This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Despite their significant contributions to GDP and employment, SMEs in emerging markets remain underserved by traditional banking. For these businesses, securing a loan can be challenging, time-consuming, and costly.

Think about how easy it is to order a ride on Grab, book a hotel on Agoda, or pay for groceries on Shopee without even needing to pull out your credit card or open a banking app. The region has become a hotbed for embedded finance, thanks to its mobile-first economy and digitally savvy population.

Businesses can now process payments across multiple channels – including in-person, online, mobile, and over the phone – with greater speed, efficiency and security. The unified platform streamlines operations, reduces transaction times, and enhances the overall customer experience.

Kueski , the buy now, pay later (BNPL) and online consumer lender in Latin America, has launched an in-store version of Kueski Pay, which will become available to all consumers by the end of Q2 of 2024, to offer them the ability to complete transactions through the Kueski mobile app, regardless of internet connection, in physical stores.

Thailand is moving closer to welcoming its first virtual banks, with the Bank of Thailand (BOT) currently accepting applications for the virtual banking license. With the deadline looming on the 19th of September 2024, speculations are rife for Thailand’s virtual banking license applicants.

The pandemic has exposed the pain points of all verticals when it comes to payments, and especially when it comes to transacting in person, in a tactile environment, with cash, and where banking conduits are limited. Banks have been inching into the space; cash still remains a hallmark. Looking Toward Underserved Markets .

Mobile phone usage in Senegal has surpassed 60 per cent this year. The majority of traditional financial services infrastructure, such as ATMs and point-of-sale terminals, are concentrated in the capital city of Dakar, leaving rural areas underserved. appeared first on The Fintech Times.

Although lower costs and increased availability of new peer-to-peer (P2P) payment systems have allowed more first-time users to enjoy the ease and benefits of the banking system, the fact remains that 1.7 The fact that more telecom companies are now offering basic mobile payment services is also helping to bridge the unbanked gap.

In the past few years, the burgeoning popularity of digital banks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. First name. First name. Company Name. Phone number. Source: PwC.

Moniepoint , a Nigeria-based fintech offering an all-in-one banking, credit, and cross-border payment solution for African businesses and their customers, is on a mission to help businesses and individuals digitise their operations. to provide infrastructure and payment solutions for banks and financial institutions.

NOW Money , one of the leading inclusive digital payroll and banking platform for migrant workers, today announced its new strategic partnership with Mastercard , a global technology company in the payments industry. Customers can handle payments, transfers, and other financial operations directly from their mobile phones.

Over the years, weve covered a broad range of fintech topics from digital banking to decentralised finance , regtech , green fintech , and more. This includes services like mobilebanking, peer-to-peer payments, investment platforms, and blockchain applications. Consumer trust in banks plummeted.

We will explore success stories, the pivotal role of mobile money , and the unique challenges faced. The Role of Mobile Money Mobile money is a cornerstone of fintech in emerging markets. In many parts of Africa, mobile money services have seen explosive growth. In India, Paytm has revolutionised digital payments.

Virtual bank Radius Bank — which services small businesses (SMBs), micro-firms and consumers — is rolling out a revamped digital banking platform and a mobilebanking app, the company said on Monday (Dec. The platforms have added new digital solutions for financial budgeting and tracking as well.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financial inclusion and helping people develop healthy financial habits.

Lloyds Banking Group is shutting down its mobile van banking service this year and closing 123 branches, sparking concern over reduced access to essential financial services, particularly in rural and underserved areas. is unhappy with Lloyds’ decision to stop its mobile van banking service.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

-backed Chinese onlinebank is gearing up to launch soon following on the heels of establishing the bank. one of the bank’s investors, said Tuesday (Dec. 27) shareholders and regulators signed off on the name Sichuan XW Bank. The bank) will be officially open to users in the near future.”. consumers and 74.6

The list, produced by CNBC in collaboration with market research firm Statista, highlights the world’s top 250 fintech companies across eight market categories: payments, wealthtech, business process solutions, neobanking, alternative finance, financial planning, digital assets and banking solutions. billion (US$4.4

Orange Middle East and Africa (OMEA) ( www.Orange.com ) and Mastercard have announced a strategic partnership to expand access to mobile financial services across Sub-Saharan Africa. The partnership will be rolled out in seven countries including Cameroon, Central African Republic, Guinea-Bissau, Liberia, Mali, Senegal and Sierra Leone.

The report, Advancing Economic Inclusion—Empowering Underserved Communities with Fintech , highlights the innovative products and services revolutionizing the way commerce is conducted through safe, secure, convenient, and rewarding solutions.

EAZY Financial Services ‘EazyPay’, a Bahraini financial institution specialising in point-of-sale (POS) and online payment gateway acquiring services, has teamed up with Tarabut , the MENA region’s regulated open banking platform. Conister Bank Limited has launched an online deposit system for its UK retail customers.

Indian digital payments firm Paytm has officially launched a niche payments bank as part of its drive to double its customer base to 500 million over the next three years. The payments bank operates 31 branches and 3,000 customer points in its first year, the company noted in a release. billion in Paytm’s parent, One97 Communications.

This revolutionary service provides over 5 million Lebanese citizens with the ability to manage their payments securely and transparently for local and international purchases without needing a bank account. Through Wink Pay, we can simplify and digitize customer onboarding, as well as facilitate online payments.

Orange Middle East and Africa is strategically partnering with global payments giant Mastercard to expand access to mobile financial services across Sub-Saharan Africa. Only 48 per cent of the African adult population is banked, according to the African Digital Banking Transformation Report.

