This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This Friday, March 28, 2025, marks the end of an era for DBS Bank as Piyush Gupta steps down after an extraordinary 16-year tenure as Chief Executive Officer. During his tenure, he turned DBS from a traditional lender into a globally recognised powerhouse of digital banking. His leadership has been nothing short of transformative.

Like most business owners, your instincts tell you to hop on the bandwagon and launch an online store for your business. From different types of online payment gateways and key features to look for, to tips to help you choose the right payment solution for your business and implement it. This is expected to grow to 22.6%

And yet, accepting non-cash forms of payments is more or less required to operate a modern business, at least in the U.S. They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. Acquiring Bank: The business’ (i.e., merchant’s) bank.

In simple, layman’s terms, embedded finance is when financial services – like payments, loans, or insurance – are integrated directly into non-financial platforms. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

However, mobile payments, digital wallets, and real-time transactions are broadening financial access. How does the rise of real-time payments impact traditional banking in Latin America? Growth is driven by financial inclusion, fintech innovation, and regulatory reforms. Key Takeaways – Report Summary 2. Management Summary 3.

Whether you are starting a new online store or looking to grow your existing brick-and-mortar small business, you must make provisions for accepting credit card payments. A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%.

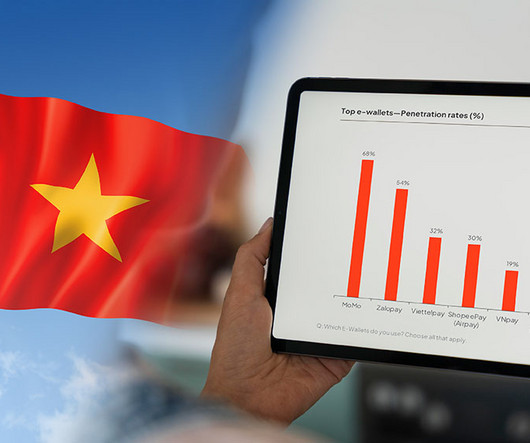

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. They let buyers initiate payments by placing their mobile phone near a compatible payment terminal.

They enable secure, efficient in-store and online payment processing and offer flexible payment options that customers demand today. Merchant services are comprehensive solutionstools, systems, and supportthat allow businesses to process in-person and online payments. custom software for a particular industry or market).

These methods leverage digital wallets, mobile payments, bank transfers, and other innovative technologies to deliver more flexible options for consumers. Region-Specific Preferences : In Europe, 36% of online purchases are made through bank transfers, while Asia sees a dominance of digital wallets at 70% of transactions.

The latest version of its non-custodial DeFi app elevates it into a decentralized banking ecosystem with a host of new features including a crypto debit card. Multi-chain deposits, yield-earning options, seamless worldwide spending, and gamified educational features support a robust suite of alternative banking services.

While brick-and-mortar retail isnt going away, todays customers value the convenience of shopping online. That means selling your products and services online allows you to better serve your customers (and reach new ones!) To accept online payments, you need a payment processor and payment gateway. all while increasing revenue.

More than three-quarters of Americans now prefer to pay their bills digitally, especially Gen Z and Millennials, who show a significant inclination toward mobile payments. However, this increase in digital payments also brings about heightened risks – almost one in five consumers surveyed has fallen prey to online identity theft.

Accepting payments always comes with processes and fees, particularly when it comes to online or digital payments. TL;DR A payment link enables you to request and accept online payments without having to build a website or checkout page. Payment links are ideal if you don’t process a lot of online sales.

Confronted by shifting factors such as tech advancements, generative AI, high interest rates, increased institutional oversight, and evolving customer expectations — the best banks must adapt their business and operating models in 2024, including in Asia. CHINA #1 China Merchants Bank China Merchants Bank Co.,

Are digital first banks in Asia poised to lead a disruptive charge against well-entrenched, established commercial banks? In the traditional banking sphere globally, but especially true in Asia, there is a considerable proportion of unbanked and underbanked populations who lack complete or any access to banking services.

per cent Central Bank of Armenia (CBA) Armenia’s growth has been driven in part by its young, tech-savvy population. Through its regulatory sandbox, the Central Bank of Armenia (CBA) has attracted $90million in investments, propelling the country to 34th place in the Global Fintech Index 2023. per cent holding a credit card.

With a payment gateway, they simply enter their card details online on your website or app. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer. For example, if you operate an online store, you need fast and secure online payment solutions.

For online shopping, Visa passkeys replace passwords or one-time codes. Click to Pay – Enables consumers to complete online transactions within a few clicks, powering a more seamless and secure checkout experience at scale. to broaden its merchant coverage network across Japan.

The plastic card, by necessity, is giving way to digital cards, and mobile apps are bringing card-not-present transactions, increasingly, to mobile devices. She noted that mobile app use is up double-digit percentages as of April, when the pandemic shifted so much of everyday life online.

However, in recent decades, the government has engaged in efforts to diversify the economy to include other agricultural products, as well as non-agricultural sectors such as tourism and natural resources like oil, gas, and gold. Mobile phone usage in Senegal has surpassed 60 per cent this year. appeared first on The Fintech Times.

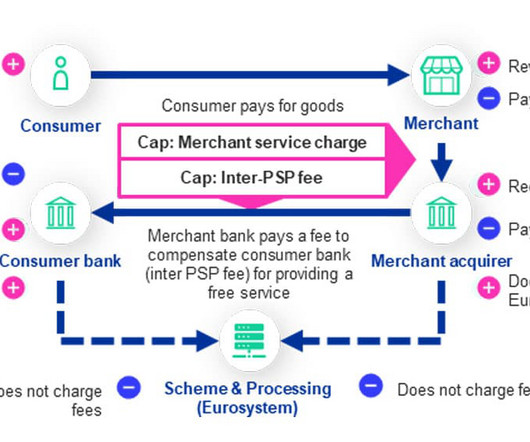

TRANSACTION FEE: A step-by-step overview of the digital euro compensation model Payment service providers will be able to charge merchants a fee for enabling them to accept digital euro transactions, the European Central Bank (ECB) has revealed, but a cap will be placed on the amount that it will be possible for them to charge.

