This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Card issuers need for speed exists on several levels, and we at OpenWay see this firsthand, since our Way4 card management software is used by top banks, processors and fintechs around the world. This can be an account opened in Way4 or in the integrated Core Banking System. Indeed, rapid product development remains a top priority.

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

For online shopping, Visa passkeys replace passwords or one-time codes. Click to Pay – Enables consumers to complete online transactions within a few clicks, powering a more seamless and secure checkout experience at scale. to broaden its merchant coverage network across Japan.

TRANSFOND , the Romanian Banking Association , and the entire banking community in Romania announce that the new RoPay system has become operational. RoPay allows users to make instant mobile payments in line with the national payment scheme. The first available use is for proximity-based person-to-person (P2P) payments.

The widespread shift to online reliance has created a greater demand for accessing various services online, including government public services and online retail payments. This increased digital dependency has raised the need for secure access and quick and easy identity verification online.

Payments providers will need to prioritise interoperability and compliance to unlock growth while addressing security and volatility concerns. The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services.

PYMNTS’ November 2020 Disbursements Tracker® , done in collaboration with Ingo Money , states that “FIs that support digital and mobile payment tools could help these consumers access financial solutions without using traditional accounts, but many FIs must address age-old challenges before they can roll out such tools.” In a word, “legacy.”

Tap to Everything There are six billion mobile devices in the world providing consumers with a versatile NFC enabled device primed to be ‘tapped’ At the end of 2023, Visa’s tap-to-pay penetration reached 65 per cent globally, up two times the penetration we saw in 2019, cementing tap as one of the best commerce experiences today.

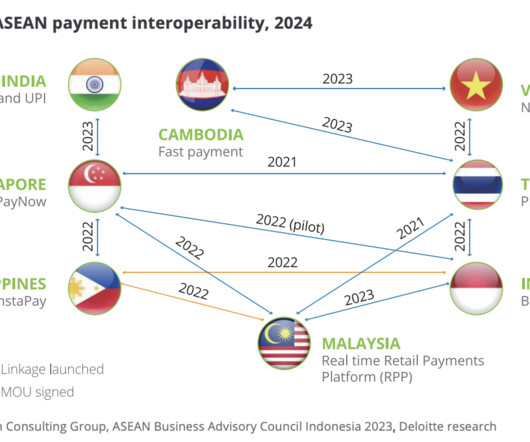

Asia Pacific point-of-sale payment methods – Select markets, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Payment interoperability The growth of digital payment innovations in APAC has emphasized the need for connectivity and interoperability in both online and offline transactions.

Completing online payments via manual card entry can be time-consuming and off-putting for customers. Click to Pay completely removes the need to enter credit card information during online purchases, making it more convenient and faster than manual card entry. Learn More What is Click to Pay?

It has pulled ahead of its EU neighbors in developing real-time payments technology and in recruiting banks to adopt it. And as Rita Camporeale , Head of Payments Systems at the Italian Banking Association ( ABI ), told PYMNTS’ Karen Webster, the pandemic has accelerated the embrace of instant payments that flow directly between banks.

Before that, we were talking about Ireland’s Central Bank and its search for top fintech talent, new investment in mobile payments in the Philippines , and the pace of digital transformation in India’s financial services sector. You joined TBC a few years after the bank expanded to Uzbekistan. Why Uzbekistan?

Ralf Germer, CEO and co-founder, PagBrasil Pix has been a giant windfall for Brazil and is now responsible for 90 per cent of bank transactions in Brazil. Through this collaboration, Bancard will offer this service to banks in Paraguay, enhancing convenience and financial accessibility for Paraguayan travellers.

QR codes had made some inroads here and there, and yet did not become the go-to repositories of data and information – scannable, naturally, across mobile devices – that some had predicted. Visa and other payments networks, stretching back a few years to 2017, had debuted the world’s first interoperable QR code acceptance solution in India.

It’s not fair, said FI.SPAN CEO and Co-Founder Lisa Shields, that Bill.com and AvidXchange get to have all the business payments fun — and there’s no reason why banks shouldn’t get to participate. Banks don’t ask for APIs, said Shields. It becomes a technological project for both the bank and for the customer.

It’s not always easy to tell the difference between the meaning of integrations and interoperability: Integrations are systems connected in the same way, while systems that are interoperable work together, but remain different. It just works.”. The same concept can be applied to payments.

Women, refugees, the poor and the young had historically had low inclusion in Jordan’s banking system because there’s no good onboarding process for them – but mobile-phone penetration runs deep across Jordanian society, even among critically underbanked segments. Building Better Payments And Banking Services .

UPI is a real-time payment system developed by the National Payments Corporation of India (NPCI) that enables instant money transfers between two bank accounts through a mobile platform. These guidelines enable non-bank entities to enter the payment aggregation business and expand their scope to include the import of services.

In a mutual commitment to accelerating the adoption of an open digital wallet, global card networks Mastercard and Visa announce their agreement to allow each network to request tokenized credentials from the other when consumers are transacting across any digital medium — in app, online and in store. Tokens Get Turbocharged. A Global Push.

Alipay+ , Ant International’s cross-border mobile payment and digitalization solution, revealed three trends shaping the future of tourism to the benefit of global merchants and the industry. Alipay+’s mobile payment partners from around the world have also seen significant growth.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financial inclusion and helping people develop healthy financial habits.

When it comes to open banking, there’s a clear choice in place: by fiat, which includes formal processes, or by evolution, which would imply letting the market dictate what happens. In an interview with PYMNTS’ Karen Webster, Clayton Weir, co-founder and chief strategy officer of FI.SPAN, revealed the promise and the peril of open banking.

