This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Selling products and services internationally means facing new challenges, especially regarding payment processing, regulatory requirements, currency exchanges, and fraudprevention. For instance, while credit cards are popular in North America, regions like Europe favor bank transfers, and digital wallets are dominant in Asia.

The Protect suite is among nearly 200 products under Visa’s portfolio, covering critical areas such as Acceptance, Advisory, Issuing, Open Banking, and Risk and Identity. Featured image credit: Edited from Freepik The post Visa Set to Roll out New AI-Powered FraudPrevention Solutions appeared first on Fintech Singapore.

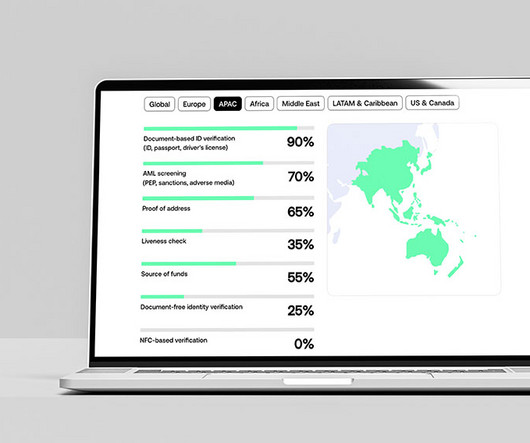

According to a new report by Sumsub, crypto fraud rates declined by a remarkable 23% between 2023 and 2024, positioning APAC as a leader in combating crypto fraud. The rise of document-free verification The Sumsub report also highlights the rise of document-free (non-doc) identity verification. in 2023 to 2% in 2024.

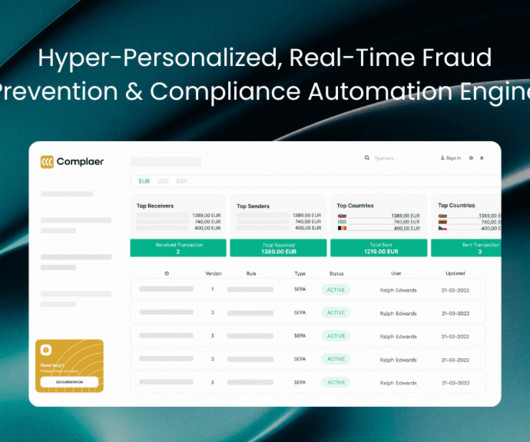

Fraud evolves daily, yet legacy systems take months to adaptleaving businesses exposed. Complaers no-code fraudprevention engine puts compliance teams back in control, delivering real-time, hyper-personalised AML/CTF strategies without engineering support. Complaer is changing that.

As small and medium-size businesses are increasingly turning to non-banking cost-efficient payments solutions, Guavapay is at the forefront of providing solutions that meet the evolving needs of global businesses with real-time, affordable fund transfer, multi-currency accounts and advanced payment APIs.

The Economic Crime and Corporate Transparency Act 2023, specifically the “failure-to-preventfraud” offence, and outlines how businesses can mitigate fraud risks. Firms must be required to have fraudprevention policies in place and demonstrate their effectiveness. Why is it important?

iDenfy , the global fraudprevention identity verification service provider, has filed a patent for technology that verifies a user’s address data. Fraudsters, using forged or altered information, have long been exploiting traditional address verification methods, such as utility bills or other proof of address documents.In

Interchange and assessment fees are set by card networks and are non-negotiable. Acquiring bank – The merchants bank that receives and disburses the funds. They facilitate transactions by connecting merchants, credit card processors, and banks while establishing rules, regulations, and fees for processing payments.

Moniepoint is building an all-in-one, seamlessly integrated platform for African businesses that features services including digital payments, banking, foreign exchange, credit, and business management tools. Wise became the first non-bank operating in Japan to earn approval to join the country’s domestic payment network, Zegin.

