This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Future technologies and innovations In 2024, payments innovation is being driven by the rapid adoption of artificial intelligence (AI), tokenisation, and emerging technologies like central bank digital currencies (CBDCs) and stablecoins.

Despite these challenges, emerging usecases, increased regulatory clarity, and growing consumer interest suggest that open banking’s future in the USA holds promise for a more competitive financial landscape. Continued eCommerce Growth: The eCommerce sector is set to expand, driving demand for secure online payment methods.

Andrew Doukanaris Ambassador, The Payments Association While vIBANs have positive usecases, challenges exist in limited monitoring of the end user, alignment with the PSPs risk appetite, and the lack of a consistent framework to mitigate financial crime and regulatory risks.

AI will lead the way in transformation Dan Dica, CEO, Lynx Dan Dica , CEO, Lynx , the healthcare fintech explains how AI will transform risk management and compliance in payments. “The next big paymenttrend that will leave a significant impact is undoubtedly artificial intelligence (AI).

A big challenge with pull payments is that they don’t give consumers as much control over the movement of their funds as they would like. With push payments, the consumer is always in control of a transaction,” LaFleche said. Pull PaymentTrends. We don’t really see many usecases for real-time pull payments,” he said.

For example, there are a lot of stablecoins out there favored by those who simply want to use them as a store of value. Besides, Dhamodharan said Mastercard’s goal isn’t to turn cryptocurrency into the paymentstrend of 2020. But he added that the new program isn’t the only way Mastercard is looking at blockchain technology.

It was in a convergence of these trends that Visa launched its real-time payments solution, Visa Direct , a technology enabling push payments onto recipients’ Visa cards. Emerging And Unexpected UseCases. “This is a very flexible platform in terms of usecases,” he said.

Small banks are less able to afford widescale implementations of new faster payments technology off the bat, and so they tend to focus first on serving only the usecase they thought would be most impactful. They might focus on usecases serving whichever customer base is larger or provides most of their revenue, for example.

Data from Discover Global Network , the global payment network, comes as it reveals the results of its 2024 Payment State of the Union (PSOU) study, providing global perspectives from merchants and consumers.

How can we look to this rapidly growing business for new usecases for instant payments? Regulators encourage these efforts to educate and set a high bar, as evidenced in public commentary by NCUA board member and former chair Rodney Hood. What will this look like in the coming years?

Faster Payments Council (FPC), in partnership with Glenbrook Partners, today released results from the 3rd annual Faster Payments Barometer. The FPC conducted the latest survey of payments system stakeholders to gauge progress and perceptions around faster payments, trends, usecases, and challenges in the United States.

Additionally, we will hear from experts about the popularity and usecases of the payment technology, and if it will overtake credit card usage by 2025. Of course, not every region responds to paymenttrends in the same way.

Instant payments in the US ‘, surveyed 300 senior payment professionals in US banks to get a better picture of the demand for instant payments, the barriers to implementation, the challenges banks face, and other important paymenttrends. It’s given banks plenty of reasons not to modernise.

With innovations introducing virtual card technology and data analytics into the fold, the commercial card space is positioning itself to address some of the emerging challenges of business payments in accounts payable and beyond. Payroll company ADP recently estimated that as much as 80 percent of U.S.

Mastercard touted the solution’s ability to support faster payments as well as a host of other improvements, including cross-border efficiency and transparency. The API is a clear vote of confidence on Mastercard’s part that corporates want, and will use, faster payments services.

In addition, the use of biometrics in retail and payments — especially for fraud prevention, but also in other areas — is becoming more popular, and solid usecases are starting to accumulate. Mobile and digital payments are making inroads into penitentiaries around the world. Recent events in China and the U.K.

Luckily, the revolution in payments choice in just the past few years, to say nothing of COVID’s acceleration of any trend you can name, has proffered a solution to luxury’s woes. BNPL is perhaps the most-watched paymentstrend of the pandemic, and for good reason. Flexible Payments Give Lift to Luxury.

The “Twelve Days of Christmas” is a holiday classic, though some of us at PYMNTS still don’t understand why anyone would want to take a partridge away from what seems like a pleasant existence in a pear tree. In fact, PYMNTS found that 26 percent of consumers expressed interest in using contactless cards at physical stores.

Payments Flash-Forward: Why December 2020 Will Be One To Remember. PYMNTS asked 30 payment executives to make a prediction about payments and commerce that they’d put in a time capsule to be unearthed at the conclusion of next year. The decision comes after a lawsuit filed against the company by COTECH SA. Trackers and Reports.

The center’s strategy for shaping the future of payments encompasses a broad range of business needs and is constantly updated to keep par with the ever evolving paymenttrends of the region.

It depends a great deal on how many cards are in the market that are contactless-enabled, combined with contactless terminals, combined with the usecase for everyday payments. C ontactless basically targets low-value cash transactions as the first place that it kind of changes the paradigm and the speed of adoption. …

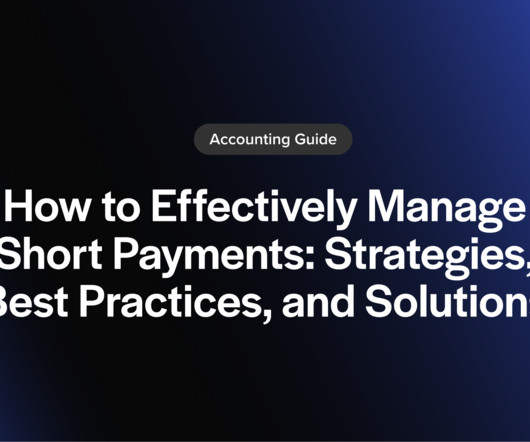

When a buyer pays less than the billed amount, also known as a short payment, significant challenges can arise for businesses trying to maintain a healthy cash flow. This article will explain short payments, their usecases, and how they can impact your bottom line to help your business effectively navigate and manage your finances.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content