This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The traditional underwriting process to buy life insurance is often painful for customers and costly for insurers. The post How Alternative Data Could Improve The Life Insurance Underwriting Process appeared first on CB Insights Research. Want the full expert post? Want the full expert post? Become a CB Insights customer.

Loan underwriting is a slow and complex process, due to insufficient data for credit scoring, stringent risk management requirements, and highly manual processes. The post 91 companies digitizing and accelerating the loan underwriting process appeared first on CB Insights Research. Fraud is also a concern.

Traditional banks will require credit histories and collateral to underwrite a small business loan, both of which many SMBs in Southeast Asian nations lack. At the root of the matter is often a lack of predictive data to ascertain the creditworthiness of these small- to medium-sized businesses (SMBs). Improving The SMB Lending Experience.

What are underwriting data platforms? Underwriting data platforms collect third-party alternative datasets, such as social media, public records, and demographic information. Insurers can tap into these data sources to augment their own internal datasets — with the goal of improving and expediting underwriting decisions.

Our research shows that 92.9 percent are doing so in credit underwriting. percent of FIs reported using AI in credit underwriting.”. The second-most common application is credit underwriting, as 71.4 Our research shows that 43.7 Our research shows that 43.7 Decisions, Decisions. percent), authentication (61.5

Property & casualty (P&C) underwriting is trapped by paper and a lack of robust datasets. The post 9 Startups Bringing Technology And Data To P&C Underwriting appeared first on CB Insights Research. This increases costs and creates opportunities for error. Want the full post? Become a CB Insights customer.

Digital Black Friday sales this year hit $9 billion, a 22 percent increase from 2019 figures, according to recent Adobe research. But according to Pero, banks aren't always equipped to fulfill online sellers' working capital needs due to their legacy underwriting processes. They're not looking at the future.".

Lastly, I was curious as to how much of the change might be demand-driven and how much is a function of supply, i.e. tightened underwriting. This is consistent with the known tightening in mortgage underwriting that occurred during the Great Recession. The post FICO Research: Are Millennials Really Abandoning Credit?

“Our technology and underwriting algorithms provide rapid, fair decisions, ensuring seamless transactions for merchants and their customers.” According to a market report by Grand View Research, the global fintech market is expected to reach $698.48 billion by 2030, expanding at a compound annual growth rate (CAGR) of 20.3%

As estimated by SPAC Research , 248 SPACs went public in 2020, raising $81 billion. The average underwriting fee is heftiest, as a percentage, on the smallest deals as measured in deal values, found PwC. The average underwriting fee is heftiest, as a percentage, on the smallest deals as measured in deal values, found PwC.

The post Why Smart Home Devices Could Be The Future Of Home Insurance Underwriting appeared first on CB Insights Research. Become a CB Insights customer. If you’re already a customer, log in here.

PYMNTS’ latest research reveals that this is changing, however: The share of financial institutions (FIs) using AI has increased dramatically since 2018. Our research reveals that while AI use remains limited among FIs, it has grown considerably, from 5.5 percent employ it for credit underwriting. percent today.

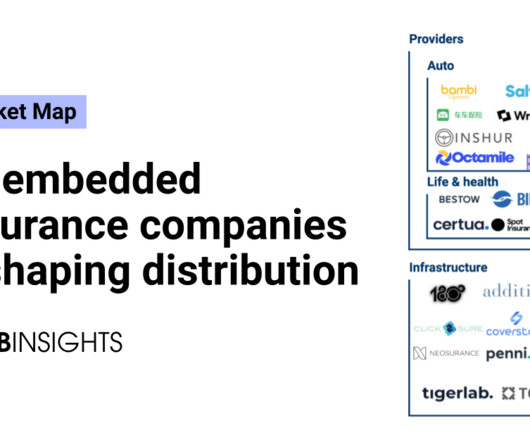

using payroll provider data for pay-as-you-go workers comp), improve underwriting accuracy (e.g. The post These 75 embedded insurance companies are transforming digital distribution appeared first on CB Insights Research. For consumers, these products can provide faster, more convenient, and more accessible insurance options.