Visa has introduced three new AI-powered risk and fraudprevention solutions to enhance security in digital payments. The new products, integrated into the end-to-end Visa Protect suite, aim to diminish fraud across immediate account-to-account and card not present (CNP) payments, as well as transactions both on and off Visa’s network.

Meanwhile, the fraud landscape is rapidly changing. Over a third of fraud attempts (42.5 per cent) targeting financial institutions now use AI, according to a recent study by digital identity and fraudprevention solution Signicat. Overall, around 29 per cent of these AI-driven fraud efforts are successful.

As technologies like cloud computing and artificial intelligence (AI) become more accessible, banks in 2025 will face a new challenge. ’ One company that is well-placed in this banking evolution is Temenos , the core banking solutions provider. How will banks utilise AI in 2025? The result? The impact?

Its the bridge between an eCommerce website, its customers, and the bank. Its the third-party service that serves as the link between the payment gateway, acquiring bank, and issuing bank or card network. It works in tandem with the customers bank or credit card provider to verify and authorize the transaction.

From open banking to open finance and beyond: The future of financial data-sharing March 18 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The evolution of open banking into open finance, examining regional regulatory approaches and adoption trends. Why is it important?

Ensure the gateway offers PCI DSS compliance, encryption, tokenization, and fraudprevention tools to safeguard transactions. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer. Learn More What is a Payment Gateway? This is known as the settlement time.

Behind every seamless payment card transaction is a complex network of banks, credit card companies, and payment systems working together to transfer money from the customer to the merchant. Although they go to issuing banks, the rates are set by card networks. However, this convenience comes at a cost, mainly for businesses.

” As small and medium-sized businesses increasingly turn to non-banking cost-efficient payment solutions, Guavapay aims to provide solutions that meet the evolving needs of global businesses with real-time, affordable fund transfer, multi-currency accounts and advanced payment APIs.

Payment technology and innovation are accelerating across the fintech industry, with more companies recognising the importance of adapting to changing customer needs, with non-cash transactions projected to hit 2.3 Reserve banks mandating reduced cash use will enhance security and economic participation. trillion transactions by 2027.

Latvia-based BluOr Bank has selected Nets , part of the European paytech, Nexi Group , to leverage its payment card issuing services, offering an enhanced customer banking experience tobusiness and entrepreneurs in the Baltic region. This collaboration aims to enhance how businesses manage their expenses.

And yet, accepting non-cash forms of payments is more or less required to operate a modern business, at least in the U.S. They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. Acquiring Bank: The business’ (i.e., merchant’s) bank.

This challenge is particularly acute in industries like payments, where trust, security, and compliance are non-negotiable. Non-compliance can expose businesses to fines, reputational damage, and loss of consumer trust. Why compliance and fraudprevention are essential in the payment industry The payments industry is built on trust.

APIs have played a central role in the digital evolution of banking. Initially, APIs were point-to-point connectors to enable simple integrations; with rapid innovations, they have now matured into a foundational layer supporting a wide range of use casesfrom customer onboarding and loan origination to card issuance and fraud detection.

Merchant Information, a solution within Tink’s Consumer Engagement offering, means banking app transactions are shown with a clear brand name, logo, location, and merchant contact details – reducing the need for consumers to contact their bank to enquire about transactions they don’t recognise.

A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%. The company facilitates the transfer of information and funds between the customer’s bank and your business’ bank.

Government mandates that penalize non-compliance with fraudprevention measures and require victim reimbursement underscore the urgency for financial institutions to strengthen their defense and ensure compliance. APP scam losses in Brazil hit almost $380 million in 2023 and are projected to increase by almost 40% by 2028.

It highlights key trends, such as open banking, tokenisation, and fraudprevention, which are crucial for merchants to remain competitive and secure. As the payments ecosystem continues to evolve with innovations like open banking, instant payments, and tokenisation, merchants are facing a host of challenges and opportunities.

