This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In 2023, 27% of all point-of-sale (POS) payments were made using credit cards while 23% were made with debit cards. Behind every seamless payment card transaction is a complex network of banks, credit card companies, and payment systems working together to transfer money from the customer to the merchant.

Appointments Sibstar, the UK debit card and app for people living with dementia, has appointed GoHenry co-founder and CEO, Louise Hill, as a non-executive director. Most recently Neil was a trader at Triland Metals and he rejoins Britannia having been at the firm between 2019 and 2023 as a base metals sales trader.

The payment processor is a financial institution that handles transactions between the two banks. Instead of driving down the complicated road of bank transfers or check payments, you can give your customers a simpler way to complete their purchases through your own website. But what’s the difference between these two?

TL;DR: Electronic Funds Transfer (EFT) is the umbrella term for all electronic payments made between bank accounts. Talk to sales Understanding EFT: The Umbrella Term for Digital Transactions Ever paid for your coffee with just a tap of a card or received payment from a customer thousands of miles away? No cash or checks needed.

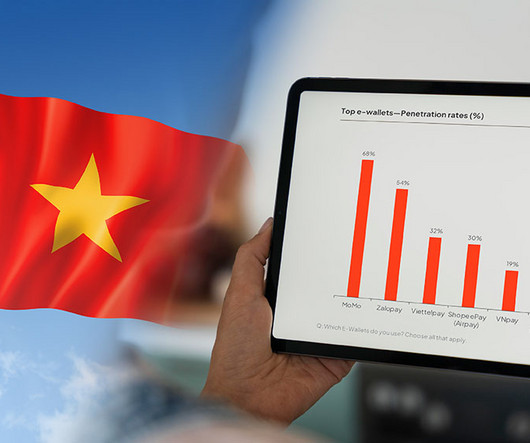

Vietnam’s digital finance landscape is undergoing a notable shift as new players emerge, established ones fade, and traditional banks rise to prominence, a new report by Decision Lab shows. However, by Q4 2023, Moca had slipped out of the top rankings, replaced by mobile apps from traditional banks.

Home Credit , a global non-bank consumer lender, has successfully reduced its credit risk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China.

A study by the Federal Reserve Bank of San Francisco showed that credit cards account for 31% of all payments, significantly more than cash at 18%, and debit cards at 29%. The customer can make the credit payment physically by swipe, dip, or tap, depending on your point-of-sale (POS) system , which will capture the credit card details.

EAZY Financial Services ‘EazyPay’, a Bahraini financial institution specialising in point-of-sale (POS) and online payment gateway acquiring services, has teamed up with Tarabut , the MENA region’s regulated open banking platform. Most recently, he served as chief operating officer at Bankable.

Its a digital evolution of the conventional point-of-sale (POS) terminal. A physical POS terminal requires customers to insert, swipe, or tap their cards on the machine. In turn, the payment processor ensures a seamless transfer of the information between the merchant, issuing bank, and customer.

These efforts include TCH’s efforts to connect financial institutions’ (FIs’) core banking systems to the company’s Real-Time Payments (RTP) network, along with what card networks and FinTechs are doing to enable real-time push payments to receiver bank accounts. Achieving ubiquity across the 12,000 or so FIs in the U.S.

The issuing bank verifies whether the customer has enough funds in their account to complete the transaction. Once approved, the information is sent to the merchants bank account, where the funds are deposited. If necessary, you need to apply for a merchant account through a bank or payment processor.

Brett Narlinger , head of global commerce at branded payments provider Blackhawk Network , said some of that stems from consumers who lack banking system access and find cash the easiest way to handle transactions. Countless think pieces have been written about how cash is on its last legs, but somehow it keeps sticking around.

It will also continue to invest in its comprehensive tech stack to power the end-to-end customer journeys across banking, insurance, and embedded commerce. Founded in 2008, Perfios is a B2B SaaS company serving the banking, financial services and insurance industry in 18 countries, empowering 1,000+ financial institutions.

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

In the initial phase, Paymob will integrate MID Takseet into its point of sale (POS) terminals to facilitate in-store card and digital wallet transactions, with online integration slated for the second phase. MID Takseet offers advanced non-banking financial solutions, fostering growth for businesses and customers.

This will prompt industry stakeholders to heighten their efforts to address cross-border payment inefficiencies through developments in crypto payment systems, the expansion of real-time payment capabilities, and solutions aimed at enhancing foreign exchange management and banking access across different countries.

has established a new pinnacle by executing the first non-Apple Pay account-to-account near-field communication (NFC) payment on an iPhone. celebrated the successful execution of the experimental transaction in development mode, setting the stage for what could revolutionize Point of Sale (POS) interactions.

Businesses of all types are deploying new initiatives to meet this demand, with merchants like CVS Pharmacy rolling out QR-based payment integrations at store locations across the country, and payments providers like Square and PayPal introducing QR codes at their point-of-sale (POS) systems.

Here’s some more details: About 60% of the compromises were at non-bank ATMs, such as those in convenience stores. The rest took place at bank ATMs or point-of-sale (POS) devices, such as card payment machines at retailers. This new data follows a 546 percent increase in compromised ATMs from 2014 to 2015.

It was a team of cybersecurity researchers from the firm ERPScan, and not malicious hackers, who discovered that point-of-sale (POS) systems made by SAP had a gaping loophole. It was later revealed that non-celebrity users of the photo-sharing social network were also affected, though Instagram did not say how many.

This week’s commercial card innovation tracker finds a tie-up between a FinTech and a neo-bank to make cards available for Google Pay, as well as a Tokenization-as-a-Service offering from a card issuing platform. FinTech firm Nium has teamed with Southeast Asia neo-bank Aspire to enable a mobile payments feature with its cards.