UK-based Zepz (previously known as WorldRemit Group) offers several onlinebanking services, including money deposit and collection, mobile money and top-ups, and online cashless transactions. The round drew participation from Accel, LeapFrog Investments, Technology Crossover Ventures, and Farallon Capital Management.

Cash Usage Decline : The World Bank reported that cash usage in advanced economies declined by nearly 50% during the pandemic, with consumers opting for digital and contactless payment methods instead. Consumers quickly embraced mobile wallets and tap-to-pay cards, driven by the desire to minimize physical contact during transactions.

12) the national launch of a mobile payments bank, which, according to a report , is India’s first one. According to the report, Airtel is taking advantage of a big push by the Indian government to accelerate financial inclusion and bring more competition to the market by issuing payment bank licenses.

Traditional banking products, including checking, credit, and savings accounts, are under threat from a new crop of digital-first startups. Many of these startups are launching products without a bank charter and targeting a very specific customer base. DOWNLOAD THE 61-PAGE consumer banking REPORT. savings accounts.

Consumers in the Philippines are demanding so much from online technologies, that research from Digido , the Filipino online lender, has found the digital lending market could reach $1billion in the second half of 2025. Digido revealed that in terms of market structure, non-bank digital lenders are expected to make up 55.2

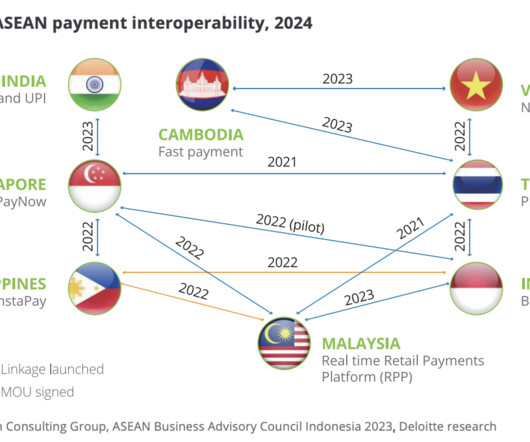

Asia Pacific point-of-sale payment methods – Select markets, Source: Beyond Payments: Digitalization Trends in the Cross-Border Checkout Revolution, Deloitte, Jul 2024 Payment interoperability The growth of digital payment innovations in APAC has emphasized the need for connectivity and interoperability in both online and offline transactions.

Grab , Razer , AirAsia , Axiata and CIMB join other companies that are considering applying for digital banking licenses in Malaysia, sources told Reuters on Wednesday (Jan. Some are in discussions with consultants for guidance as they ponder a move into digital banking, according to the sources, who are familiar with the matter.

. “SteelWave Digital can further bridge the financial accessibility gap by expanding its strategic partnerships with global liquidity providers to enhance capital flows into underserved markets. “Fintechs working to bridge this gap should focus on developing a superior user experience within the online platform and mobile channel.

New research from Economist Impact supported by Temenos finds that European banks are fighting back against competition from platform players, neobanks and payment providers. European banks are also migrating core banking systems to public cloud and SaaS in greater numbers than their counterparts in other regions.

India-based Paytm Payments Bank not only wants to become the world’s largest digital bank , but also to evolve into a financial services company providing a slew of services like wealth management and trading. 28), Paytm founder Vijay Shekhar Sharma said the company is aiming to have 500 million bank accounts.

At a high level, SoftPOS – short for software point of sale – lets merchants take contactless payments across their own mobile devices and tablets. And retailers across any range of settings are finding value in offering buy online, pickup in store ( BOPIS ) offerings.

However, recent stringent regulations imposed by the Reserve Bank of India (RBI) have significantly impacted the sector, leading many fintech companies to reassess their BNPL strategies. Similarly, Slice, originally a BNPL firm, has transitioned to offering prepaid credit cards and is now merging with North East Small Finance Bank.

In 2022, the country was home to 993 active fintech companies, representing about 25% of all fintech ventures operating across the ASEAN region, data from a 2022 report by the United Overseas Bank (UOB), PwC Singapore and the Singapore Fintech Association (SFA) reveal. billion to US$15 billion during the period. in July 2023.

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digital bank licenses to eligible applicants. Oversea-Chinese Banking Corp. and United Overseas Bank Ltd. billion ($1.1 Grab + Singtel .

As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment optionsfrom technical complexity to new forms of fraud and financial crimeare met. And thats a really positive development.

challenger bank Coconut, which launched only weeks ago to provide banking services for freelancers, has landed a new partner. 7) said PrePay Solutions (PPS) is working with the company to provide Coconut its banking infrastructure and prepaid card technology. Reports Wednesday (Feb.

It may not be the year of mobile payments — yet — but it is certainly the year mobile payments players are laying the groundwork for what they know is inevitable. This week, PYMNTS dug into the week of mobile pay news to bring you the latest from the ecosystem. Early Warning Boosts Big Banks’ P2P Power.

It enables financial institutions, especially those without core banking systems or with systems lacking API integration, to manage bulk transactions. Integrated with bank accounts and digital wallets in Pakistan, Hakeem provides customers with easy disbursement options. ThitsaWorks Pte.

Its intended use is to combat the widespread fraud and scams going on in relation to digital payments, and can let users cut off some companies from their bank accounts. The method can only be utilized for specific scenarios like online or mobile purchases or AP payments, so the expansion of mobile device usage has been a boost.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content