With over 30 years of banking and payments experience, Elliff has a strong track record of innovating and building intrapreneurial ventures and high-growth businesses while at NatWest Group and JP Morgan Chase. This is especially true for dispute resolution and fraudprevention.

OpenWay , a provider of digital payments technology to banks, processors, national payment switches, and mobile wallet operators, found that clients are recognising the benefits of AI. Gen AI can identify which government agencies or non-profits may be interested in this functionality and generate targeted proposals.

Stripe Radar combines data from the hundreds of thousands of businesses processing transactions on the Stripe network with intelligence from banks and credit card networks to provide users with the ability to customize the fraud defenses for their individual business.

The issuing bank verifies whether the customer has enough funds in their account to complete the transaction. Once approved, the information is sent to the merchants bank account, where the funds are deposited. If necessary, you need to apply for a merchant account through a bank or payment processor.

Those apps, she said, should provide security and fraudprevention, transaction insights, “seamless DIY” and customized engagement. Consumers expect to service their accounts with activities like profile setups, making payments and helping manage their accounts with dispute resolution and fraud alerts,” she said.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. And then trust.

For banking professionals, it’s important to recognize the severe impact of high chargeback levels on merchants, a challenge that continues to escalate. These figures define the maximum number of chargebacks a merchant can incur within a month before being classified as “non-compliant.” Why Do Chargeback Thresholds Exist?

And when that happens, non-compliance can lead to many degrees of harm to any and all business owners. It gets worse: merchants that use a non-PCI certified provider can face class action lawsuits, fines of up to $10,000 per month, and $500,000 per incident. Fraudprevention For both customers and merchants, fraud is a common concern.

Bronwyn brings over two decades of experience across technology, cybersecurity, regulatory compliance and fraudprevention. Most recently, Bronwyn served as CISO at fintech Mambu and led security transformation and AI enablement initiatives for TSB Bank.

The original sensitive data is still secured and hidden in an external data bank. Payment verification by the issuing bank means the customers bank will check whether the customer has sufficient funds to complete the transaction.

Debit or credit card chargebacks are when a disputed charge made to a merchant’s account is refunded to the customer’s bank account. This has been aided by the rise of online banking, which has made the chargeback process as easy as a few clicks. What Are Credit Card Chargebacks?

Today, Visa (NYSE:V), a leader in digital payments, announced continued expansion of its global value-added services business with the addition of three new AI-powered risk and fraudprevention solutions. Security and fraudprevention are fundamental to Visa.

There seems to be no shortage of action in the corporate banking space, whether it be scandals (like Royal Bank of Scotland’s Global Restructuring Group fiasco ), cyberattacks (such as the $81 million stolen from the central bank of Bangladesh) or anomalies like Brexit impacting top financial institutions across the globe.

Determining interchange fees: Interchange fees are costs paid between banks for accepting card-based transactions. MCCs enable businesses and regulatory bodies to maintain accurate financial records, streamline tax reporting, and reduce the risk of non-compliance. MCCs play a role in setting these fees.

In May, Fintech Global released its inaugural FinCrimeTech50 list, recognizing the world’s leading technology companies fighting money laundering, fraud and financial crime. The list features the 50 most innovative tech companies offering solutions in financial crime and fraudprevention in the world. Transparently.AI

These companies, which represent countries such as Malaysia, the Philippines and South Korea, are tackling challenges in sectors such as lending, banking, and business finance, leveraging innovative business models and cutting-edge technologies to boost efficiency and enhance accessibility across the financial services industry.

31) said the companies have released their joint analysis on the issue to find that more than a third (38 percent) of banks and payments organizations admit it is becoming increasingly difficult to differentiate between a fraudulent and genuine transaction. Reports Tuesday (Jan.

and ACH/eChecks for direct bank transfers. Fraudprevention tools: Helps detect and prevent fraudulent transactions. Additional security like 3D Secure , off-site data storage, and customizable fraud modules will also be valuable tools to protect customer payments. Digital wallets (Apple Pay, PayPal, etc.)

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content