This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Card issuers need for speed exists on several levels, and we at OpenWay see this firsthand, since our Way4 card management software is used by top banks, processors and fintechs around the world. This flexibility allows issuers to quickly innovate a common product for a new business model. gaming) but accepted at approved merchants.

While many banks and issuers still use one-time passcodes (OTPs) to protect customers from fraud, modern tools and attack vectors make their days at the office rather easy. Faster payments and faster fraud As new payment use cases and systems emerge, they naturally introduce new fraud risks. Its a great time to be a fraudster.

Defining “acceptable risk” in UK payments regulation 13 March 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? How the FCA can define and balance acceptable risk in UK payments regulation to support innovation while ensuring financial stability and consumer protection. What’s next?

Source: 2025 State of Chargebacks: A GLOBAL VIEW FOR ISSUERS AND MERCHANTS A significant chunk of the expected increase in chargebacks will occur in North America, with the expected volume of chargebacks reaching 132.9 million in 2028 from 114.4 million in 2025.

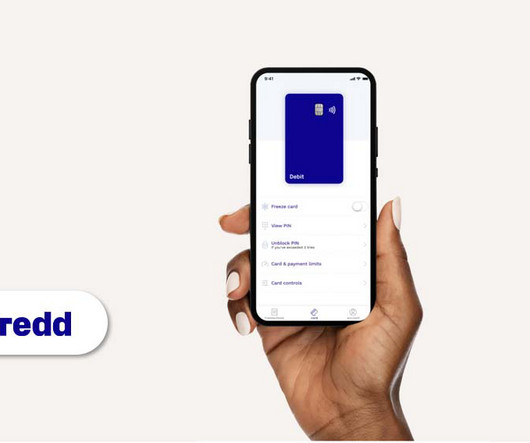

Patricia Haynes joins as Senior Vice President of Platform, bringing her expertise in technology operations and risk management from roles at Zopa and LexisNexis Risk Solutions. This move is part of Thredd ‘s efforts to strengthen its platform, products, and regional support for fintech firms and programme managers worldwide.

Ballerine , an AI risk intelligence platform designed to help financial institutions, fintechs, and marketplaces automate and optimize merchant onboarding, verification, and lifecycle monitoring processes, announced the appointment of Cihat Fitzgerald as Chief Risk Officer.

Tribe Payments , the pioneering digital payments and infrastructure orchestrator which specialises in issuer and acquirer processing, has been selected by embedded financial services platform, Orenda Finance , to provide its issuer processing services. Íkualo hopes to reach 70,000 active accounts in the country.

Tribe Payments has been chosen by SetldPay to provide their issuer processing, with the company also benefitting from Tribe’s Risk Monitor and 3D Secure solutions. 3DS has become an essential part of risk management and fraud prevention for any business that takes online payments.

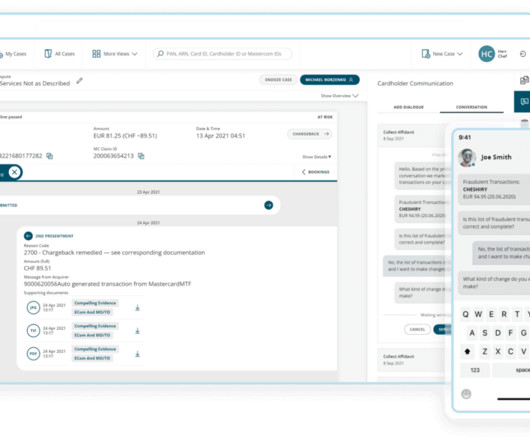

Managing fraud cases has been a top challenge for card issuers, according to recent studies. Rising operations and outsourcing costs and burgeoning fraud recovery caseloads make it especially challenging for issuers to meet chargeback deadlines and avoid cardholder write-offs.

Fraud rates are seven times higher online than in stores1, as criminals exploit exposed card numbers, creating headaches for cardholders and huge losses for merchants and card issuers. Additionally, the risk of fraud is minimized. Mastercard’s technology is already making online checkout quicker for businesses.