The first clear trend observed around newly originated mortgages is that as we get further away from the Great Recession, underwriting criteria seems to have eased and a broader section of consumers are obtaining mortgages as a result. The post FICO Research: Broader Mix of Consumers Obtaining New Mortgages appeared first on FICO.

A new study from Juniper Research has found that the value of unsecured loans issued via AI underwriting platforms will reach USD 315 billion in 2025, up from just USD 24 billion in 2020.

The week begins with a few research-related announcements in the fintech and financial services space. The disposition of regulators toward change in the industry is a major concern as new technologies are introduced to enhance operations like underwriting and statistical modeling. The insurance business is ripe for innovation.

Founded in 1969 on the eve of the historic moon landing, MUFON — Mutual UFO Network — is the world’s largest organization that provides scientific research and investigation into the UFO phenomenon. The life blood may indeed be the researchers, field investigators and volunteers, which keep the organization off the ground.

Underwriting and claims automation. Why it matters: Insurers can use geospatial analytics to quickly and accurately underwrite policies and virtually assess claims for property insurance without needing in-person inspections. What’s next: Underwriting and claims teams have prioritized geospatial analytics in recent years.

Additionally, machine learning algorithms are analyzing vast amounts of data to automate processes like fraud detection, compliance, and underwriting. The post 90+ Startups Automating The Bank appeared first on CB Insights Research. Want the full expert post? Become a CB Insights customer.

We saw market research a couple of weeks ago that indicates the market evolved about 10 years in eight weeks in terms of increase in penetration. A rapidly changing world, he said, meant changes for MercadoLibre as well, particularly in its underwriting business MercadoCrédito. Creating Credit Scores Out Of Data .

Insurtech companies want to modernize processes like underwriting and distribution while also helping to establish entirely new forms of business within an industry that is often seen as old-fashioned. Insurtech has emerged as a major draw for VC investment, with the space attracting more than $6B in funding last year.

Allianz and Munich Re will use customers’ Google Cloud data to improve its underwriting: Due to the complex nature and catastrophic potential of cyber risks, insurers have often had problems underwriting and pricing policies. The post Google Is Partnering With Cyber Insurance Giants.

However, 25% of UK BNPL users have been charged with late payment fees according to research by the Centre for Financial Capability, which indicates there is a need to either improve underwriting and affordability standards or educate borrowers on the potential implications and consequences of using such a product.

POS systems come in a wide variety of shapes and sizes, so make sure you do your research and choose one with all of the right features for your unique business. Your account will then be approved by underwriters for a certain amount of money per transaction based on your business type, processing history, and ticket size.

According to sources cited by American Banker , the CFPB will remove the controversial underwriting rules that would have forced lenders to establish a borrower’s ability to repay before offering them a small-dollar, short-term lending product. Last October, the CFPB announced it would “revisit” the rules.

The cyber insurance market is an emerging sector, Sayata Labs CEO and Co-Founder Asaf Lifshitz explained in a recent interview with PYMNTS, and insurance providers are facing some tough hurdles in underwriting and risk mitigation. Rapid Expansion. Technology, Partnerships Address the Gaps.

Vesta ($30M Series A): Vesta provides a platform for mortgage origination and underwriting that is designed to streamline processes, reduce risk, and help lenders improve their book of business. appeared first on CB Insights Research.

The company uses machine learning tools to guarantee merchant payments and underwrite transactions. appeared first on CB Insights Research. Who are the parties to the deal? Paidy: Japan-based Paidy provides buy now, pay later services for e-commerce consumers. Its on a GMV run rate for about $1.5B Become a CB Insights customer.

From account opening to underwriting to claims disbursements, the auto insurance policy of the future will be built almost entirely on digital transactions. The post The Future of Auto Insurance: How technology is changing every aspect of the $766B market appeared first on CB Insights Research. But there is still a long way to go.

