This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In many regions, they create jobs, drive innovation, and stimulate local economies. From innovative lending platforms to advanced payment processing, fintech is enabling them to access growth opportunities and thrive in today’s competitive markets. Fintech companies see this gap as an opportunity to innovate.

Think about how easy it is to order a ride on Grab, book a hotel on Agoda, or pay for groceries on Shopee without even needing to pull out your credit card or open a banking app. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population. What’s Next?

Kueski , the buy now, pay later (BNPL) and online consumer lender in Latin America, has launched an in-store version of Kueski Pay, which will become available to all consumers by the end of Q2 of 2024, to offer them the ability to complete transactions through the Kueski mobile app, regardless of internet connection, in physical stores.

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

Over the years, weve covered a broad range of fintech topics from digital banking to decentralised finance , regtech , green fintech , and more. This includes services like mobilebanking, peer-to-peer payments, investment platforms, and blockchain applications. Consumer trust in banks plummeted.

This year’s awards are also supported by 12 fintech community members, including Ripple, NETS, ADVANCE.AI, and HSBC, as part of the ‘Fintech Gives Back’ initiative, aimed at encouraging innovation and supporting emerging talent. Ripple, NETS, Syfe, and YouTrip returned as sponsors this year. ThitsaWorks Pte.

These markets, often characterised by underdeveloped financial infrastructure , benefit significantly from fintech innovations. We will explore success stories, the pivotal role of mobile money , and the unique challenges faced. The Role of Mobile Money Mobile money is a cornerstone of fintech in emerging markets.

NOW Money , one of the leading inclusive digital payroll and banking platform for migrant workers, today announced its new strategic partnership with Mastercard , a global technology company in the payments industry. Customers can handle payments, transfers, and other financial operations directly from their mobile phones.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financial inclusion and helping people develop healthy financial habits.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

Orange Middle East and Africa (OMEA) ( www.Orange.com ) and Mastercard have announced a strategic partnership to expand access to mobile financial services across Sub-Saharan Africa. The partnership will be rolled out in seven countries including Cameroon, Central African Republic, Guinea-Bissau, Liberia, Mali, Senegal and Sierra Leone.

EAZY Financial Services ‘EazyPay’, a Bahraini financial institution specialising in point-of-sale (POS) and online payment gateway acquiring services, has teamed up with Tarabut , the MENA region’s regulated open banking platform. Conister Bank Limited has launched an online deposit system for its UK retail customers.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

Cooperative Bank of Oromia and Mastercard have unveiled a groundbreaking collaboration with the launch of the Coopbank Prepaid Mastercard and the introduction of the Community Pass technology in Ethiopia. Transactions will be effortless through a dedicated mobile application, providing efficient card management capabilities.

The report, Advancing Economic Inclusion—Empowering Underserved Communities with Fintech , highlights the innovative products and services revolutionizing the way commerce is conducted through safe, secure, convenient, and rewarding solutions.

This revolutionary service provides over 5 million Lebanese citizens with the ability to manage their payments securely and transparently for local and international purchases without needing a bank account. Through Wink Pay, we can simplify and digitize customer onboarding, as well as facilitate online payments.

What happens when an ongoing revolution in payment innovation meets a regulatory regime determined to ensure secure and safe transactions for individual consumers, business entities, and even governments? Here is our look at fintech innovation around the world. This is the payments landscape in the UK and EU in 2025.

Orange Middle East and Africa is strategically partnering with global payments giant Mastercard to expand access to mobile financial services across Sub-Saharan Africa. Only 48 per cent of the African adult population is banked, according to the African Digital Banking Transformation Report.

Their growing popularity has spurred continuous financial innovation, such as the rise of buy now, pay later (BNPL). Project Nexus , for example, is led by the Bank for International Settlements (BIS) and aims to create a blueprint for connecting national instant payment systems to enable seamless cross-border payments.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

Over the past decade, Singapore has emerged as a global powerhouse in fintech innovation, not just in Southeast Asia but across the broader Asian region. Whether its purchasing travel insurance during flight bookings or accessing micro-loans while shopping online, embedded finance simplifies financial interactions.

12) the national launch of a mobile payments bank, which, according to a report , is India’s first one. According to the report, Airtel is taking advantage of a big push by the Indian government to accelerate financial inclusion and bring more competition to the market by issuing payment bank licenses.

Consumers in the Philippines are demanding so much from online technologies, that research from Digido , the Filipino online lender, has found the digital lending market could reach $1billion in the second half of 2025. Digido revealed that in terms of market structure, non-bank digital lenders are expected to make up 55.2

. “SteelWave Digital can further bridge the financial accessibility gap by expanding its strategic partnerships with global liquidity providers to enhance capital flows into underserved markets. “Fintechs working to bridge this gap should focus on developing a superior user experience within the online platform and mobile channel.

With a rapidly growing economy and a tech-savvy population, Indonesia has become a hotbed for fintech innovation and startups, peering into the most well-funded fintech startups in ASEAN’s largest country can provide hints on what verticals investors are most bullish on in this region. billion to US$15 billion during the period.

