This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Financial Barriers Facing SMEs in Emerging Markets SMEs face unique financial obstacles, particularly in emerging markets. Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Traditional banks typically require extensive documentation, credit history, and collateral, which many lack.

In simple, layman’s terms, embedded finance is when financial services – like payments, loans, or insurance – are integrated directly into non-financial platforms. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

Senegal is one of many countries across the Middle East and Africa trying to diversify its economy and future-proof itself by hosting financialinclusion by employing fintech solutions. Mobile phone usage in Senegal has surpassed 60 per cent this year.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

Lloyds Banking Group is shutting down its mobile van banking service this year and closing 123 branches, sparking concern over reduced access to essential financial services, particularly in rural and underserved areas. is unhappy with Lloyds’ decision to stop its mobile van banking service.

NOW Money , one of the leading inclusive digital payroll and banking platform for migrant workers, today announced its new strategic partnership with Mastercard , a global technology company in the payments industry. Customers can handle payments, transfers, and other financial operations directly from their mobile phones.

Kueski , the buy now, pay later (BNPL) and online consumer lender in Latin America, has launched an in-store version of Kueski Pay, which will become available to all consumers by the end of Q2 of 2024, to offer them the ability to complete transactions through the Kueski mobile app, regardless of internet connection, in physical stores.

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

Cambodia is leveraging fintech innovations and strategic reforms to boost economic growth, financialinclusion and international partnerships, positioning itself as a key player in the Southeast Asian digital economy. per cent this year and six per cent next year, according to the Asian Development Bank. million in 2021 to 19.5

Cooperative Bank of Oromia and Mastercard have unveiled a groundbreaking collaboration with the launch of the Coopbank Prepaid Mastercard and the introduction of the Community Pass technology in Ethiopia. Transactions will be effortless through a dedicated mobile application, providing efficient card management capabilities.

Orange Middle East and Africa (OMEA) ( www.Orange.com ) and Mastercard have announced a strategic partnership to expand access to mobilefinancial services across Sub-Saharan Africa. Orange Money customers will be able to instantly obtain a virtual or physical debit card, linked directly to their Orange Money wallets.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financialinclusion and helping people develop healthy financial habits.

This article delves into how fintech is reshaping financial services in these regions. We will explore success stories, the pivotal role of mobile money , and the unique challenges faced. The Role of Mobile Money Mobile money is a cornerstone of fintech in emerging markets.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. First name. Company Name. Phone number. Source: PwC.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

Although lower costs and increased availability of new peer-to-peer (P2P) payment systems have allowed more first-time users to enjoy the ease and benefits of the banking system, the fact remains that 1.7 The fact that more telecom companies are now offering basic mobile payment services is also helping to bridge the unbanked gap.

Orange Middle East and Africa is strategically partnering with global payments giant Mastercard to expand access to mobilefinancial services across Sub-Saharan Africa. Only 48 per cent of the African adult population is banked, according to the African Digital Banking Transformation Report.

“SteelWave Digital can further bridge the financial accessibility gap by expanding its strategic partnerships with global liquidity providers to enhance capital flows into underserved markets. ” The post What More Could Your Fintech be Doing to Bridge the Financial Accessibility Gap?

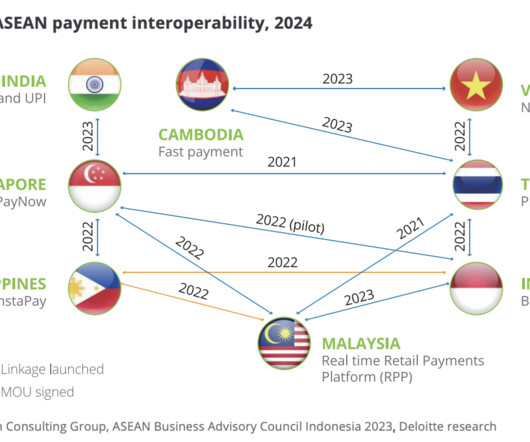

Asia Pacific point-of-sale payment methods – Select markets, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Payment interoperability The growth of digital payment innovations in APAC has emphasized the need for connectivity and interoperability in both online and offline transactions.

This revolutionary service provides over 5 million Lebanese citizens with the ability to manage their payments securely and transparently for local and international purchases without needing a bank account. Through Wink Pay, we can simplify and digitize customer onboarding, as well as facilitate online payments.

EAZY Financial Services ‘EazyPay’, a Bahraini financial institution specialising in point-of-sale (POS) and online payment gateway acquiring services, has teamed up with Tarabut , the MENA region’s regulated open banking platform. Most recently, he served as chief operating officer at Bankable.

When recognizing Cybersecurity Month in October, it is important to consider the connection between cybersecurity, cutting-edge technology, and financialinclusion. Executives of financial institutions should have a good understanding of the importance of financialinclusion and the impact technology has on it is essential.