TL;DR Online payments rely on API or hosted gateways with encryption and fraud detection, while in-store transactions require POS hardware with EMV chip technology and NFC capabilities. The issuing bank verifies whether the customer has enough funds in their account to complete the transaction.

Coverage includes Singapore’s Singtel rollout of international payment options in its Dash mobile app. In addition, PUC Berhad is teaming up with Revenue Group Berhad for online-to-offline (O2O) payments in Malaysia , and the United Kingdom’s Metro Bank is upgrading its mobile app to bring mobile payments to over 38 nations.

As traditional banking processes are replaced by more integrated financial solutions, companies across industries are embedding payment processing, lending, insurance, and investment services directly into their platforms. global banks) is now open to independent innovators who can embed payments into the fabric of everyday interactions.

The Australian Securities and Investments Commission (ASIC), the country’s financial regulator, has filed documents against HSBC Bank Australia as it alleges the bank failed to adequately protect customers from being scammed out of millions of dollars. “All banks need to pull their weight in the fight against scams.

Using digital wallets and mobile payment apps were once emerging trends but are now becoming common practice for both online and in-store purchases,” Christine Roberts, EVP, and President of Citizens Pay told Tearsheet recently. Moreover, online purchases drive higher digital wallet usage compared to in-store transactions.

Tap to Everything There are six billion mobile devices in the world providing consumers with a versatile NFC enabled device primed to be ‘tapped’ At the end of 2023, Visa’s tap-to-pay penetration reached 65 per cent globally, up two times the penetration we saw in 2019, cementing tap as one of the best commerce experiences today.

Make that leather wallet a mobile one, wielded on smartphones. As we noted in this space earlier in the summer, using apps to bank is markedly being embraced by the younger generation. As spotlighted in the Digital Banking Tracker , the global digital banking market is slated to grow by 16 percent, compounded annually.

The pandemic has exposed the pain points of all verticals when it comes to payments, and especially when it comes to transacting in person, in a tactile environment, with cash, and where banking conduits are limited. Banks have been inching into the space; cash still remains a hallmark.

DBS Bank has announced the restoration of its digital banking services after a temporary disruption that affected its DBS/POSB digibank Online and Mobile platforms, as well as DBS PayLah! times on the bank’s operations. The bank or MAS have yet to release an official statement on the matter.

The coronavirus pandemic — which has forced all of us online — is exposing just who in financial services has embraced digitization, and who is truly digital native. We now must bank entirely online, by necessity. And many of us must transact entirely online, by necessity, to get the goods and services we need on a daily basis.

In a statement, the company noted that these options work across all purchasing channels, whether online, in-store, or via sales teams. SBSN empowers banks to expand their offerings to small businesses by enabling them to access the small business B2B trade credit market. March has been a busy month for TreviPay.

DBS and POSB customers faced difficulties accessing the bank’smobile apps on Saturday morning, with over 500 reports of issues recorded on outage tracking site Downdetector since 7 am. A notice on the app indicated potential difficulties for customers accessing their digibank mobile services.

As the financial services space focuses on digitizing offerings for their small business customers, much of these efforts are targeting onlinebanking portals accessed via desktop. One of the biggest impacts of mobile-based services will be the shift from weekly or monthly processes to operating in real time. .

Last week, wireless carrier T-Mobile announced it would throw its hat into the mobilebanking arena with the national rollout of T-Mobile MONEY. The mobile app offers low or no-fee checking-like services, out-of-network ATM usage fees and the ability to earn 4 percent APY on balances of up to $3,000. In fact, 72.4

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

Completing online payments via manual card entry can be time-consuming and off-putting for customers. Click to Pay completely removes the need to enter credit card information during online purchases, making it more convenient and faster than manual card entry. Learn More What is Click to Pay?

Questions like, “What is a bank?”. It’s a fair question today, particularly as we observe the blurring of the lines between traditional banks, Big Tech and FinTechs — and as we contemplate the impact that the blurring of the digital and physical worlds has on consumers’ expectations and customer service paradigms.

Dwollas clients are now able to leverage Plaids instant account verification and real-time balance check alongside comprehensive pay-by-bank payments through a single vendor and a single API. Fintech myPOS unveils a new strategic partnership with Satispay , an Italian independent mobile payment firm.

In today’s top news in digital-first banking, FIS is working with Quontic Bank on the Bitcoin Rewards Checking Account, while Aeldra has chosen i2c Inc. to power its digital private banking offerings. FIS Powers Launch Of Quontic Bank’s Bitcoin Rewards Account. Aeldra Taps i2c To Enable Global Banking Services.

Quality Engineering is transforming digital banking, enabling seamless innovation, operational continuity, and future-proofing in a rapidly evolving landscape. The global banking industry is currently undergoing widespread change from a regulatory and technology perspective. These large-scale projects are inherently risky.

Visa has signed an agreement with Abu Dhabi Islamic Bank (ADIB) to collaborate on an enhanced threat intelligence solution and integrate its advanced cybersecurity capabilities with digital payments. Additional partnerships MiFinity, a global payment services provider, has integrated Apple Pay into its mobile app.

Mobile and onlinebanking providers have been upping their fraud protection measures over the last decade, making it more difficult for bad actors to rely on some of the schemes that previously worked in such channels. Banks need to think of their fraud strategies as items that are constantly changing, Venturo explained.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content