This article aims to explore the impact that Visa and Mastercard has on the payment industry, examining their influence on innovation, regulation, consumer behavior, and the broader economy. Bank of America launched the BankAmericard in 1958, widely considered the first credit card available to consumers, which eventually evolved into Visa.

challenger bank Coconut, which launched only weeks ago to provide banking services for freelancers, has landed a new partner. 7) said PrePay Solutions (PPS) is working with the company to provide Coconut its banking infrastructure and prepaid card technology. Reports Wednesday (Feb.

However, recent stringent regulations imposed by the Reserve Bank of India (RBI) have significantly impacted the sector, leading many fintech companies to reassess their BNPL strategies. Similarly, Slice, originally a BNPL firm, has transitioned to offering prepaid credit cards and is now merging with North East Small Finance Bank.

Prior to Airwallex, Liu worked as an investment consultant for banking firm China International Capital Corporation (CICC) in Shanghai. The startup targets underserved markets in the insurance space, such as the poor, students and startups. At Airwallex, Liu is responsible for the company’s branding and operations.

At a high level, SoftPOS – short for software point of sale – lets merchants take contactless payments across their own mobile devices and tablets. And retailers across any range of settings are finding value in offering buy online, pickup in store ( BOPIS ) offerings.

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digital bank licenses to eligible applicants. Oversea-Chinese Banking Corp. and United Overseas Bank Ltd. billion ($1.1 Grab + Singtel .

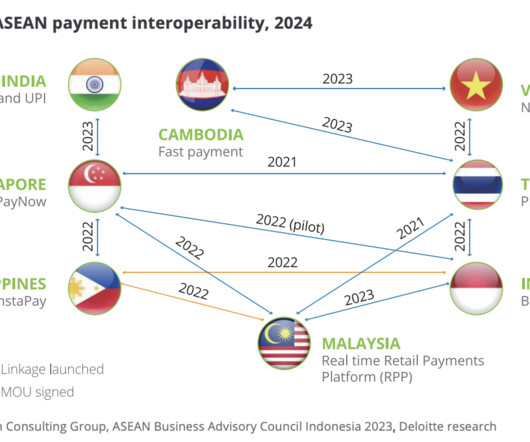

Cambodia is leveraging fintech innovations and strategic reforms to boost economic growth, financial inclusion and international partnerships, positioning itself as a key player in the Southeast Asian digital economy. per cent this year and six per cent next year, according to the Asian Development Bank. million in 2021 to 19.5

It may not be the year of mobile payments — yet — but it is certainly the year mobile payments players are laying the groundwork for what they know is inevitable. This week, PYMNTS dug into the week of mobile pay news to bring you the latest from the ecosystem. Early Warning Boosts Big Banks’ P2P Power.

These “credit invisibles” don’t have credit cards, bank accounts or credit history — so how can a lender assess their risk? The EFL score uses psychometrics and behavioral data to measure a person’s credit risk based on an applicant’s answers to a series of interactive questions and exercises administered via an online assessment.

Understanding Financial Inclusion Financial inclusion is the idea of making sure everybody has access to and uses financial services, mainly those who are not currently using banking services such as deposits, loans, and insurance. Technology has also bridged the gap between the banked and the unbanked by providing digital payment solutions.

And, of course, its relationship with the card networks and issuers was…complicated at best, Dan Schulman told Karen Webster during their fireside chat at Innovation Project 2017. Moreover, Schulman noted, One Touch has so far made a lot of headway against the sort of blessing/curse nature of mobile for merchants. Because it has to.

Federico Balige, LatAm CEO of PayU GPO PayU GPO stands at the forefront of online payment services across more than 50 high-growth markets, including Latin America, Africa, and Eastern Europe. In the fast-paced e-commerce landscape of Latin America, PayU GPO has emerged as a vital partner for businesses aiming to succeed online.

Some banks may not be able to connect to both. The panel will explore some of these initiatives including the New York Fed's CBDC pilot program with major banks, the recently concluded Boston Fed's Project Hamilton and other global CBDC projects. 100B/yr US alone – sticky, underserved, corporate/gov't load (no consumer).

Nicky Senyard, CEO and founder of Fintel Connect “Developing countries are actually great places for new ideas because they often don’t have traditional banks. This shift has led to a bunch of great advancements in mobilebanking and money apps, making it possible for financial services to reach even the most remote areas.

Small business banking provider BlueVine announced Tuesday (Nov. The funding will be used to further build and scale BlueVine’s banking platform, which boasts a business checking account that integrates with BlueVine’s existing suite of online financing products. 19) it has raised $102.5

SMEs aren’t getting the banking services that fit their needs now that they’re demanding online and mobile solutions, however. “Banks have a window right now to take advantage of that.” “Banks have a window right now to take advantage of that.”

The terms ethical finance and ethical banking often go hand in hand with climate awareness and focusing on net zero. Platforms like Kiva facilitate microloans to entrepreneurs in developing countries, often those who lack access to traditional banking services. However, they are not restricted to the climate.

To improve the financial lives of millions of Americans, speed matters — especially for FinTechs seeking to bring new products to market digitally and to target consumers underserved by traditional banking models. As Choubey told Webster, the FinTech traces its roots to providing financial access to 90 million Americans.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content