Point-of-sale (POS) terminals became commonplace, allowing businesses to process payments seamlessly. For example, PSD2 in Europe opened payment services to non-bank providers, encouraging fintech innovation. They offered convenience and security by eliminating the need for physical cash.

In the initial phase, MID Takseet will be integrated into Paymob’s point of sale (POS) terminals to power in-store card and digital wallet transactions, with online integration to follow in the second phase.

This has been made possible via Network’s point-of-sale (POS) terminals in the UAE. This initiative ensures seamless and secure transactions for Indian tourists and non-resident Indians (NRIs) across Network International’s merchant network in the UAE.

For a merchant to accept credit cards, they need to pay both credit card processing fees to the banks involved and for the soft and hardware required to process cards. Acquiring Bank (Merchant Bank): The financial institution that establishes and maintains the merchant’s account, enabling them to accept credit card payments.

There are all kinds of frauds taking root out there, but among the more popular are the spoofing scams in which the consumer gets a phone call from “the IRS” or “their bank” making requests that absolutely no consumer should ever acquiesce to. Banks do not call you and ask you for your personal information,” she said.

TL;DR A payment gateway is a solution that securely reads and transfers a customer’s payment information to a merchant’s bank account—both for online and in-person transactions. Think of it as a cash register, except that the payments it processes are non-cash.

And when that happens, non-compliance can lead to many degrees of harm to any and all business owners. It gets worse: merchants that use a non-PCI certified provider can face class action lawsuits, fines of up to $10,000 per month, and $500,000 per incident. As such, they’re typically the ones that are scrutinized the most.

Credit card merchant fees are split between multiple key players- merchants, credit card networks, banks, and processors. Interchange fees are set by credit card issuers, such as Bank of America, Citi, or Chase, and are adjusted every year in April and October. to 2.9%) while the non-qualified is the highest.

And in commentary on the latest earnings call, CEO Jack Dorsey and Chief Financial Officer Amrita Ahuja said that the move toward online sales saw online store GPV surge by more than five times since mid-March, to a weekly run rate at $59 million, or $3 billion on an annualized basis. Where The Bright Spots Lie.

In some cases, when a traditional bank shuts the door on an SMB applicant, a business owner may not know where else to turn for capital. Financing also enables small firms to obtain equipment without making a dent in the lifeline of a bank line of credit. Financing Modernization. But the price tag is rarely painless.

As stated on the post-earnings conference call with analysts, CEO Charles Scharf said, “if confidence does deteriorate and the shelter-in-place orders stay on for longer, which is possible, then it wouldn’t surprise me that loss estimates would have to go up from this point.”. Overall credit card loans were down by $2.4

Algorithms are taking on more of the data and security work for financial institutions (FIs), with technologies such as data mining and business rules management systems (BRMS) finding popularity among banks and credit unions. Large Versus Small Banks. In the case of BRMS, use has dropped off significantly for the largest banks.

NexPay , a global education payments, has unveiled new board roles including David Jonhstone as non-executive chair, Rajesh Yohannan, the current CEO of Axi Corp, as a non-executive board director, as well as Clive Wilson to the newly created role of chief risk and governance officer.

However, recent stringent regulations imposed by the Reserve Bank of India (RBI) have significantly impacted the sector, leading many fintech companies to reassess their BNPL strategies. Similarly, Slice, originally a BNPL firm, has transitioned to offering prepaid credit cards and is now merging with North East Small Finance Bank.

Mastercard announced Tuesday (April 4) that Mastercard cardholders from select banks in the United Arab Emirates (UAE) will now be able use the Samsung Pay service to make payments in a quick and secure way. Mastercard said it has been actively driving contactless payments in the market.

This approach is commonly used by eCommerce platforms, point-of-sale (POS) systems, and other software that facilitates online or in-person payments. Established payment platforms have already cultivated extensive user bases, merchant networks, and partnerships with banks.

Pintec allows banks, non-bank FIs and businesses to turn on a host of services that, in essence, allow them to custom build their own consumer ecosystems. If you look at, for example, a second- or third-tier bank, however, they aren’t going to have all of that time and money to experience.

Your PMS is a central hub to manage payment requests and store banking information (like your routing and bank account number for ACH payments ). Payment processors handle the nitty-gritty of authorization, settlement, and transfer of funds between your business and your customer’s bank.

According to a recent report from Worldpay , 65 percent of eCommerce spend, and 36 percent of point-of-sale (POS) spend in the country, came from mobile wallets in 2017. These eWallets and others are also a must at the point of sale, more so than in any major global market.”.

He said that offline or non-digital payments can translate into missed payments for products and lack of visibility for transactions, all of which negatively impacts cash flow. Floyd noted that this is especially true where there is poor banking infrastructure in place, or where there are high and complex banking fees.

Avoid Non-Mandatory Contracts No one likes to be stuck in a contract, from cell phone contracts to credit card processing contracts. This process requires a merchant account, which is a special type of bank account that allows businesses to receive payments in multiple forms, including credit and debit cards.

billion non-prepaid debit card transactions in 2018, solidifying debit as a staple payment type. They insert or swipe their debit cards at stores’ point-of-sale (POS) devices — or key in details online — and maybe enter PINs, but the behind-the-scenes processes through which transactions are routed are kept invisible.

As described in a PYMNTS interview with Karen Webster, allows banks, non-bank FIs and businesses to turn on a host of services that, in essence, allow them to custom build their own consumer ecosystems. The payments space in China also includes a company called Pintec.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content