The Definition of Fintech vs Traditional Finance Fintech refers to financial technology, which encompasses a broad range of tech innovations and advancements applied to financial services. Overall, fintech aims to improve and automate the delivery and use of financial services, often focusing on innovation, usabilty, and efficiency.

These awards highlight companies and individuals whose fintech initiatives have contributed to advancing financial technology, promoting financialinclusion, and improving service delivery. Integrated with bank accounts and digital wallets in Pakistan, Hakeem provides customers with easy disbursement options.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

12) the national launch of a mobile payments bank, which, according to a report , is India’s first one. According to the report, Airtel is taking advantage of a big push by the Indian government to accelerate financialinclusion and bring more competition to the market by issuing payment bank licenses.

Embedded finance refers to the integration of financial services directly into non-financial platforms, eliminating traditional barriers to transactions and enhancing user convenience. Beyond offering convenience, super apps also play a crucial role in addressing financialinclusion challenges.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. million to support SMEs in Chile.

In 2022, the country was home to 993 active fintech companies, representing about 25% of all fintech ventures operating across the ASEAN region, data from a 2022 report by the United Overseas Bank (UOB), PwC Singapore and the Singapore Fintech Association (SFA) reveal. billion to US$15 billion during the period. in July 2023.

Nicky Senyard, CEO and founder of Fintel Connect “Developing countries are actually great places for new ideas because they often don’t have traditional banks. This shift has led to a bunch of great advancements in mobilebanking and money apps, making it possible for financial services to reach even the most remote areas.

As of April 2023, there were 1,000 active fintechs in Latin America (LatAm) with a vast majority focusing on financialinclusion, tackling the issue of 70 per cent of the population not having access to formal financial services. Can you tell me more about the company and your role within it? million users in 2019 to 29.3

These “credit invisibles” don’t have credit cards, bank accounts or credit history — so how can a lender assess their risk? The EFL score uses psychometrics and behavioral data to measure a person’s credit risk based on an applicant’s answers to a series of interactive questions and exercises administered via an online assessment.

Speakers: Marisa Parella, Federal Reserve; Mark Ranta, Alacriti; Sherri Reagin, North Salem State Bank; Elspeth Bloodgood, Jack Henry & Associates 1:40pm-2:20pmCT: Panel Session – Fin+Tech = Unlocking Limitless Potential (Louisiana Ballroom) Fintech solutions are not a one-size-fits-all approach.

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digital bank licenses to eligible applicants. Oversea-Chinese Banking Corp. and United Overseas Bank Ltd. billion ($1.1 Grab + Singtel .

Bank of America launched the BankAmericard in 1958, widely considered the first credit card available to consumers, which eventually evolved into Visa. In 1966, a group of California banks formed the Interbank Card Association (ICA), later known as Master Charge and then Mastercard.

It may not be the year of mobile payments — yet — but it is certainly the year mobile payments players are laying the groundwork for what they know is inevitable. This week, PYMNTS dug into the week of mobile pay news to bring you the latest from the ecosystem. Early Warning Boosts Big Banks’ P2P Power.

Prior to Airwallex, Liu worked as an investment consultant for banking firm China International Capital Corporation (CICC) in Shanghai. The startup targets underserved markets in the insurance space, such as the poor, students and startups. At Airwallex, Liu is responsible for the company’s branding and operations.

To improve the financial lives of millions of Americans, speed matters — especially for FinTechs seeking to bring new products to market digitally and to target consumers underserved by traditional banking models. As Choubey told Webster, the FinTech traces its roots to providing financial access to 90 million Americans.

Digital and mobile payments have become the predominant payment methods, leading many to believe that cash is on the verge of extinction. The integration of digital payment options, such as mobile, contactless and online payments, has become a cornerstone of modern commerce.

Jeremy Baber, CEO of Lanistar “Established markets are dominated by traditional banking meaning the opportunities for newer fintechs to deliver significant change are much more restricted. . “Brazil, for example, has been the site of the development and roll-out of bank transfer methods such as PIX and QR-code-driven payments.

Akulaku – US$2 billion Indonesia’s most valuable fintech startup is Akulaku, an onlinebanking and digital finance platform valued at US$2 billion. Founded in 2016, Akulaku provides digital banking, financing, investment and insurance brokerage services, targeting financialunderserved demographics.

Over the years, weve covered a broad range of fintech topics from digital banking to decentralised finance , regtech , green fintech , and more. Fintech, or financial technology, is the integration of technology into financial services. This shift affects banks, insurers, asset managers, and regulators alike.

With online fraud’s rapid growth into a shady multibillion-dollar annual business, preventing it is becoming increasingly critical for all merchants and consumers. The issue of identity verification fringes upon a host of other related issues such as cyberthreats, identity fraud, and financialinclusion.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content