For payment processors and financial institutions, however, understanding BINs is essential for smooth transaction processing, security, and even risk management. Payment processors use this data to authenticate the card details, ensuring that the card being used matches the card type, issuer, and other key characteristics tied to the BIN.

Patricia previously served as VP of Technology Operations and Delivery at Zopa, where she led risk management and process improvements, and Senior Director of Software Engineering at LexisNexis Risk Solutions, spearheading AML and compliance technology initiatives.

Card programs can increase purchase authorization rates without taking on undue fraud-liability risk with 3-D Secure (3DS). Here’s what it is and how card issuers can leverage it.

Network tokenization stands out as another prime example, as it replaces sensitive card data with encrypted identifiers for each transaction, reducing fraud risk without compromising approval rates. The post EBANX Data Shows 41% of Online Card Transactions in Brazil Come From Digital Issuers appeared first on FF News | Fintech Finance.

An issuer decline code is provided by an issuing bank to a merchant, indicating the rejection of a credit card transaction. This means that the issuer has halted or blocked the transaction. The specific code gives a brief reason for why the issuer turned down the purchase.

ACI Worldwide (NASDAQ: ACIW), a global leader in mission-critical, real-time payments software, and RS2 , a global payments processor and technology provider, have joined forces to offer a one-stop solution for acquirers and issuers in Brazil.

Apart from keeping complex payment structures running, interchange fees compensate issuing banks for taking on cardholder credit risk, and help card companies fund rewards programs. Covers risk taken on by issuing banks Issuing banks take on financial risks while extending credit to cardholders. Even for low-risk cards (e.g.,

This PoC provided an opportunity to explore insights into technological risks associated with digital assets across multiple blockchains. Transparency and risk management are critical to supporting institutional engagement in tokenized finance.” Contact Renjie Butalid VP Business Development Metrika renjie@metrika.co

The card scheme Click to Pay mandate underscores this evolution, making it mandatory for issuers to adopt a more streamlined, card-on-file experience that prioritises security and user convenience. But beyond compliance, what does Click to Pay mean for the payments industry today, and how can card issuers navigate this transition effectively?

Debit card issuers face an ever-growing array of fraud schemes perpetrated against them and their account holders. Two-thirds of card issuers were expected to offer contactless debit products by the end of this year, for example, and 87 percent of all cards are anticipated to be contactless-enabled by the end of 2022.

Mastercard wants to build confidence in open banking by addressing regulatory compliance, liability, and technology integration issues on behalf of its issuers and fintechs.

As well as chargeback fees, there’s also the risk of banks choosing to freeze or even terminate merchant accounts. These records can serve as valuable evidence in the event of a chargeback dispute, helping you present your case to the card networks or issuers.

Lin Tao ( Prezzee ) highlighted the disproportionate risk her industry faces: Gift cards are inherently attractive to scammers due to their high liquidity and minimal traceability. The card issuers often side with the customer without consulting us, which is unfair and costly.

For e-commerce players, this means fewer abandoned carts and a lower risk of fraud, while consumers can benefit from faster checkouts and peace of mind. For issuers, this is an alternative to have their cardholders authenticated, reducing fraud risk. Upon successful authentication, the transaction is completed.

For issuers, Tap to Add Card can help reduce the risk and associated costs of provisioning fraud, simplifies the add-to-wallet process leading to fewer customer service inquiries, and improves transaction approval rates. This significantly improves the customer experience.

Heres a simple breakdown: Interchange fees: Interchange fees go to the customers bank (the card issuer). Acquirer fees: Acquirer fees go to the financial institution that underwrites the credit and takes the financial risk. Assessment fees: These go to the card networks like Visa and Mastercard.