Pew Research, 2016 ). However, new FICO research points to just the opposite. Indeed, FICO’s research shows that just 64% of Millennials 18-24 have credit cards. To learn more about FICO research into Millennials and Credit Cards download our ebook or to learn more about our Bank Card Solutions visit fico.com.

Working with FICO, the company now can build flexible and customizable auto insurance pricing and life insurance underwriting decision-making solutions, with advanced simulation capabilities, in eight weeks. Our focus is on staying innovative by investing a lot in research and development for our products.

One of the largest P&C carriers in the US is looking to partner with insurtech companies that can help with underwriting, reinsurance, risk, and claims. The post The CB Insights Book of RFTs appeared first on CB Insights Research. See 140+ technology solutions that the world’s largest companies are looking for right now.

a leading payments technology company, has achieved significant results by creating a centralized underwriting management solution on the FICO® Decision Management Platform (DMP). The 2018 judges are: Sid Dash, research director at Chartis Research. Julie Conroy, research director for Aite Group’s Retail Banking practice.

Almost 85 per cent of tasks and activities in financial services firms would benefit from generative AI technology, according to a new research study by Fifty One Degrees , a London-based AI consultancy. Recent research estimates that generative AI will drive $2.6trillion to $4.4trillion annually in value for global companies.

This means the sub-merchants dont have to go through the lengthy and arduous underwriting process. Its also great for small businesses because it can eliminate many headaches associated with Know Your Customer (KYC) requirements, Anti-Money Laundering (AML) regulations, application processing, and underwriting.

The campus will be located between Facebook and Google in the Stanford Research Park. JPMorgan Chase is doubling down with its FinTech aspirations, gearing up to start development of a new FinTech corporate campus in the early part of 2019. CNBC reported that the campus in Palo Alto, California will be home to more than 1,000 employees.

FT Partners Research This nuanced approach to financing was exemplified by significant funding rounds in the Asia Pacific region, with Indian digital payments firm PhonePe and Australian-based Rakuten Securities securing substantial growth stage funding amounting to US$850 million and US$576 million, respectively. Ushering in Insurtech 2.0

A report in Zacks Equity Research Friday (Jan. This partnership will allow us to build on our proven broad-based direct origination capability and rigorous underwriting process while meeting the demands of our borrowers for proprietary middle market corporate loans.”

A report in Zacks Equity Research on Friday (Jan. This partnership will allow us to build on our proven broad-based direct origination capability and rigorous underwriting process while meeting the demands of our borrowers for proprietary middle-market corporate loans.” ” In another statement, Bradley E.

It represents a massive source of economic strength — according to Forrester Research estimates, B2B eCommerce will reach more than $1.1 Like Affirm, Resolve does that by assuming the payment risk, and acting as the underwriter for the credit lines offered to B2B buyers via its platform. trillion by 2020.

In a press release, the company said the foregoing included the full exercise of the underwriters’ option to purchase 1,249,999 additional shares from USA Technologies (USAT). The gross proceeds to the company from the offering, before deducting underwriting discounts and commissions and other offering expenses, was approximately $43.1

FT Partners Research This nuanced approach to financing was exemplified by significant funding rounds in the Asia Pacific region, with Indian digital payments firm PhonePe and Australian-based Rakuten Securities securing substantial growth stage funding amounting to US$850 million and US$576 million, respectively. Ushering in Insurtech 2.0

.” Utilising embedded finance and AI Ryan Miemczyk, director of research, Trust Impact Ltd Probably unsurprisingly, artificial intelligence (AI) could play a huge role in the fintech’s sector journey to becoming more ‘good’ However, its benefits will be truly seen when combined with other offerings.

PYMNTS’ own research has found that consumers are more willing than ever to switch banks in pursuit of better apps and user experiences. Cohen likened The Floor’s approach to building an “app store” of digital technologies that can be deployed as banks can improve their internal tech stacks with a range of new integrations.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content