This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

UPI is a real-time payment system developed by the National Payments Corporation of India (NPCI) that enables instant money transfers between two bank accounts through a mobile platform. These guidelines enable non-bank entities to enter the payment aggregation business and expand their scope to include the import of services.

Over 200 submissions were received across six categories, with 175 entries in the corporate categories and 29 in the individual Fintech Mentor Award category. It enables financial institutions, especially those without core banking systems or with systems lacking API integration, to manage bulk transactions. ThitsaWorks Pte.

A 2018 survey by Bank of America shows that millennials’ top financial priorities were saving for emergency funds (64%), saving for retirement (49%), and saving to buy a house (33%) — not much different from the concerns their baby boomer parents had 30 years ago. From big banks to big tech. get the REPORT on next generation investors.

NACHA, the payments clearing house through which ACH transactions flow, reported a banner year in 2020, posting an 8.2% Specifically, ACH Originators of WEB debit entries are required to use a “commercially reasonable fraudulent transaction detection system” to screen WEB debits for fraud. Trial and micro deposits of just a few cents.

ACH (Automated Clearing House) payments are electronic fund transfers that use the ACH network to move funds between bank accounts in the United States. Banks would compile ACH transfers onto tapes once per day, and ship the tapes to the clearing house to have the transfers distributed to the banks they are meant to go to.

As more people have worked, learned, banked, exercised, relaxed, and even sought medical care from home during Covid-19, they have gotten a crash course in just how much can be accomplished at home. Branchless banking. BANKING, HEALTHCARE, RETAIL SECTORS LIKELY TO EXPERIENCE SIGNIFICANT GROWTH IN CHATBOT USE. Cloud call centers.

Instead, it was an ecosystem of apps that they used regularly and could access on their mobile phones: Uber, Amazon, Walmart, PayPal, Square, banking apps, OpenTable, Facebook, Instagram, Google, Venmo – and yes, WhatsApp and Messenger, to name but a few. Just like WeChat did. Of Messenger and Libra.

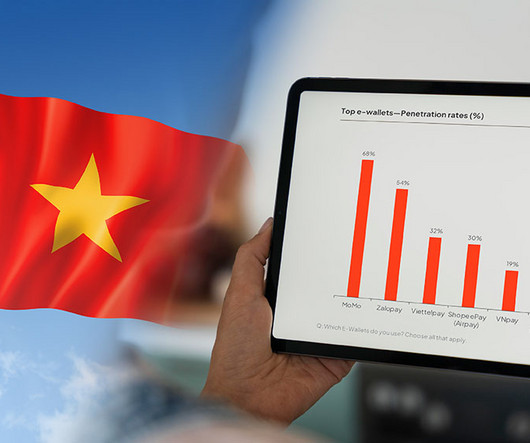

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

If Amazon can get you lower-debt payments or give you a bank account, you’ll buy more stuff on Amazon.”. Based on our findings, it’s hard to claim that Amazon is building the next-generation bank. In aggregate, these product development and investment decisions reveal that Amazon isn’t building a traditional bank that serves everyone.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content