Credit card issuer (or issuing bank) – These are financial institutions that issue credit cards to customers. Also known as card companies or card issuers (e.g., The exact fees you pay can vary depending on the type of card used, the card issuer, the credit card network, the type of transaction, and the pricing model (e.g.,

Ally Financial's recently announced $2.65 billion cash-and-stock deal for CardWorks, which offers unsecured credit cards among other products, places a high price tag on a traditionally risky product.

.) : Card networks , such as Visa, Mastercard, American Express, and Discover, play a critical role by routing transaction data between acquirers and issuers (cardholders’ banks). They also set interchange fees that cover transaction costs and risks. Market Size and Growth The U.S.

In our industry, the ability to move large payments instantly, securely and reliably is crucial, said Ann Bowering, CEO of Computershare Issuer Services, North America. With real-time payments, we can settle higher-value transactions immediately, reducing counterparty risk and improving overall working capital efficiency.

Risk-based authentication (RBA) offers a way forward, balancing security and user experience while addressing the growing sophistication of fraud. With many banks and issuers still using one-time passcodes (OTPs) to protect customers from fraud, modern tools and attack vectors make their days at the office easier.

Credit card issuers caught in the trap of chasing new customers with increasingly costly rewards-point programs are trying something new: letting more users redeem rewards directly with merchants instead of acting as the intermediary.

Card fraud risks — already soaring prior to the coronavirus outbreak — are changing rapidly as the pandemic deepens, forcing issuers and merchants to rethink protective measures.

Credit union credit card issuer Collabria Financial Services has teamed up with digital identity verification fintech Trulioo. The Canada-based card issuer will leverage Trulioo to streamline the verification process for new cardholders.

For issuers, Tap to Add Card can help reduce the risk and associated costs of provisioning fraud, simplifies the add-to-wallet process leading to fewer customer service inquiries, and improves transaction approval rates. This significantly improves the customer experience.

Paymentology , a global issuer-processor, announced the appointment of Jim Hart as its new Chief Information Security Officer (CISO). Hart has also advised both scale-ups and large enterprises on cybersecurity and risk mitigation. Hart brings over 25 years of IT security experience to the role.

Lin Tao ( Prezzee ) highlighted the disproportionate risk her industry faces: Gift cards are inherently attractive to scammers due to their high liquidity and minimal traceability. The card issuers often side with the customer without consulting us, which is unfair and costly.

As innovation continues in the virtual asset space, regulatory authorities in Hong Kong have proposed new regulatory rules for stablecoin issuers. Under the proposed regime, issuers would require a license from the HKMA to issue stablecoins that reference the value of one or more fiat currencies in Hong Kong.

Paul Fabara , chief risk and client services officer at Visa Paul Fabara , chief risk and client services officer at Visa , explained the impact the new tool could have: “Enumeration can have lasting impacts on our clients and there’s an immediate need for tools that can better detect and prevent these attacks in real-time.

issuers, the tool assigns a risk score to each transaction, focusing particularly on card-not-present (CNP) transactions, to identify potential threats without impacting transaction integrity. Visa has invested over US$10 billion in the past five years, aimed at enhancing network security and reducing fraud risks.

The award recognises technology providers that significantly enhance regulatory compliance and operational efficiency for merchants, issuers, and acquirers. ” Vixio’s Horizon Scanning Tool tracked over 523,000 regulatory updates in the first nine months of 2024 alone, with hundreds requiring immediate attention. .

While this payment method remains popular due to Visa and Mastercard’s robust consumer protection frameworks, it is essential for issuers to ready their operations for the anticipated rise in disputes. Without proactive measures, institutions risk overwhelmed back-office teams and diminished customer trust.”

Tribe Payments , a leading digital payments and infrastructure orchestrator that specialises in issuer and acquirer processing, has partnered with digital financial platform, Ribbon , enabling the company’s launch first in Gibraltar and, most recently, in the UK.

Nonetheless, firms must understand how to navigate them properly or risk facing growing fraud figures, and a new report from payments giant, Mastercard , in partnership with Datos Insights delves further into this topic.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content