24) a host of new strategic partnerships to bring online payments capabilities to digital wallets users in the U.S. The agreements will allow Mastercard cardholders to use the mobile wallets to shop online at the hundreds of thousands of merchants around the world where Masterpass is accepted. Mastercard announced today (Oct.

It’s a stalemate, Movile CEO Patrick Hruby told Karen Webster, that can likely be broken if Facebook agrees to integrate its service with the central bank-backed instant payments platform PIX, slated for rollout in October. “In The changes that are happening in Brazil and across the region, he noted, aren’t exactly new.

Open banking efforts are live in countries ranging from the United Kingdom to Singapore. Financial institutions (FIs) following these initiatives make their application programming interfaces (APIs) publicly available, which third-party developers can use to create solutions that draw on banking data from consenting users.

MasterCard and Vodafone have secured a new deal that will have MasterCard powering Vodafone Egypt mobile money service, Vodafone Cash. As part of this pair up, MasterCard has moved 2 million Vodafone Cash mobile wallets on its own mobile payments network. This was done in collaboration with the Egyptian Banks Company.

Whether we will see these services gain traction is tied to what many believe to be a major hurdle–interoperability. FedNow may not interoperate with RTP, and it doesn't seem to be a priority for either. Some banks may not be able to connect to both. These projects are taking different implementation approaches.

HSBC is gearing up to take on Hong Kong P2P mobile payment company Jetco, launching its own P2P mobile payment app. According to a report , HSBC has a holding page online that invites cardholders to sign up for the payment service. The app, dubbed Payme, will enable cash transfers to people with just their mobile phone number.

Due to the low penetration of credit cards, barriers related to banking access, and consumer behavior, fintechs and governments began seeking solutions to simplify consumers’ lives and allow them to purchase products and services using local payment methods. billion, or 48% of the market, according to PCMI data.

Having established what regulatory challenges banks and fintechs should be aware of when leveraging banking-as-a-service (BaaS), and how the technology is advancing financial inclusion across the globe, we now turn our attention to emerging trends and if they are region-dependent.

If the definition of insanity is doing the same thing time and again and expecting different results, then perhaps the way we pay through, and interact with, onlinebanking may have a hint of madness, or at least complacency. Security only works if both ends are using the network — and the world is a big place with lots of banks.

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. And thats a really positive development.

We're focusing on the ability for consumers to use their rewards points at over 60 million merchants around the world, whether that’s online, in-store or via contactless using a major wallet such as Apple Pay or PayPal – and really bringing [loyalty redemption] to life.”. Points as Cash Requires Program Interoperability. My Rewards 2.0

“With rapidly accelerating digital payments growth across Central and Eastern Europe, Middle East and Africa, we have seen a transformation in how consumers and merchants want to pay and be paid both online and in-store,” said Andrew Torre, Regional President, Visa CEMEA. “As

a number of leading tech companies have become vocal in their support of a real-time payments (RTP) network, to be created under the leadership of the Federal Reserve and different from what has been previously proposed by the big banks. In a recent example, in the U.S., Signing On, With ROI in Sight.

Instead of waiting for their table at a restaurant or for their name to be called by a doctor, consumers can check in to dinner reservations and medical appointments remotely via a mobile device. billion consumer accounts, including credit or debit cards, online wallets and cash-out distribution points. About The Tracker.

Like the giant puzzle pieces that keep the Earth’s surface in equilibrium, the ecosystems that represent how consumers pay, how they bank, how they borrow, how they shop and how they decide when, where and what to buy used to be easily defined and neatly connected. The Unbundling Of The Bank. The Commoditization Of Retail.

When shopping online, Visa passkeys replace the need for passwords or one-time codes, enabling more streamlined, secure transactions. There is a global desire to find commonality, interoperability and simplicity for online payments. Already available across Europe, this product was rolled out to the US market late last month.

Tap to Everything There are six billion mobile devices in the world2 providing consumers with a versatile NFC enabled device primed to be “tapped.” 3 This year, new ways to “tap” on a mobile device will become an integral part of the Visa experience. Today, online payment fraud is seven-times higher than in-person payments.

Taken as a group, the platform companies show that consumers are increasingly comfortable coming online to get what they need, that ad targeting is working, and that the companies that are pivoting online to reach consumers where they are — namely, on mobile devices and tablets — are embracing new ways to monetize that contact.

The inaugural "Faster Payments Barometer," an online survey of industry professionals, published in Fall 2019, offered insights across businesses, financial institutions (FIs), and payment providers. The bank bill pay model where the consumer interacts with its online/mobilebanking platform to request a payment be sent to the biller's bank.

Mobile Nordic Future. Oberthur Technologies (OT) is partnering with payments service provider Nets to deliver support for mobile payments to Scandinavian banks. 6, is aimed at helping to service banks in the Nordics with a financial platform that supports future international mobile payment methods.

“India has recently achieved unprecedented levels of financial inclusion and is actively promoting the adoption and growth of the online sector,” explains Rashmi Satpute , country director of India at EBANX. Including mobile money, APMs will represent around 63 per cent of African digital commerce by 2025.

In addition, Razer ’s mobile wallet dubbed Razer Pay may come to tens of thousands of point-of-sale (POS) terminals in Singapore , and a Worldpay study has found that consumers in Singapore still prefer to make payments with credit cards over eWallets. At the same time, only 13 percent of adult smartphone users in the U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content