Money Mobile money is a cornerstone of fintech in emerging markets.

Not so many years ago, Filipinos had to visit bank branches or ATMs to transfer money and manage their accounts. A complex set of geographic and institutional barriers, including the fragmentation of Filipinos across over 7,000 islands, and low levels of financial literacy, are also hampering the use of financial services.

In the great digital shift , the mobile device is the point of sale — especially in Asia’s fast-growing markets. The conversation came against a backdrop where online transaction volumes and mobile wallet adoption are increasing. Donlea noted that mobile wallets are designed for consumer and brand loyalty.

The customer-merchant Payment Service Provider (PSP) takes charge of the approval process through National Payments Corporation of India (NPCI), swiftly debiting the money from the issuer bank and crediting it to the merchant’s acquiring bank in under 60 seconds. Fortunately, there’s a light at the end of this tunnel!

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

In the landscape of commerce, mobile payments have emerged as a disruptive force, altering the way people engage in financial transactions. As technology advances and consumer preferences evolve, the trajectory of mobile payments promises unparalleled convenience, robust security, and seamless integration into our daily lives.

PalmPay ( www.PalmPay.com ), a leading digital bank and fintech platform focused on emerging markets, has launched the PalmPay Debit Card in Nigeria in partnership with Verve, Africa’s largest domestic card scheme. “ said Sofia Zab, Chief Marketing Officer at PalmPay. With over 35 million users and a growing network of 1.1

Drawing on comprehensive data from the 14 largest banking groups in Great Britain and Northern Ireland, the insights provide an in-depth examination of the tactics fraudsters use, the platforms they exploit, and the devastating impact these scams have on victims. Whilst scam values decreased overall, rates and losses remain substantial.

Drawing on comprehensive data from the 14 largest banking groups in Great Britain and Northern Ireland, the insights provide an in-depth examination of the tactics fraudsters use, the platforms they exploit, and the devastating impact these scams have on victims.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financialinclusion and helping people develop healthy financial habits.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content